Note

Click here to download the full example code

Estimate a stationary covariance function¶

The objective here is to estimate a stationary covariance model from data.

The library builds an estimation of the stationary covariance function on a ProcessSample or TimeSeries using the previous algorithm implemented in the StationaryCovarianceModelFactory class. The result consists in a UserDefinedStationaryCovarianceModel which is easy to manipulate.

Such an object is composed of a time grid and a collection of  square matrices of dimension d. corresponds to the number of time steps of the final time grid on which the covariance is estimated. When estimated from a time series , the UserDefinedStationaryCovarianceModel may have a time grid different from the initial time grid of the time series.

square matrices of dimension d. corresponds to the number of time steps of the final time grid on which the covariance is estimated. When estimated from a time series , the UserDefinedStationaryCovarianceModel may have a time grid different from the initial time grid of the time series.

from __future__ import print_function

import openturns as ot

import openturns.viewer as viewer

from matplotlib import pylab as plt

ot.Log.Show(ot.Log.NONE)

Create some 1-d normal process data with an Exponential covariance model

# Dimension parameter

dim = 1

# Create the time grid

t0 = 0.0

N = 300

t1 = 20.0

dt = (t1 - t0) / N

tgrid = ot.RegularGrid(t0, dt, N)

# Create the covariance model

amplitude = [1.0] * dim

scale = [1.0] * dim

covmodel = ot.ExponentialModel(scale, amplitude)

# Create a stationary Normal process with that covariance model

process = ot.GaussianProcess(covmodel, tgrid)

# Create a time series and a sample of time series

tseries = process.getRealization()

sample = process.getSample(1000)

Build a factory of stationary covariance function

covarianceFactory = ot.StationaryCovarianceModelFactory()

# Set the spectral factory algorithm

segmentNumber = 5

spectralFactory = ot.WelchFactory(ot.Hanning(), segmentNumber)

covarianceFactory.setSpectralModelFactory(spectralFactory)

# Check the current spectral factory

print(covarianceFactory.getSpectralModelFactory())

Out:

class=WelchFactory window = class=FilteringWindows implementation=class=Hanning blockNumber = 5 overlap = 0.5

Case 1 : Estimation on a ProcessSample

# The spectral model factory computes the spectral density function

# without using the block and overlap arguments of the Welch factories

estimatedModel_PS = covarianceFactory.build(sample)

# Case 2 : Estimation on a TimeSeries

# The spectral model factory compute the spectral density function using

# the block and overlap arguments of spectral model factories

estimatedModel_TS = covarianceFactory.build(tseries)

# Evaluate the covariance function at each time step

# Care : if estimated from a time series, the time grid has changed

for i in range(N):

tau = tgrid.getValue(i)

cov = estimatedModel_PS(tau)

Drawing…

sampleValueEstimated = ot.Sample(N, 1)

sampleValueModel = ot.Sample(N, 1)

for i in range(N):

t = tgrid.getValue(i)

for j in range(i - 1):

s = tgrid.getValue(j)

estimatedValue = estimatedModel_PS(t, s)

modelValue = covmodel(t, s)

if j == 0:

sampleValueEstimated[i, 0] = estimatedValue[0, 0]

sampleValueModel[i, 0] = modelValue[0, 0]

sampleT = tgrid.getVertices()

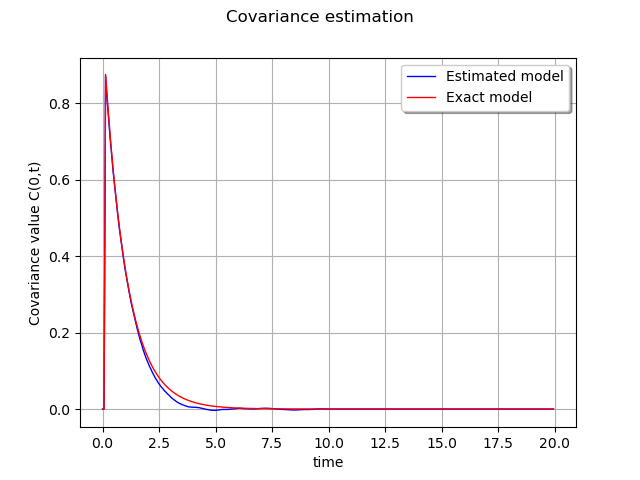

graph = ot.Graph('Covariance estimation', 'time', 'Covariance value C(0,t)', True)

curveEstimated = ot.Curve(sampleT, sampleValueEstimated, 'Estimated model')

graph.add(curveEstimated)

curveModel = ot.Curve(sampleT, sampleValueModel, 'Exact model')

curveModel.setColor('red')

graph.add(curveModel)

graph.setLegendPosition('topright')

view = viewer.View(graph)

plt.show()

Total running time of the script: ( 0 minutes 0.437 seconds)