Note

Go to the end to download the full example code

Estimate a GEV on race times data¶

In this example, we illustrate various techniques of extreme value modeling applied to the fatest annual race times for the women’s 1500 meter event over the period 1975-1992. Readers should refer to [coles2001] to get more details.

We illustrate techniques to:

estimate a stationary and a non stationary GEV,

estimate a return level,

using:

the log-likelihood function,

the profile log-likelihood function.

This analyse is particular as we are interested in modeling the annual minimum race times and not the annual maximum race times. In order to transform the minimum modeling into a maximum modeling, we proceeds as follows.

We denote by  where all the

where all the  are

independent and identically distributed variables. We introduce

are

independent and identically distributed variables. We introduce

for

for  ,

and

,

and  . Then, we have:

. Then, we have:

We can show that if the renormalized maximum  tends to the GEV distribution

parametrized by

tends to the GEV distribution

parametrized by  , then the renormalized minimum tends to

the GEV for minima distribution parametrized by

, then the renormalized minimum tends to

the GEV for minima distribution parametrized by  where:

where:

The cumulated distribution function of , denoted by  , is defined by:

, is defined by:

![\tilde{G}(z) = 1-G(-z) = 1-\exp \left( -\left[ 1-\tilde{\xi} \left( \dfrac{z-\tilde{\mu}}{\tilde{\sigma}}\right)\right]^{-1/\tilde{\xi}}\right)](data:image/svg+xml;base64,PD94bWwgdmVyc2lvbj0nMS4wJyBlbmNvZGluZz0nVVRGLTgnPz4KPCEtLSBUaGlzIGZpbGUgd2FzIGdlbmVyYXRlZCBieSBkdmlzdmdtIDMuMS4yIC0tPgo8c3ZnIHZlcnNpb249JzEuMScgeG1sbnM9J2h0dHA6Ly93d3cudzMub3JnLzIwMDAvc3ZnJyB4bWxuczp4bGluaz0naHR0cDovL3d3dy53My5vcmcvMTk5OS94bGluaycgd2lkdGg9JzI4OC40MDYwNjRwdCcgaGVpZ2h0PSczNi41NzI2OTlwdCcgdmlld0JveD0nNTAuMDY4NDY5IC0zNi41NzI2OTEgMjg4LjQwNjA2NCAzNi41NzI2OTknPgo8ZGVmcz4KPHBhdGggaWQ9J2c1LTQ5JyBkPSdNMi41MDI2MTUtNS4wNzY5NjFDMi41MDI2MTUtNS4yOTIxNTQgMi40ODY2NzUtNS4zMDAxMjUgMi4yNzE0ODItNS4zMDAxMjVDMS45NDQ3MDctNC45ODEzMiAxLjUyMjI5MS00Ljc5MDAzNyAuNzY1MTMxLTQuNzkwMDM3Vi00LjUyNzAyNEMuOTgwMzI0LTQuNTI3MDI0IDEuNDEwNzEtNC41MjcwMjQgMS44NzI5NzYtNC43NDIyMTdWLS42NTM1NDlDMS44NzI5NzYtLjM1ODY1NSAxLjg0OTA2Ni0uMjYzMDE0IDEuMDkxOTA1LS4yNjMwMTRILjgxMjk1MVYwQzEuMTM5NzI2LS4wMjM5MSAxLjgyNTE1Ni0uMDIzOTEgMi4xODM4MTEtLjAyMzkxUzMuMjM1ODY2LS4wMjM5MSAzLjU2MjY0IDBWLS4yNjMwMTRIMy4yODM2ODZDMi41MjY1MjYtLjI2MzAxNCAyLjUwMjYxNS0uMzU4NjU1IDIuNTAyNjE1LS42NTM1NDlWLTUuMDc2OTYxWicvPgo8cGF0aCBpZD0nZzUtMTI2JyBkPSdNMy4zNTU0MTctNS4zNDc5NDVDMy4wMjg2NDMtNC45ODkyOSAyLjc4MTU2OS00Ljk4OTI5IDIuNjkzODk4LTQuOTg5MjlDMi41MTA1ODUtNC45ODkyOSAyLjM0MzIxMy01LjA2ODk5MSAyLjE1MTkzLTUuMTcyNjAzQzEuOTM2NzM3LTUuMjc2MjE0IDEuNzkzMjc1LTUuMzQ3OTQ1IDEuNjA5OTYzLTUuMzQ3OTQ1QzEuMjk5MTI4LTUuMzQ3OTQ1IDEuMTM5NzI2LTUuMTgwNTczIC43MDkzNC00LjcxMDMzNkwuODY4NzQyLTQuNTU4OTA0QzEuMTk1NTE3LTQuOTE3NTU5IDEuNDQyNTktNC45MTc1NTkgMS41MzAyNjItNC45MTc1NTlDMS43MTM1NzQtNC45MTc1NTkgMS44ODA5NDYtNC44Mzc4NTggMi4wNzIyMjktNC43MzQyNDdDMi4yODc0MjItNC42MzA2MzUgMi40MzA4ODQtNC41NTg5MDQgMi42MTQxOTctNC41NTg5MDRDMi45MjUwMzEtNC41NTg5MDQgMy4wODQ0MzMtNC43MjYyNzYgMy41MTQ4MTktNS4xOTY1MTNMMy4zNTU0MTctNS4zNDc5NDVaJy8+CjxwYXRoIGlkPSdnMS0wJyBkPSdNNS41NzExMDgtMS44MDkyMTVDNS42OTg2My0xLjgwOTIxNSA1Ljg3Mzk3My0xLjgwOTIxNSA1Ljg3Mzk3My0xLjk5MjUyOFM1LjY5ODYzLTIuMTc1ODQxIDUuNTcxMTA4LTIuMTc1ODQxSDEuMDA0MjM0Qy44NzY3MTItMi4xNzU4NDEgLjcwMTM3LTIuMTc1ODQxIC43MDEzNy0xLjk5MjUyOFMuODc2NzEyLTEuODA5MjE1IDEuMDA0MjM0LTEuODA5MjE1SDUuNTcxMTA4WicvPgo8cGF0aCBpZD0nZzAtMTgnIGQ9J004LjM2ODYxOCAyOC4wODI2OUM4LjM2ODYxOCAyOC4wMzQ4NjkgOC4zNDQ3MDcgMjguMDEwOTU5IDguMzIwNzk3IDI3Ljk3NTA5M0M3Ljg3ODQ1NiAyNy41MzI3NTIgNy4wNzc0NiAyNi43MzE3NTYgNi4yNzY0NjMgMjUuNDQwNTk4QzQuMzUxNjgxIDIyLjM1NjE2NCAzLjQ3ODk1NCAxOC40NzA3MzUgMy40Nzg5NTQgMTMuODY3OTk1QzMuNDc4OTU0IDEwLjY1MjA1NSAzLjkwOTM0IDYuNTAzNjExIDUuODgxOTQzIDIuOTQwOTcxQzYuODI2NDAxIDEuMjQzMzM3IDcuODA2NzI1IC4yNjMwMTQgOC4zMzI3NTItLjI2MzAxNEM4LjM2ODYxOC0uMjk4ODc5IDguMzY4NjE4LS4zMjI3OSA4LjM2ODYxOC0uMzU4NjU1QzguMzY4NjE4LS40NzgyMDcgOC4yODQ5MzItLjQ3ODIwNyA4LjExNzU1OS0uNDc4MjA3UzcuOTI2Mjc2LS40NzgyMDcgNy43NDY5NDktLjI5ODg3OUMzLjc0MTk2OCAzLjM0NzQ0NyAyLjQ4NjY3NSA4LjgyMjkxNCAyLjQ4NjY3NSAxMy44NTYwNEMyLjQ4NjY3NSAxOC41NTQ0MjEgMy41NjI2NCAyMy4yODg2NjcgNi41OTkyNTMgMjYuODYzMjYzQzYuODM4MzU2IDI3LjEzODIzMiA3LjI5MjY1MyAyNy42MjgzOTQgNy43ODI4MTQgMjguMDU4NzhDNy45MjYyNzYgMjguMjAyMjQyIDcuOTUwMTg3IDI4LjIwMjI0MiA4LjExNzU1OSAyOC4yMDIyNDJTOC4zNjg2MTggMjguMjAyMjQyIDguMzY4NjE4IDI4LjA4MjY5WicvPgo8cGF0aCBpZD0nZzAtMTknIGQ9J002LjMwMDM3NCAxMy44Njc5OTVDNi4zMDAzNzQgOS4xNjk2MTQgNS4yMjQ0MDggNC40MzUzNjcgMi4xODc3OTYgLjg2MDc3MkMxLjk0ODY5MiAuNTg1ODAzIDEuNDk0Mzk2IC4wOTU2NDEgMS4wMDQyMzQtLjMzNDc0NUMuODYwNzcyLS40NzgyMDcgLjgzNjg2Mi0uNDc4MjA3IC42Njk0ODktLjQ3ODIwN0MuNTI2MDI3LS40NzgyMDcgLjQxODQzMS0uNDc4MjA3IC40MTg0MzEtLjM1ODY1NUMuNDE4NDMxLS4zMTA4MzQgLjQ2NjI1Mi0uMjYzMDE0IC40OTAxNjItLjIzOTEwM0MuOTA4NTkzIC4xOTEyODMgMS43MDk1ODkgLjk5MjI3OSAyLjUxMDU4NSAyLjI4MzQzN0M0LjQzNTM2NyA1LjM2Nzg3IDUuMzA4MDk1IDkuMjUzMyA1LjMwODA5NSAxMy44NTYwNEM1LjMwODA5NSAxNy4wNzE5OCA0Ljg3NzcwOSAyMS4yMjA0MjMgMi45MDUxMDYgMjQuNzgzMDY0QzEuOTYwNjQ4IDI2LjQ4MDY5NyAuOTY4MzY5IDI3LjQ3Mjk3NiAuNDY2MjUyIDI3Ljk3NTA5M0MuNDQyMzQxIDI4LjAxMDk1OSAuNDE4NDMxIDI4LjA0NjgyNCAuNDE4NDMxIDI4LjA4MjY5Qy40MTg0MzEgMjguMjAyMjQyIC41MjYwMjcgMjguMjAyMjQyIC42Njk0ODkgMjguMjAyMjQyQy44MzY4NjIgMjguMjAyMjQyIC44NjA3NzIgMjguMjAyMjQyIDEuMDQwMSAyOC4wMjI5MTRDNS4wNDUwODEgMjQuMzc2NTg4IDYuMzAwMzc0IDE4LjkwMTEyMSA2LjMwMDM3NCAxMy44Njc5OTVaJy8+CjxwYXRoIGlkPSdnMC0yMCcgZD0nTTIuOTg4NzkyIDI4LjIwMjI0Mkg2LjEzMzAwMVYyNy41NDQ3MDdIMy42NDYzMjZWLjE3OTMyOEg2LjEzMzAwMVYtLjQ3ODIwN0gyLjk4ODc5MlYyOC4yMDIyNDJaJy8+CjxwYXRoIGlkPSdnMC0yMScgZD0nTTIuNjU0MDQ3IDI3LjU0NDcwN0guMTY3MzcyVjI4LjIwMjI0MkgzLjMxMTU4MlYtLjQ3ODIwN0guMTY3MzcyVi4xNzkzMjhIMi42NTQwNDdWMjcuNTQ0NzA3WicvPgo8cGF0aCBpZD0nZzAtMzInIGQ9J005LjA1MDA2MiAzNS4yNTU3OTFDOS4wNTAwNjIgMzUuMjE5OTI1IDkuMDUwMDYyIDM1LjE5NjAxNSA4Ljk3ODMzMSAzNS4xMTIzMjlDNy44MzA2MzUgMzMuNzI1NTI5IDYuODc0MjIyIDMyLjE5NTI2OCA2LjE2ODg2NyAzMC41MzM0OTlDNC42MDI3NCAyNi44NzUyMTggMy45ODEwNzEgMjIuNTk1MjY4IDMuOTgxMDcxIDE3LjQ1NDU0NUMzLjk4MTA3MSAxMi4zNjE2NDQgNC41NjY4NzQgNy44OTA0MTEgNi4zMzYyMzkgMy45NjkxMTZDNy4wMjk2MzkgMi40NTA4MDkgNy45MzgyMzIgMS4wNDAxIDkuMDAyMjQyLS4yNTEwNTlDOS4wMjYxNTItLjI4NjkyNCA5LjA1MDA2Mi0uMzEwODM0IDkuMDUwMDYyLS4zNTg2NTVDOS4wNTAwNjItLjQ3ODIwNyA4Ljk2NjM3Ni0uNDc4MjA3IDguNzg3MDQ5LS40NzgyMDdTOC41ODM4MTEtLjQ3ODIwNyA4LjU1OTktLjQ1NDI5NkM4LjU0Nzk0NS0uNDQyMzQxIDcuODA2NzI1IC4yNzQ5NjkgNi44NzQyMjIgMS41OTAwMzdDNC43OTQwMjIgNC41MzEwMDkgMy43NDE5NjggOC4wNDU4MjggMy4yMDM5ODUgMTEuNjA4NDY4QzIuOTE3MDYxIDEzLjUzMzI1IDIuODIxNDIgMTUuNDkzODk4IDIuODIxNDIgMTcuNDQyNTlDMi44MjE0MiAyMS45MTM4MjMgMy4zODMzMTMgMjYuNDgwNjk3IDUuMjk2MTM5IDMwLjU2OTM2NUM2LjE0NDk1NiAzMi4zODY1NSA3LjI4MDY5NyAzNC4wMjQ0MDggOC40NjQyNTkgMzUuMjY3NzQ2QzguNTcxODU2IDM1LjM2MzM4NyA4LjU4MzgxMSAzNS4zNzUzNDIgOC43ODcwNDkgMzUuMzc1MzQyQzguOTY2Mzc2IDM1LjM3NTM0MiA5LjA1MDA2MiAzNS4zNzUzNDIgOS4wNTAwNjIgMzUuMjU1NzkxWicvPgo8cGF0aCBpZD0nZzAtMzMnIGQ9J002LjYzNTExOCAxNy40NTQ1NDVDNi42MzUxMTggMTIuOTgzMzEzIDYuMDczMjI1IDguNDE2NDM4IDQuMTYwMzk5IDQuMzI3NzcxQzMuMzExNTgyIDIuNTEwNTg1IDIuMTc1ODQxIC44NzI3MjcgLjk5MjI3OS0uMzcwNjFDLjg4NDY4Mi0uNDY2MjUyIC44NzI3MjctLjQ3ODIwNyAuNjY5NDg5LS40NzgyMDdDLjUwMjExNy0uNDc4MjA3IC40MDY0NzYtLjQ3ODIwNyAuNDA2NDc2LS4zNTg2NTVDLjQwNjQ3Ni0uMzEwODM0IC40NTQyOTYtLjI1MTA1OSAuNDc4MjA3LS4yMTUxOTNDMS42MjU5MDMgMS4xNzE2MDYgMi41ODIzMTYgMi43MDE4NjggMy4yODc2NzEgNC4zNjM2MzZDNC44NTM3OTggOC4wMjE5MTggNS40NzU0NjcgMTIuMzAxODY4IDUuNDc1NDY3IDE3LjQ0MjU5QzUuNDc1NDY3IDIyLjUzNTQ5MiA0Ljg4OTY2NCAyNy4wMDY3MjUgMy4xMjAyOTkgMzAuOTI4MDJDMi40MjY4OTkgMzIuNDQ2MzI2IDEuNTE4MzA2IDMzLjg1NzAzNiAuNDU0Mjk2IDM1LjE0ODE5NEMuNDQyMzQxIDM1LjE3MjEwNSAuNDA2NDc2IDM1LjIxOTkyNSAuNDA2NDc2IDM1LjI1NTc5MUMuNDA2NDc2IDM1LjM3NTM0MiAuNTAyMTE3IDM1LjM3NTM0MiAuNjY5NDg5IDM1LjM3NTM0MkMuODQ4ODE3IDM1LjM3NTM0MiAuODcyNzI3IDM1LjM3NTM0MiAuODk2NjM4IDM1LjM1MTQzMkMuOTA4NTkzIDM1LjMzOTQ3NyAxLjY0OTgxMyAzNC42MjIxNjcgMi41ODIzMTYgMzMuMzA3MDk4QzQuNjYyNTE2IDMwLjM2NjEyNyA1LjcxNDU3IDI2Ljg1MTMwOCA2LjI1MjU1MyAyMy4yODg2NjdDNi41Mzk0NzcgMjEuMzYzODg1IDYuNjM1MTE4IDE5LjQwMzIzOCA2LjYzNTExOCAxNy40NTQ1NDVaJy8+CjxwYXRoIGlkPSdnMi0wJyBkPSdNNy44Nzg0NTYtMi43NDk2ODlDOC4wODE2OTQtMi43NDk2ODkgOC4yOTY4ODctMi43NDk2ODkgOC4yOTY4ODctMi45ODg3OTJTOC4wODE2OTQtMy4yMjc4OTUgNy44Nzg0NTYtMy4yMjc4OTVIMS40MTA3MUMxLjIwNzQ3Mi0zLjIyNzg5NSAuOTkyMjc5LTMuMjI3ODk1IC45OTIyNzktMi45ODg3OTJTMS4yMDc0NzItMi43NDk2ODkgMS40MTA3MS0yLjc0OTY4OUg3Ljg3ODQ1NlonLz4KPHBhdGggaWQ9J2c0LTIyJyBkPSdNMS43MjE1NDQtLjI2MzAxNEMyLjAyMDQyMyAuMDExOTU1IDIuNDYyNzY1IC4xMTk1NTIgMi44NjkyNCAuMTE5NTUyQzMuNjM0MzcxIC4xMTk1NTIgNC4xNjAzOTktLjM5NDUyMSA0LjQzNTM2Ny0uNzY1MTMxQzQuNTU0OTE5LS4xMzE1MDcgNS4wNTcwMzYgLjExOTU1MiA1LjQ3NTQ2NyAuMTE5NTUyQzUuODM0MTIyIC4xMTk1NTIgNi4xMjEwNDYtLjA5NTY0MSA2LjMzNjIzOS0uNTI2MDI3QzYuNTI3NTIyLS45MzI1MDMgNi42OTQ4OTQtMS42NjE3NjggNi42OTQ4OTQtMS43MDk1ODlDNi42OTQ4OTQtMS43NjkzNjUgNi42NDcwNzMtMS44MTcxODYgNi41NzUzNDItMS44MTcxODZDNi40Njc3NDYtMS44MTcxODYgNi40NTU3OTEtMS43NTc0MSA2LjQwNzk3LTEuNTc4MDgyQzYuMjI4NjQzLS44NzI3MjcgNi4wMDE0OTQtLjExOTU1MiA1LjUxMTMzMy0uMTE5NTUyQzUuMTY0NjMzLS4xMTk1NTIgNS4xNDA3MjItLjQzMDM4NiA1LjE0MDcyMi0uNjY5NDg5QzUuMTQwNzIyLS45NDQ0NTggNS4yNDgzMTktMS4zNzQ4NDQgNS4zMzIwMDUtMS43MzM0OTlMNS42NjY3NS0zLjAyNDY1OEM1LjcxNDU3LTMuMjUxODA2IDUuODQ2MDc3LTMuNzg5Nzg4IDUuOTA1ODUzLTQuMDA0OTgxQzUuOTc3NTg0LTQuMjkxOTA1IDYuMTA5MDkxLTQuODA1OTc4IDYuMTA5MDkxLTQuODUzNzk4QzYuMTA5MDkxLTUuMDMzMTI2IDUuOTY1NjI5LTUuMTUyNjc3IDUuNzg2MzAxLTUuMTUyNjc3QzUuNjc4NzA1LTUuMTUyNjc3IDUuNDI3NjQ2LTUuMTA0ODU3IDUuMzMyMDA1LTQuNzQ2MjAyTDQuNDk1MTQzLTEuNDIyNjY1QzQuNDM1MzY3LTEuMTgzNTYyIDQuNDM1MzY3LTEuMTU5NjUxIDQuMjc5OTUtLjk2ODM2OUM0LjEzNjQ4OC0uNzY1MTMxIDMuNjcwMjM3LS4xMTk1NTIgMi45MTcwNjEtLjExOTU1MkMyLjI0NzU3Mi0uMTE5NTUyIDIuMDMyMzc5LS42MDk3MTQgMi4wMzIzNzktMS4xNzE2MDZDMi4wMzIzNzktMS41MTgzMDYgMi4xMzk5NzUtMS45MzY3MzcgMi4xODc3OTYtMi4xMzk5NzVMMi43MjU3NzgtNC4yOTE5MDVDMi43ODU1NTQtNC41MTkwNTQgMi44ODExOTYtNC45MDE2MTkgMi44ODExOTYtNC45NzMzNUMyLjg4MTE5Ni01LjE2NDYzMyAyLjcyNTc3OC01LjI3MjIyOSAyLjU3MDM2MS01LjI3MjIyOUMyLjQ2Mjc2NS01LjI3MjIyOSAyLjE5OTc1MS01LjIzNjM2NCAyLjEwNDExLTQuODUzNzk4TC4zNzA2MSAyLjA2ODI0NEMuMzU4NjU1IDIuMTI4MDIgLjMzNDc0NSAyLjE5OTc1MSAuMzM0NzQ1IDIuMjcxNDgyQy4zMzQ3NDUgMi40NTA4MDkgLjQ3ODIwNyAyLjU3MDM2MSAuNjU3NTM0IDIuNTcwMzYxQzEuMDA0MjM0IDIuNTcwMzYxIDEuMDc1OTY1IDIuMjk1MzkyIDEuMTU5NjUxIDEuOTYwNjQ4TDEuNzIxNTQ0LS4yNjMwMTRaJy8+CjxwYXRoIGlkPSdnNC0yNCcgZD0nTTMuMTIwMjk5IC4wNTk3NzZMMS44NjUwMDYtLjQ0MjM0MUMxLjU1NDE3Mi0uNTYxODkzIC44MzY4NjItLjg0ODgxNyAuODM2ODYyLTEuNTY2MTI3Qy44MzY4NjItMi41OTQyNzEgMi4wOTIxNTQtMy42MzQzNzEgMi4zNDMyMTMtMy42MzQzNzFDMi4zNjcxMjMtMy42MzQzNzEgMi40NzQ3Mi0zLjYxMDQ2MSAyLjUxMDU4NS0zLjU5ODUwNkMyLjgzMzM3NS0zLjUwMjg2NCAzLjE0NDIwOS0zLjUwMjg2NCAzLjM1OTQwMi0zLjUwMjg2NEMzLjczMDAxMi0zLjUwMjg2NCA0LjQzNTM2Ny0zLjUwMjg2NCA0LjQzNTM2Ny0zLjg0OTU2NEM0LjQzNTM2Ny00LjExMjU3OCA0LjAwNDk4MS00LjE0ODQ0MyAzLjQ5MDkwOS00LjE0ODQ0M0MzLjI1MTgwNi00LjE0ODQ0MyAyLjkyOTAxNi00LjE0ODQ0MyAyLjQ5ODYzLTQuMDA0OTgxQzIuMjExNzA2LTQuMjQ0MDg1IDIuMDkyMTU0LTQuNjI2NjUgMi4wOTIxNTQtNC45ODUzMDVDMi4wOTIxNTQtNS42NDI4MzkgMi41MjI1NC02LjU3NTM0MiAzLjQ2Njk5OS03LjAxNzY4NEMzLjY4MjE5Mi02Ljc2NjYyNSAzLjk2OTExNi02Ljc2NjYyNSA0LjIyMDE3NC02Ljc2NjYyNUM0LjUxOTA1NC02Ljc2NjYyNSA1LjI0ODMxOS02Ljc2NjYyNSA1LjI0ODMxOS03LjExMzMyNUM1LjI0ODMxOS03LjQxMjIwNCA0LjY3NDQ3MS03LjQxMjIwNCA0LjI5MTkwNS03LjQxMjIwNEM0LjA1MjgwMi03LjQxMjIwNCAzLjg3MzQ3NC03LjQxMjIwNCAzLjUzODczLTcuMzUyNDI4QzMuNDc4OTU0LTcuNDk1ODkgMy40NjY5OTktNy41MTk4MDEgMy40NjY5OTktNy43ODI4MTRDMy40NjY5OTktNy45OTgwMDcgMy41MTQ4MTktOC4xNjUzOCAzLjUxNDgxOS04LjIwMTI0NUMzLjUxNDgxOS04LjI3Mjk3NiAzLjQ1NTA0NC04LjMyMDc5NyAzLjM5NTI2OC04LjMyMDc5N0MzLjIwMzk4NS04LjMyMDc5NyAzLjIwMzk4NS03Ljg3ODQ1NiAzLjIwMzk4NS03Ljc4MjgxNEMzLjIwMzk4NS03LjYxNTQ0MiAzLjIxNTk0LTcuNDQ4MDcgMy4yODc2NzEtNy4yOTI2NTNDMS44NTMwNTEtNi44NzQyMjIgMS4yMTk0MjctNS44NTgwMzIgMS4yMTk0MjctNS4wODA5NDZDMS4yMTk0MjctNC4zNjM2MzYgMS42OTc2MzQtMy45NjkxMTYgMi4wMjA0MjMtMy43ODk3ODhDLjc4OTA0MS0zLjEyMDI5OSAuMjYzMDE0LTEuOTAwODcyIC4yNjMwMTQtMS4yNTUyOTNDLjI2MzAxNC0uMjE1MTkzIDEuMjA3NDcyIC4xNTU0MTcgMS42Mzc4NTggLjMzNDc0NUwyLjcxMzgyMyAuNzY1MTMxQzMuMDEyNzAyIC44NzI3MjcgMy41MDI4NjQgMS4wNzU5NjUgMy41ODY1NSAxLjEyMzc4NkMzLjcwNjEwMiAxLjIwNzQ3MiAzLjgwMTc0MyAxLjM1MDkzNCAzLjgwMTc0MyAxLjU0MjIxN0MzLjgwMTc0MyAxLjc5MzI3NSAzLjYxMDQ2MSAyLjE5OTc1MSAzLjE5MjAzIDIuMTk5NzUxQzMuMDEyNzAyIDIuMTk5NzUxIDIuNjE4MTgyIDIuMTUxOTMgMi4xODc3OTYgMS44MjkxNDFDMi4xMDQxMSAxLjc1NzQxIDIuMDkyMTU0IDEuNzQ1NDU1IDIuMDQ0MzM0IDEuNzQ1NDU1QzEuOTg0NTU4IDEuNzQ1NDU1IDEuOTI0NzgyIDEuNzkzMjc1IDEuOTI0NzgyIDEuODY1MDA2QzEuOTI0NzgyIDEuOTk2NTEzIDIuNTQ2NDUxIDIuNDM4ODU0IDMuMTkyMDMgMi40Mzg4NTRDMy45NTcxNjEgMi40Mzg4NTQgNC40MjM0MTIgMS42OTc2MzQgNC40MjM0MTIgMS4xODM1NjJDNC40MjM0MTIgLjgxMjk1MSA0LjIyMDE3NCAuNTE0MDcyIDMuODM3NjA5IC4zNDY3TDMuMTIwMjk5IC4wNTk3NzZaTTMuNzMwMDEyLTcuMTEzMzI1QzMuOTMzMjUtNy4xNzMxMDEgNC4xNDg0NDMtNy4xNzMxMDEgNC4zMDM4NjEtNy4xNzMxMDFDNC42OTgzODEtNy4xNzMxMDEgNC43MzQyNDctNy4xNjExNDYgNC45NzMzNS03LjEwMTM3QzQuODI5ODg4LTcuMDQxNTk0IDQuNzM0MjQ3LTcuMDA1NzI5IDQuMjMyMTMtNy4wMDU3MjlDNC4wMDQ5ODEtNy4wMDU3MjkgMy44NjE1MTktNy4wMDU3MjkgMy43MzAwMTItNy4xMTMzMjVaTTIuNzg1NTU0LTMuODM3NjA5QzMuMDcyNDc4LTMuOTA5MzQgMy4zMzU0OTItMy45MDkzNCAzLjQ3ODk1NC0zLjkwOTM0QzMuODczNDc0LTMuOTA5MzQgMy44OTczODUtMy44OTczODUgNC4xNjAzOTktMy44Mzc2MDlDNC4wMjg4OTItMy43Nzc4MzMgMy45MjEyOTUtMy43NDE5NjggMy40MDcyMjMtMy43NDE5NjhDMy4xMjAyOTktMy43NDE5NjggMy4wMDA3NDctMy43NDE5NjggMi43ODU1NTQtMy44Mzc2MDlaJy8+CjxwYXRoIGlkPSdnNC0yNycgZD0nTTYuMDczMjI1LTQuNTA3MDk4QzYuMjI4NjQzLTQuNTA3MDk4IDYuNjIzMTYzLTQuNTA3MDk4IDYuNjIzMTYzLTQuODg5NjY0QzYuNjIzMTYzLTUuMTUyNjc3IDYuMzk2MDE1LTUuMTUyNjc3IDYuMTgwODIyLTUuMTUyNjc3SDMuNTM4NzNDMS43NDU0NTUtNS4xNTI2NzcgLjQ1NDI5Ni0zLjE1NjE2NCAuNDU0Mjk2LTEuNzQ1NDU1Qy40NTQyOTYtLjcyOTI2NSAxLjExMTgzMSAuMTE5NTUyIDIuMTg3Nzk2IC4xMTk1NTJDMy41OTg1MDYgLjExOTU1MiA1LjE0MDcyMi0xLjM5ODc1NSA1LjE0MDcyMi0zLjE5MjAzQzUuMTQwNzIyLTMuNjU4MjgxIDUuMDMzMTI2LTQuMTEyNTc4IDQuNzQ2MjAyLTQuNTA3MDk4SDYuMDczMjI1Wk0yLjE5OTc1MS0uMTE5NTUyQzEuNTkwMDM3LS4xMTk1NTIgMS4xNDc2OTYtLjU4NTgwMyAxLjE0NzY5Ni0xLjQxMDcxQzEuMTQ3Njk2LTIuMTI4MDIgMS41NzgwODItNC41MDcwOTggMy4zMzU0OTItNC41MDcwOThDMy44NDk1NjQtNC41MDcwOTggNC40MjM0MTItNC4yNTYwNCA0LjQyMzQxMi0zLjMzNTQ5MkM0LjQyMzQxMi0yLjkxNzA2MSA0LjIzMjEzLTEuOTEyODI3IDMuODEzNjk5LTEuMjE5NDI3QzMuMzgzMzEzLS41MTQwNzIgMi43Mzc3MzMtLjExOTU1MiAyLjE5OTc1MS0uMTE5NTUyWicvPgo8cGF0aCBpZD0nZzQtNzEnIGQ9J004LjkxODU1NS04LjMwODg0MkM4LjkxODU1NS04LjQxNjQzOCA4LjgzNDg2OS04LjQxNjQzOCA4LjgxMDk1OS04LjQxNjQzOFM4LjczOTIyOC04LjQxNjQzOCA4LjY0MzU4Ny04LjI5Njg4N0w3LjgxODY4LTcuMzA0NjA4QzcuNzU4OTA0LTcuNDAwMjQ5IDcuNTE5ODAxLTcuODE4NjggNy4wNTM1NDktOC4wOTM2NDlDNi41Mzk0NzctOC40MTY0MzggNi4wMjU0MDUtOC40MTY0MzggNS44NDYwNzctOC40MTY0MzhDMy4yODc2NzEtOC40MTY0MzggLjU5Nzc1OC01LjgxMDIxMiAuNTk3NzU4LTIuOTg4NzkyQy41OTc3NTgtMS4wMTYxODkgMS45NjA2NDggLjI1MTA1OSAzLjc1MzkyMyAuMjUxMDU5QzQuNjE0Njk1IC4yNTEwNTkgNS43MDI2MTUtLjAzNTg2NiA2LjMwMDM3NC0uNzg5MDQxQzYuNDMxODgtLjMzNDc0NSA2LjY5NDg5NC0uMDExOTU1IDYuNzc4NTgtLjAxMTk1NUM2LjgzODM1Ni0uMDExOTU1IDYuODUwMzExLS4wNDc4MjEgNi44NjIyNjctLjA0NzgyMUM2Ljg3NDIyMi0uMDcxNzMxIDYuOTY5ODYzLS40OTAxNjIgNy4wMjk2MzktLjcwNTM1NUw3LjIyMDkyMi0xLjQ3MDQ4NkM3LjMxNjU2My0xLjg2NTAwNiA3LjM2NDM4NC0yLjAzMjM3OSA3LjQ0ODA3LTIuMzkxMDM0QzcuNTY3NjIxLTIuODQ1MzMgNy41OTE1MzItMi44ODExOTYgOC4yNDkwNjYtMi44OTMxNTFDOC4yOTY4ODctMi44OTMxNTEgOC40NDAzNDktMi44OTMxNTEgOC40NDAzNDktMy4xMjAyOTlDOC40NDAzNDktMy4yMzk4NTEgOC4zMjA3OTctMy4yMzk4NTEgOC4yODQ5MzItMy4yMzk4NTFDOC4wODE2OTQtMy4yMzk4NTEgNy44NTQ1NDUtMy4yMTU5NCA3LjYzOTM1Mi0zLjIxNTk0SDYuOTkzNzczQzYuNDkxNjU2LTMuMjE1OTQgNS45NjU2MjktMy4yMzk4NTEgNS40NzU0NjctMy4yMzk4NTFDNS4zNjc4Ny0zLjIzOTg1MSA1LjIyNDQwOC0zLjIzOTg1MSA1LjIyNDQwOC0zLjAyNDY1OEM1LjIyNDQwOC0yLjkwNTEwNiA1LjMyMDA1LTIuOTA1MTA2IDUuMzIwMDUtMi44OTMxNTFINS42MTg5MjlDNi41NjMzODctMi44OTMxNTEgNi41NjMzODctMi43OTc1MDkgNi41NjMzODctMi42MTgxODJDNi41NjMzODctMi42MDYyMjcgNi4zMzYyMzktMS4zOTg3NTUgNi4xMDkwOTEtMS4wNDAxQzUuNjU0Nzk1LS4zNzA2MSA0LjcxMDMzNi0uMDk1NjQxIDQuMDA0OTgxLS4wOTU2NDFDMy4wODQ0MzMtLjA5NTY0MSAxLjU5MDAzNy0uNTczODQ4IDEuNTkwMDM3LTIuNjQyMDkyQzEuNTkwMDM3LTMuNDQzMDg4IDEuODc2OTYxLTUuMjcyMjI5IDMuMDM2NjEzLTYuNjIzMTYzQzMuNzg5Nzg4LTcuNDgzOTM1IDQuOTAxNjE5LTguMDY5NzM4IDUuOTUzNjc0LTguMDY5NzM4QzcuMzY0Mzg0LTguMDY5NzM4IDcuODY2NTAxLTYuODYyMjY3IDcuODY2NTAxLTUuNzYyMzkxQzcuODY2NTAxLTUuNTcxMTA4IDcuODE4NjgtNS4zMDgwOTUgNy44MTg2OC01LjE0MDcyMkM3LjgxODY4LTUuMDMzMTI2IDcuOTM4MjMyLTUuMDMzMTI2IDcuOTc0MDk3LTUuMDMzMTI2QzguMTA1NjA0LTUuMDMzMTI2IDguMTE3NTU5LTUuMDQ1MDgxIDguMTY1MzgtNS4yNjAyNzRMOC45MTg1NTUtOC4zMDg4NDJaJy8+CjxwYXRoIGlkPSdnNC0xMjInIGQ9J00xLjUxODMwNi0uOTY4MzY5QzIuMDMyMzc5LTEuNTU0MTcyIDIuNDUwODA5LTEuOTI0NzgyIDMuMDQ4NTY4LTIuNDYyNzY1QzMuNzY1ODc4LTMuMDg0NDMzIDQuMDc2NzEyLTMuMzgzMzEzIDQuMjQ0MDg1LTMuNTYyNjRDNS4wODA5NDYtNC4zODc1NDcgNS40OTkzNzctNS4wODA5NDYgNS40OTkzNzctNS4xNzY1ODhTNS40MDM3MzYtNS4yNzIyMjkgNS4zNzk4MjYtNS4yNzIyMjlDNS4yOTYxMzktNS4yNzIyMjkgNS4yNzIyMjktNS4yMjQ0MDggNS4yMTI0NTMtNS4xNDA3MjJDNC45MTM1NzQtNC42MjY2NSA0LjYyNjY1LTQuMzc1NTkyIDQuMzE1ODE2LTQuMzc1NTkyQzQuMDY0NzU3LTQuMzc1NTkyIDMuOTMzMjUtNC40ODMxODggMy43MDYxMDItNC43NzAxMTJDMy40NTUwNDQtNS4wNjg5OTEgMy4yNTE4MDYtNS4yNzIyMjkgMi45MDUxMDYtNS4yNzIyMjlDMi4wMzIzNzktNS4yNzIyMjkgMS41MDYzNTEtNC4xODQzMDkgMS41MDYzNTEtMy45MzMyNUMxLjUwNjM1MS0zLjg5NzM4NSAxLjUxODMwNi0zLjgyNTY1NCAxLjYyNTkwMy0zLjgyNTY1NEMxLjcyMTU0NC0zLjgyNTY1NCAxLjczMzQ5OS0zLjg3MzQ3NCAxLjc2OTM2NS0zLjk1NzE2MUMxLjk3MjYwMy00LjQzNTM2NyAyLjU0NjQ1MS00LjUxOTA1NCAyLjc3MzU5OS00LjUxOTA1NEMzLjAyNDY1OC00LjUxOTA1NCAzLjI2Mzc2MS00LjQzNTM2NyAzLjUxNDgxOS00LjMyNzc3MUMzLjk2OTExNi00LjEzNjQ4OCA0LjE2MDM5OS00LjEzNjQ4OCA0LjI3OTk1LTQuMTM2NDg4QzQuMzYzNjM2LTQuMTM2NDg4IDQuNDExNDU3LTQuMTM2NDg4IDQuNDcxMjMzLTQuMTQ4NDQzQzQuMDc2NzEyLTMuNjgyMTkyIDMuNDMxMTMzLTMuMTA4MzQ0IDIuODkzMTUxLTIuNjE4MTgyTDEuNjg1Njc5LTEuNTA2MzUxQy45NTY0MTMtLjc2NTEzMSAuNTE0MDcyLS4wNTk3NzYgLjUxNDA3MiAuMDIzOTFDLjUxNDA3MiAuMDk1NjQxIC41NzM4NDggLjExOTU1MiAuNjQ1NTc5IC4xMTk1NTJTLjcyOTI2NSAuMTA3NTk3IC44MTI5NTEtLjAzNTg2NkMxLjAwNDIzNC0uMzM0NzQ1IDEuMzg2OC0uNzc3MDg2IDEuODI5MTQxLS43NzcwODZDMi4wODAxOTktLjc3NzA4NiAyLjE5OTc1MS0uNjkzNCAyLjQzODg1NC0uMzk0NTIxQzIuNjY2MDAyLS4xMzE1MDcgMi44NjkyNCAuMTE5NTUyIDMuMjUxODA2IC4xMTk1NTJDNC40MjM0MTIgLjExOTU1MiA1LjA5MjkwMi0xLjM5ODc1NSA1LjA5MjkwMi0xLjY3MzcyNEM1LjA5MjkwMi0xLjcyMTU0NCA1LjA4MDk0Ni0xLjc5MzI3NSA0Ljk2MTM5NS0xLjc5MzI3NUM0Ljg2NTc1My0xLjc5MzI3NSA0Ljg1Mzc5OC0xLjc0NTQ1NSA0LjgxNzkzMy0xLjYyNTkwM0M0LjU1NDkxOS0uOTIwNTQ4IDMuODQ5NTY0LS42MzM2MjQgMy4zODMzMTMtLjYzMzYyNEMzLjEzMjI1NC0uNjMzNjI0IDIuODkzMTUxLS43MTczMSAyLjY0MjA5Mi0uODI0OTA3QzIuMTYzODg1LTEuMDE2MTg5IDIuMDMyMzc5LTEuMDE2MTg5IDEuODc2OTYxLTEuMDE2MTg5QzEuNzU3NDEtMS4wMTYxODkgMS42MjU5MDMtMS4wMTYxODkgMS41MTgzMDYtLjk2ODM2OVonLz4KPHBhdGggaWQ9J2czLTI0JyBkPSdNMS42MTc5MzMtMi4zNTExODNDMS45MTI4MjctMi4yMzk2MDEgMi4yMDc3MjEtMi4yMzk2MDEgMi4zODMwNjQtMi4yMzk2MDFDMi42NTQwNDctMi4yMzk2MDEgMy4xNzIxMDUtMi4yMzk2MDEgMy4xNzIxMDUtMi41MjY1MjZDMy4xNzIxMDUtMi43NjU2MjkgMi43NDE3MTktMi43NjU2MjkgMi40NzA3MzUtMi43NjU2MjlDMi4zMTEzMzMtMi43NjU2MjkgMi4wNjQyNTktMi43NjU2MjkgMS43NTM0MjUtMi42NjIwMTdDMS41NzgwODItMi44MjkzOSAxLjUwNjM1MS0zLjA1MjU1MyAxLjUwNjM1MS0zLjI3NTcxNkMxLjUwNjM1MS0zLjcyMjA0MiAxLjgxNzE4Ni00LjI4NzkyIDIuMzk5MDA0LTQuNTY2ODc0QzIuNTc0MzQ2LTQuMzgzNTYyIDIuNzgxNTY5LTQuMzgzNTYyIDIuOTQ4OTQxLTQuMzgzNTYyQzMuMjUxODA2LTQuMzgzNTYyIDMuNzA2MTAyLTQuMzk5NTAyIDMuNzA2MTAyLTQuNjcwNDg2QzMuNzA2MTAyLTQuOTA5NTg5IDMuMjc1NzE2LTQuOTA5NTg5IDIuOTk2NzYyLTQuOTA5NTg5QzIuODYxMjctNC45MDk1ODkgMi43MjU3NzgtNC45MDk1ODkgMi41MDI2MTUtNC44Nzc3MDlDMi40ODY2NzUtNC45MzM0OTkgMi40NjI3NjUtNS4wMTMyIDIuNDYyNzY1LTUuMTE2ODEyQzIuNDYyNzY1LTUuMjI4Mzk0IDIuNDk0NjQ1LTUuMzYzODg1IDIuNDk0NjQ1LTUuMzg3Nzk2QzIuNTAyNjE1LTUuMzk1NzY2IDIuNTAyNjE1LTUuNDI3NjQ2IDIuNTAyNjE1LTUuNDM1NjE2QzIuNTAyNjE1LTUuNTA3MzQ3IDIuNDQ2ODI0LTUuNTU1MTY4IDIuMzkxMDM0LTUuNTU1MTY4QzIuMjE1NjkxLTUuNTU1MTY4IDIuMjE1NjkxLTUuMTk2NTEzIDIuMjE1NjkxLTUuMTI0NzgyQzIuMjE1NjkxLTQuOTczMzUgMi4yNTU1NDItNC44Mzc4NTggMi4yNjM1MTItNC44MjE5MThDMS4zNzA4NTktNC41OTA3ODUgLjgyMDkyMi0zLjk1MzE3NiAuODIwOTIyLTMuMzIzNTM3Qy44MjA5MjItMi45MjUwMzEgMS4wMzYxMTUtMi42NTQwNDcgMS4zMzg5NzktMi40Nzg3MDVDLjQ4NjE3Ny0xLjk5MjUyOCAuMTkxMjgzLTEuMTg3NTQ3IC4xOTEyODMtLjgyMDkyMkMuMTkxMjgzLS4wOTU2NDEgLjkyNDUzMyAuMTY3MzcyIDEuMTc5NTc3IC4yNjMwMTRDMS42MjU5MDMgLjQzMDM4NiAxLjY0MTg0MyAuNDMwMzg2IDIuMDMyMzc5IC41NjU4NzhDMi4yMjM2NjEgLjYzNzYwOSAyLjU0MjQ2NiAuNzU3MTYxIDIuNTk4MjU3IC43ODkwNDFDMi43MjU3NzggLjg2ODc0MiAyLjcyNTc3OCAuOTgwMzI0IDIuNzI1Nzc4IDEuMDI4MTQ0QzIuNzI1Nzc4IDEuMTcxNjA2IDIuNjIyMTY3IDEuNDAyNzQgMi4zNjcxMjMgMS40MDI3NEMyLjMwMzM2MiAxLjQwMjc0IDEuOTc2NTg4IDEuMzg2OCAxLjY1Nzc4MyAxLjE5NTUxN0MxLjU3ODA4MiAxLjEzOTcyNiAxLjU3MDExMiAxLjEzMTc1NiAxLjUzMDI2MiAxLjEzMTc1NkMxLjQ0MjU5IDEuMTMxNzU2IDEuNDE4NjggMS4yMTE0NTcgMS40MTg2OCAxLjI0MzMzN0MxLjQxODY4IDEuMzcwODU5IDEuOTI4NzY3IDEuNjI1OTAzIDIuMzc1MDkzIDEuNjI1OTAzQzIuOTAxMTIxIDEuNjI1OTAzIDMuMjI3ODk1IDEuMTIzNzg2IDMuMjI3ODk1IC43NTcxNjFDMy4yMjc4OTUgLjYxMzY5OSAzLjE3MjEwNSAuNDYyMjY3IDMuMDc2NDYzIC4zNTA2ODVDMi45NzI4NTIgLjIzOTEwMyAyLjg2OTI0IC4xOTkyNTMgMi40MjI5MTQgLjAzOTg1MUMxLjcyOTUxNC0uMjA3MjIzIDEuMjExNDU3LS4zOTA1MzUgMS4wODM5MzUtLjQ2MjI2N0MuODI4ODkyLS41OTc3NTggLjY2MTUxOS0uNzg5MDQxIC42NjE1MTktMS4wNTIwNTVDLjY2MTUxOS0xLjM3ODgyOSAuOTU2NDEzLTEuOTkyNTI4IDEuNjE3OTMzLTIuMzUxMTgzWk0zLjQwMzIzOC00LjY0NjU3NUMzLjMyMzUzNy00LjYzMDYzNSAzLjI0MzgzNi00LjYwNjcyNSAyLjk1NjkxMi00LjYwNjcyNUMyLjc4OTUzOS00LjYwNjcyNSAyLjc1NzY1OS00LjYwNjcyNSAyLjY2MjAxNy00LjY1NDU0NUMyLjc4OTUzOS00LjY4NjQyNiAyLjg2OTI0LTQuNjg2NDI2IDMuMDEyNzAyLTQuNjg2NDI2QzMuMjI3ODk1LTQuNjg2NDI2IDMuMjgzNjg2LTQuNjc4NDU2IDMuNDAzMjM4LTQuNjU0NTQ1Vi00LjY0NjU3NVpNMi44NjkyNC0yLjUwMjYxNUMyLjc5NzUwOS0yLjQ4NjY3NSAyLjcxNzgwOC0yLjQ2Mjc2NSAyLjQwNjk3NC0yLjQ2Mjc2NUMyLjI1NTU0Mi0yLjQ2Mjc2NSAyLjE3NTg0MS0yLjQ2Mjc2NSAyLjA0ODMxOS0yLjUwMjYxNUMyLjIyMzY2MS0yLjU0MjQ2NiAyLjMxOTMwMy0yLjU0MjQ2NiAyLjQ2Mjc2NS0yLjU0MjQ2NkMyLjY5Mzg5OC0yLjU0MjQ2NiAyLjc1NzY1OS0yLjUzNDQ5NiAyLjg2OTI0LTIuNTEwNTg1Vi0yLjUwMjYxNVonLz4KPHBhdGggaWQ9J2czLTYxJyBkPSdNMy43MDYxMDItNS42NDI4MzlDMy43NTM5MjMtNS43NTQ0MjEgMy43NTM5MjMtNS43NzAzNjEgMy43NTM5MjMtNS43OTQyNzFDMy43NTM5MjMtNS44OTc4ODMgMy42NzQyMjItNS45Nzc1ODQgMy41NzA2MS01Ljk3NzU4NEMzLjQ0MzA4OC01Ljk3NzU4NCAzLjQxMTIwOC01Ljg4MTk0MyAzLjM3OTMyOC01LjgwMjI0MkwuNTE4MDU3IDEuNjU3NzgzQy40NzAyMzcgMS43NjkzNjUgLjQ3MDIzNyAxLjc4NTMwNSAuNDcwMjM3IDEuODA5MjE1Qy40NzAyMzcgMS45MTI4MjcgLjU0OTkzOCAxLjk5MjUyOCAuNjUzNTQ5IDEuOTkyNTI4Qy43ODEwNzEgMS45OTI1MjggLjgxMjk1MSAxLjg5Njg4NyAuODQ0ODMyIDEuODE3MTg2TDMuNzA2MTAyLTUuNjQyODM5WicvPgo8cGF0aCBpZD0nZzYtNDAnIGQ9J00zLjg4NTQzIDIuOTA1MTA2QzMuODg1NDMgMi44NjkyNCAzLjg4NTQzIDIuODQ1MzMgMy42ODIxOTIgMi42NDIwOTJDMi40ODY2NzUgMS40MzQ2MiAxLjgxNzE4Ni0uNTM3OTgzIDEuODE3MTg2LTIuOTc2ODM3QzEuODE3MTg2LTUuMjk2MTM5IDIuMzc5MDc4LTcuMjkyNjUzIDMuNzY1ODc4LTguNzAzMzYyQzMuODg1NDMtOC44MTA5NTkgMy44ODU0My04LjgzNDg2OSAzLjg4NTQzLTguODcwNzM1QzMuODg1NDMtOC45NDI0NjYgMy44MjU2NTQtOC45NjYzNzYgMy43Nzc4MzMtOC45NjYzNzZDMy42MjI0MTYtOC45NjYzNzYgMi42NDIwOTItOC4xMDU2MDQgMi4wNTYyODktNi45MzM5OThDMS40NDY1NzUtNS43MjY1MjYgMS4xNzE2MDYtNC40NDczMjMgMS4xNzE2MDYtMi45NzY4MzdDMS4xNzE2MDYtMS45MTI4MjcgMS4zMzg5NzktLjQ5MDE2MiAxLjk2MDY0OCAuNzg5MDQxQzIuNjY2MDAyIDIuMjIzNjYxIDMuNjQ2MzI2IDMuMDAwNzQ3IDMuNzc3ODMzIDMuMDAwNzQ3QzMuODI1NjU0IDMuMDAwNzQ3IDMuODg1NDMgMi45NzY4MzcgMy44ODU0MyAyLjkwNTEwNlonLz4KPHBhdGggaWQ9J2c2LTQxJyBkPSdNMy4zNzEzNTctMi45NzY4MzdDMy4zNzEzNTctMy44ODU0MyAzLjI1MTgwNi01LjM2Nzg3IDIuNTgyMzE2LTYuNzU0NjdDMS44NzY5NjEtOC4xODkyOSAuODk2NjM4LTguOTY2Mzc2IC43NjUxMzEtOC45NjYzNzZDLjcxNzMxLTguOTY2Mzc2IC42NTc1MzQtOC45NDI0NjYgLjY1NzUzNC04Ljg3MDczNUMuNjU3NTM0LTguODM0ODY5IC42NTc1MzQtOC44MTA5NTkgLjg2MDc3Mi04LjYwNzcyMUMyLjA1NjI4OS03LjQwMDI0OSAyLjcyNTc3OC01LjQyNzY0NiAyLjcyNTc3OC0yLjk4ODc5MkMyLjcyNTc3OC0uNjY5NDg5IDIuMTYzODg1IDEuMzI3MDI0IC43NzcwODYgMi43Mzc3MzNDLjY1NzUzNCAyLjg0NTMzIC42NTc1MzQgMi44NjkyNCAuNjU3NTM0IDIuOTA1MTA2Qy42NTc1MzQgMi45NzY4MzcgLjcxNzMxIDMuMDAwNzQ3IC43NjUxMzEgMy4wMDA3NDdDLjkyMDU0OCAzLjAwMDc0NyAxLjkwMDg3MiAyLjEzOTk3NSAyLjQ4NjY3NSAuOTY4MzY5QzMuMDk2Mzg5LS4yNTEwNTkgMy4zNzEzNTctMS41NDIyMTcgMy4zNzEzNTctMi45NzY4MzdaJy8+CjxwYXRoIGlkPSdnNi00OScgZD0nTTMuNDQzMDg4LTcuNjYzMjYzQzMuNDQzMDg4LTcuOTM4MjMyIDMuNDQzMDg4LTcuOTUwMTg3IDMuMjAzOTg1LTcuOTUwMTg3QzIuOTE3MDYxLTcuNjI3Mzk3IDIuMzE5MzAzLTcuMTg1MDU2IDEuMDg3OTItNy4xODUwNTZWLTYuODM4MzU2QzEuMzYyODg5LTYuODM4MzU2IDEuOTYwNjQ4LTYuODM4MzU2IDIuNjE4MTgyLTcuMTQ5MTkxVi0uOTIwNTQ4QzIuNjE4MTgyLS40OTAxNjIgMi41ODIzMTYtLjM0NjcgMS41MzAyNjItLjM0NjdIMS4xNTk2NTFWMEMxLjQ4MjQ0MS0uMDIzOTEgMi42NDIwOTItLjAyMzkxIDMuMDM2NjEzLS4wMjM5MVM0LjU3ODgyOS0uMDIzOTEgNC45MDE2MTkgMFYtLjM0NjdINC41MzEwMDlDMy40Nzg5NTQtLjM0NjcgMy40NDMwODgtLjQ5MDE2MiAzLjQ0MzA4OC0uOTIwNTQ4Vi03LjY2MzI2M1onLz4KPHBhdGggaWQ9J2c2LTYxJyBkPSdNOC4wNjk3MzgtMy44NzM0NzRDOC4yMzcxMTEtMy44NzM0NzQgOC40NTIzMDQtMy44NzM0NzQgOC40NTIzMDQtNC4wODg2NjdDOC40NTIzMDQtNC4zMTU4MTYgOC4yNDkwNjYtNC4zMTU4MTYgOC4wNjk3MzgtNC4zMTU4MTZIMS4wMjgxNDRDLjg2MDc3Mi00LjMxNTgxNiAuNjQ1NTc5LTQuMzE1ODE2IC42NDU1NzktNC4xMDA2MjNDLjY0NTU3OS0zLjg3MzQ3NCAuODQ4ODE3LTMuODczNDc0IDEuMDI4MTQ0LTMuODczNDc0SDguMDY5NzM4Wk04LjA2OTczOC0xLjY0OTgxM0M4LjIzNzExMS0xLjY0OTgxMyA4LjQ1MjMwNC0xLjY0OTgxMyA4LjQ1MjMwNC0xLjg2NTAwNkM4LjQ1MjMwNC0yLjA5MjE1NCA4LjI0OTA2Ni0yLjA5MjE1NCA4LjA2OTczOC0yLjA5MjE1NEgxLjAyODE0NEMuODYwNzcyLTIuMDkyMTU0IC42NDU1NzktMi4wOTIxNTQgLjY0NTU3OS0xLjg3Njk2MUMuNjQ1NTc5LTEuNjQ5ODEzIC44NDg4MTctMS42NDk4MTMgMS4wMjgxNDQtMS42NDk4MTNIOC4wNjk3MzhaJy8+CjxwYXRoIGlkPSdnNi0xMDEnIGQ9J000LjU3ODgyOS0yLjc3MzU5OUM0Ljg0MTg0My0yLjc3MzU5OSA0Ljg2NTc1My0yLjc3MzU5OSA0Ljg2NTc1My0zLjAwMDc0N0M0Ljg2NTc1My00LjIwODIxOSA0LjIyMDE3NC01LjMzMjAwNSAyLjc3MzU5OS01LjMzMjAwNUMxLjQxMDcxLTUuMzMyMDA1IC4zNTg2NTUtNC4xMDA2MjMgLjM1ODY1NS0yLjYxODE4MkMuMzU4NjU1LTEuMDQwMSAxLjU3ODA4MiAuMTE5NTUyIDIuOTA1MTA2IC4xMTk1NTJDNC4zMjc3NzEgLjExOTU1MiA0Ljg2NTc1My0xLjE3MTYwNiA0Ljg2NTc1My0xLjQyMjY2NUM0Ljg2NTc1My0xLjQ5NDM5NiA0LjgwNTk3OC0xLjU0MjIxNyA0LjczNDI0Ny0xLjU0MjIxN0M0LjYzODYwNS0xLjU0MjIxNyA0LjYxNDY5NS0xLjQ4MjQ0MSA0LjU5MDc4NS0xLjQyMjY2NUM0LjI3OTk1LS40MTg0MzEgMy40Nzg5NTQtLjE0MzQ2MiAyLjk3NjgzNy0uMTQzNDYyUzEuMjY3MjQ4LS40NzgyMDcgMS4yNjcyNDgtMi41NDY0NTFWLTIuNzczNTk5SDQuNTc4ODI5Wk0xLjI3OTIwMy0zLjAwMDc0N0MxLjM3NDg0NC00Ljg3NzcwOSAyLjQyNjg5OS01LjA5MjkwMiAyLjc2MTY0NC01LjA5MjkwMkM0LjA0MDg0Ny01LjA5MjkwMiA0LjExMjU3OC0zLjQwNzIyMyA0LjEyNDUzMy0zLjAwMDc0N0gxLjI3OTIwM1onLz4KPHBhdGggaWQ9J2c2LTExMicgZD0nTTIuOTI5MDE2IDEuOTcyNjAzQzIuMTYzODg1IDEuOTcyNjAzIDIuMDIwNDIzIDEuOTcyNjAzIDIuMDIwNDIzIDEuNDM0NjJWLS42NDU1NzlDMi4yMzU2MTYtLjM0NjcgMi43MjU3NzggLjExOTU1MiAzLjQ5MDkwOSAuMTE5NTUyQzQuODY1NzUzIC4xMTk1NTIgNi4wNzMyMjUtMS4wNDAxIDYuMDczMjI1LTIuNTgyMzE2QzYuMDczMjI1LTQuMTAwNjIzIDQuOTQ5NDQtNS4yNzIyMjkgMy42NDYzMjYtNS4yNzIyMjlDMi41OTQyNzEtNS4yNzIyMjkgMi4wMzIzNzktNC41MTkwNTQgMS45OTY1MTMtNC40NzEyMzNWLTUuMjcyMjI5TC4zMzQ3NDUtNS4xNDA3MjJWLTQuNzk0MDIyQzEuMTcxNjA2LTQuNzk0MDIyIDEuMjQzMzM3LTQuNzEwMzM2IDEuMjQzMzM3LTQuMTg0MzA5VjEuNDM0NjJDMS4yNDMzMzcgMS45NzI2MDMgMS4xMTE4MzEgMS45NzI2MDMgLjMzNDc0NSAxLjk3MjYwM1YyLjMxOTMwM0MuNjQ1NTc5IDIuMjk1MzkyIDEuMjkxMTU4IDIuMjk1MzkyIDEuNjI1OTAzIDIuMjk1MzkyQzEuOTcyNjAzIDIuMjk1MzkyIDIuNjE4MTgyIDIuMjk1MzkyIDIuOTI5MDE2IDIuMzE5MzAzVjEuOTcyNjAzWk0yLjAyMDQyMy0zLjgxMzY5OUMyLjAyMDQyMy00LjA0MDg0NyAyLjAyMDQyMy00LjA1MjgwMiAyLjE1MTkzLTQuMjQ0MDg1QzIuNTEwNTg1LTQuNzgyMDY3IDMuMDk2Mzg5LTUuMDA5MjE1IDMuNTUwNjg1LTUuMDA5MjE1QzQuNDQ3MzIzLTUuMDA5MjE1IDUuMTY0NjMzLTMuOTIxMjk1IDUuMTY0NjMzLTIuNTgyMzE2QzUuMTY0NjMzLTEuMTU5NjUxIDQuMzUxNjgxLS4xMTk1NTIgMy40MzExMzMtLjExOTU1MkMzLjA2MDUyMy0uMTE5NTUyIDIuNzEzODIzLS4yNzQ5NjkgMi40NzQ3Mi0uNTAyMTE3QzIuMTk5NzUxLS43NzcwODYgMi4wMjA0MjMtMS4wMTYxODkgMi4wMjA0MjMtMS4zNTA5MzRWLTMuODEzNjk5WicvPgo8cGF0aCBpZD0nZzYtMTIwJyBkPSdNMy4zNDc0NDctMi44MjE0MkMzLjY5NDE0Ny0zLjI3NTcxNiA0LjE5NjI2NC0zLjkyMTI5NSA0LjQyMzQxMi00LjE3MjM1NEM0LjkxMzU3NC00LjcyMjI5MSA1LjQ3NTQ2Ny00LjgwNTk3OCA1Ljg1ODAzMi00LjgwNTk3OFYtNS4xNTI2NzdDNS4zNDM5Ni01LjEyODc2NyA1LjMyMDA1LTUuMTI4NzY3IDQuODUzNzk4LTUuMTI4NzY3QzQuMzk5NTAyLTUuMTI4NzY3IDQuMzc1NTkyLTUuMTI4NzY3IDMuNzc3ODMzLTUuMTUyNjc3Vi00LjgwNTk3OEMzLjkzMzI1LTQuNzgyMDY3IDQuMTI0NTMzLTQuNzEwMzM2IDQuMTI0NTMzLTQuNDM1MzY3QzQuMTI0NTMzLTQuMjMyMTMgNC4wMTY5MzYtNC4xMDA2MjMgMy45NDUyMDUtNC4wMDQ5ODFMMy4xODAwNzUtMy4wMzY2MTNMMi4yNDc1NzItNC4yNjc5OTVDMi4yMTE3MDYtNC4zMTU4MTYgMi4xMzk5NzUtNC40MjM0MTIgMi4xMzk5NzUtNC41MDcwOThDMi4xMzk5NzUtNC41Nzg4MjkgMi4xOTk3NTEtNC43OTQwMjIgMi41NTg0MDYtNC44MDU5NzhWLTUuMTUyNjc3QzIuMjU5NTI3LTUuMTI4NzY3IDEuNjQ5ODEzLTUuMTI4NzY3IDEuMzI3MDI0LTUuMTI4NzY3Qy45MzI1MDMtNS4xMjg3NjcgLjkwODU5My01LjEyODc2NyAuMTc5MzI4LTUuMTUyNjc3Vi00LjgwNTk3OEMuNzg5MDQxLTQuODA1OTc4IDEuMDE2MTg5LTQuNzgyMDY3IDEuMjY3MjQ4LTQuNDU5Mjc4TDIuNjY2MDAyLTIuNjMwMTM3QzIuNjg5OTEzLTIuNjA2MjI3IDIuNzM3NzMzLTIuNTM0NDk2IDIuNzM3NzMzLTIuNDk4NjNTMS44MDUyMy0xLjI5MTE1OCAxLjY4NTY3OS0xLjEzNTc0MUMxLjE1OTY1MS0uNDkwMTYyIC42MzM2MjQtLjM1ODY1NSAuMTE5NTUyLS4zNDY3VjBDLjU3Mzg0OC0uMDIzOTEgLjU5Nzc1OC0uMDIzOTEgMS4xMTE4MzEtLjAyMzkxQzEuNTY2MTI3LS4wMjM5MSAxLjU5MDAzNy0uMDIzOTEgMi4xODc3OTYgMFYtLjM0NjdDMS45MDA4NzItLjM4MjU2NSAxLjg1MzA1MS0uNTYxODkzIDEuODUzMDUxLS43MjkyNjVDMS44NTMwNTEtLjkyMDU0OCAxLjkzNjczNy0xLjAxNjE4OSAyLjA1NjI4OS0xLjE3MTYwNkMyLjIzNTYxNi0xLjQyMjY2NSAyLjYzMDEzNy0xLjkxMjgyNyAyLjkxNzA2MS0yLjI4MzQzN0wzLjg5NzM4NS0xLjAwNDIzNEM0LjEwMDYyMy0uNzQxMjIgNC4xMDA2MjMtLjcxNzMxIDQuMTAwNjIzLS42NDU1NzlDNC4xMDA2MjMtLjU0OTkzOCA0LjAwNDk4MS0uMzU4NjU1IDMuNjgyMTkyLS4zNDY3VjBDMy45OTMwMjYtLjAyMzkxIDQuNTc4ODI5LS4wMjM5MSA0LjkxMzU3NC0uMDIzOTFDNS4zMDgwOTUtLjAyMzkxIDUuMzMyMDA1LS4wMjM5MSA2LjA0OTMxNSAwVi0uMzQ2N0M1LjQxNTY5MS0uMzQ2NyA1LjIwMDQ5OC0uMzcwNjEgNC45MTM1NzQtLjc1MzE3NkwzLjM0NzQ0Ny0yLjgyMTQyWicvPgo8cGF0aCBpZD0nZzYtMTI2JyBkPSdNNC42OTgzODEtNy45MzgyMzJDNC4zNTE2ODEtNy41OTE1MzIgNC4xMDA2MjMtNy4zNTI0MjggMy43MTgwNTctNy4zNTI0MjhDMy41Mzg3My03LjM1MjQyOCAzLjM3MTM1Ny03LjM4ODI5NCAzLjAwMDc0Ny03LjYzOTM1MkMyLjc2MTY0NC03Ljc4MjgxNCAyLjUyMjU0LTcuOTM4MjMyIDIuMjQ3NTcyLTcuOTM4MjMyQzEuODA1MjMtNy45MzgyMzIgMS41NDIyMTctNy42MzkzNTIgLjk4MDMyNC03LjAxNzY4NEwxLjE0NzY5Ni02Ljg1MDMxMUMxLjQ5NDM5Ni03LjE5NzAxMSAxLjc0NTQ1NS03LjQzNjExNSAyLjEyODAyLTcuNDM2MTE1QzIuMzA3MzQ3LTcuNDM2MTE1IDIuNDc0NzItNy40MDAyNDkgMi44NDUzMy03LjE0OTE5MUMzLjA4NDQzMy03LjAwNTcyOSAzLjMyMzUzNy02Ljg1MDMxMSAzLjU5ODUwNi02Ljg1MDMxMUM0LjA0MDg0Ny02Ljg1MDMxMSA0LjMwMzg2MS03LjE0OTE5MSA0Ljg2NTc1My03Ljc3MDg1OUw0LjY5ODM4MS03LjkzODIzMlonLz4KPC9kZWZzPgo8ZyBpZD0ncGFnZTEnPgo8dXNlIHg9JzUyLjczNDI4NCcgeT0nLTE3Ljk2NjEzNScgeGxpbms6aHJlZj0nI2c2LTEyNicvPgo8dXNlIHg9JzUwLjA2ODQ2OScgeT0nLTE0Ljk0NDE0MycgeGxpbms6aHJlZj0nI2c0LTcxJy8+Cjx1c2UgeD0nNTkuMzAyMDkyJyB5PSctMTQuOTQ0MTQzJyB4bGluazpocmVmPScjZzYtNDAnLz4KPHVzZSB4PSc2My44NTQ0MTgnIHk9Jy0xNC45NDQxNDMnIHhsaW5rOmhyZWY9JyNnNC0xMjInLz4KPHVzZSB4PSc2OS44MjUwMjQnIHk9Jy0xNC45NDQxNDMnIHhsaW5rOmhyZWY9JyNnNi00MScvPgo8dXNlIHg9Jzc3LjY5ODE4JyB5PSctMTQuOTQ0MTQzJyB4bGluazpocmVmPScjZzYtNjEnLz4KPHVzZSB4PSc5MC4xMjM2NicgeT0nLTE0Ljk0NDE0MycgeGxpbms6aHJlZj0nI2c2LTQ5Jy8+Cjx1c2UgeD0nOTguNjMzMzE0JyB5PSctMTQuOTQ0MTQzJyB4bGluazpocmVmPScjZzItMCcvPgo8dXNlIHg9JzExMC41ODg0NzUnIHk9Jy0xNC45NDQxNDMnIHhsaW5rOmhyZWY9JyNnNC03MScvPgo8dXNlIHg9JzExOS44MjIwOTgnIHk9Jy0xNC45NDQxNDMnIHhsaW5rOmhyZWY9JyNnNi00MCcvPgo8dXNlIHg9JzEyNC4zNzQ0MjQnIHk9Jy0xNC45NDQxNDMnIHhsaW5rOmhyZWY9JyNnMi0wJy8+Cjx1c2UgeD0nMTMzLjY3MjkyMScgeT0nLTE0Ljk0NDE0MycgeGxpbms6aHJlZj0nI2c0LTEyMicvPgo8dXNlIHg9JzEzOS42NDM1MjcnIHk9Jy0xNC45NDQxNDMnIHhsaW5rOmhyZWY9JyNnNi00MScvPgo8dXNlIHg9JzE0Ny41MTY2ODInIHk9Jy0xNC45NDQxNDMnIHhsaW5rOmhyZWY9JyNnNi02MScvPgo8dXNlIHg9JzE1OS45NDIxNjMnIHk9Jy0xNC45NDQxNDMnIHhsaW5rOmhyZWY9JyNnNi00OScvPgo8dXNlIHg9JzE2OC40NTE4MTcnIHk9Jy0xNC45NDQxNDMnIHhsaW5rOmhyZWY9JyNnMi0wJy8+Cjx1c2UgeD0nMTgwLjQwNjk3OCcgeT0nLTE0Ljk0NDE0MycgeGxpbms6aHJlZj0nI2c2LTEwMScvPgo8dXNlIHg9JzE4NS42MDk2MzYnIHk9Jy0xNC45NDQxNDMnIHhsaW5rOmhyZWY9JyNnNi0xMjAnLz4KPHVzZSB4PScxOTEuNzg3NzkyJyB5PSctMTQuOTQ0MTQzJyB4bGluazpocmVmPScjZzYtMTEyJy8+Cjx1c2UgeD0nMjAwLjI4MzYxMicgeT0nLTM1LjM4NzY2NycgeGxpbms6aHJlZj0nI2cwLTMyJy8+Cjx1c2UgeD0nMjA5Ljc0ODE1MScgeT0nLTE0Ljk0NDE0MycgeGxpbms6aHJlZj0nI2cyLTAnLz4KPHVzZSB4PScyMjEuMDM5MTQ1JyB5PSctMzEuODAxMDgnIHhsaW5rOmhyZWY9JyNnMC0yMCcvPgo8dXNlIHg9JzIyNy4zNDg4NDMnIHk9Jy0xNC45NDQxNDMnIHhsaW5rOmhyZWY9JyNnNi00OScvPgo8dXNlIHg9JzIzNS44NTg0OTYnIHk9Jy0xNC45NDQxNDMnIHhsaW5rOmhyZWY9JyNnMi0wJy8+Cjx1c2UgeD0nMjQ5LjAzMzA1MycgeT0nLTE4LjA5ODk1MycgeGxpbms6aHJlZj0nI2c2LTEyNicvPgo8dXNlIHg9JzI0Ny44MTM2NTcnIHk9Jy0xNC45NDQxNDMnIHhsaW5rOmhyZWY9JyNnNC0yNCcvPgo8dXNlIHg9JzI1NS40OTY1OTInIHk9Jy0zMS44MDEwOCcgeGxpbms6aHJlZj0nI2cwLTE4Jy8+Cjx1c2UgeD0nMjY1LjQ5MjQ3OCcgeT0nLTIzLjAzMTkwMScgeGxpbms6aHJlZj0nI2c0LTEyMicvPgo8dXNlIHg9JzI3NC4xMTk3NDgnIHk9Jy0yMy4wMzE5MDEnIHhsaW5rOmhyZWY9JyNnMi0wJy8+Cjx1c2UgeD0nMjg2Ljk5NTA3MycgeT0nLTIzLjAzMTkwMScgeGxpbms6aHJlZj0nI2c2LTEyNicvPgo8dXNlIHg9JzI4Ni4wNzQ5MDknIHk9Jy0yMy4wMzE5MDEnIHhsaW5rOmhyZWY9JyNnNC0yMicvPgo8cmVjdCB4PScyNjUuNDkyNDc4JyB5PSctMTguMTcyMDI4JyBoZWlnaHQ9Jy40NzgxODcnIHdpZHRoPScyNy42MjUzOTMnLz4KPHVzZSB4PScyNzYuMzc4Njg4JyB5PSctNi43NDM0OCcgeGxpbms6aHJlZj0nI2c2LTEyNicvPgo8dXNlIHg9JzI3NS43NjM5NzMnIHk9Jy02Ljc0MzQ4JyB4bGluazpocmVmPScjZzQtMjcnLz4KPHVzZSB4PScyOTQuMzEzMzg2JyB5PSctMzEuODAxMDgnIHhsaW5rOmhyZWY9JyNnMC0xOScvPgo8dXNlIHg9JzMwMy4xMTM3NTgnIHk9Jy0zMS44MDEwOCcgeGxpbms6aHJlZj0nI2cwLTIxJy8+Cjx1c2UgeD0nMzA5LjQyMzQ0OCcgeT0nLTI5LjEyNDQyNicgeGxpbms6aHJlZj0nI2cxLTAnLz4KPHVzZSB4PSczMTYuMDA5OTU1JyB5PSctMjkuMTI0NDI2JyB4bGluazpocmVmPScjZzUtNDknLz4KPHVzZSB4PSczMjAuMjQ0MTM4JyB5PSctMjkuMTI0NDI2JyB4bGluazpocmVmPScjZzMtNjEnLz4KPHVzZSB4PSczMjUuMzE4OTMzJyB5PSctMzEuMjI3NjUzJyB4bGluazpocmVmPScjZzUtMTI2Jy8+Cjx1c2UgeD0nMzI0LjQ3ODMyJyB5PSctMjkuMTI0NDI2JyB4bGluazpocmVmPScjZzMtMjQnLz4KPHVzZSB4PSczMjkuMDA5OTg3JyB5PSctMzUuMzg3NjY3JyB4bGluazpocmVmPScjZzAtMzMnLz4KPC9nPgo8L3N2Zz4KPCEtLSBERVBUSD0wIC0tPg==)

for all  such that

such that  .

.

In that example, we model the  variable which is the annual maximum of the opposite race times.

variable which is the annual maximum of the opposite race times.

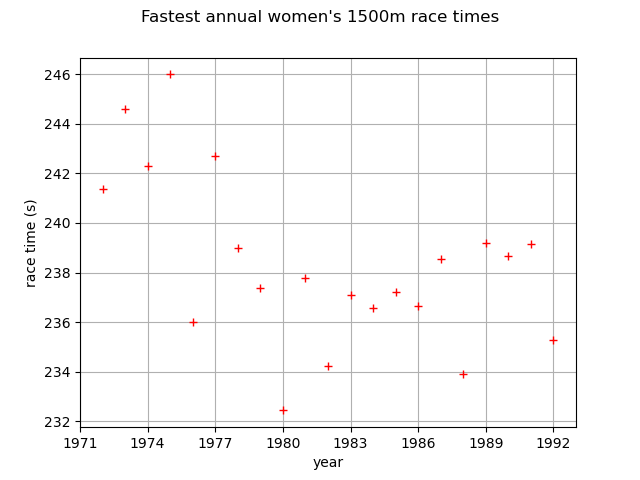

First, we load the race times dataset. We start by looking at them through time.

import openturns as ot

import openturns.viewer as otv

import openturns.experimental as otexp

from openturns.usecases import coles

data = coles.Coles().racetime

print(data[:5])

graph = ot.Graph(

"Fastest annual women's 1500m race times", "year", "race time (s)", True, ""

)

cloud = ot.Cloud(data[:, :2])

cloud.setColor("red")

graph.add(cloud)

graph.setIntegerXTick(True)

view = otv.View(graph)

[ Year Race time ]

0 : [ 1972 241.371 ]

1 : [ 1973 244.616 ]

2 : [ 1974 242.301 ]

3 : [ 1975 246 ]

4 : [ 1976 235.994 ]

We select the race times column. We transform them into their opposite values.

sample = -1.0 * data[:, 1]

Stationary GEV modeling via the log-likelihood function

We first assume that the dependence through time is negligible, so we first model the data as independent observations over the observation period. We estimate the parameters of the GEV distribution by maximizing the log-likelihood of the data.

factory = ot.GeneralizedExtremeValueFactory()

result_LL = factory.buildMethodOfLikelihoodMaximizationEstimator(sample)

We get the fitted GEV for the variable and its parameters

.

.

fitted_GEV = result_LL.getDistribution()

desc = fitted_GEV.getParameterDescription()

param = fitted_GEV.getParameter()

print(", ".join([f"{p}: {value:.3f}" for p, value in zip(desc, param)]))

mu: -239.260, sigma: 3.643, xi: -0.470

We get the asymptotic distribution of the estimator .

In that case, the asymptotic distribution is normal.

parameterEstimate = result_LL.getParameterDistribution()

print("Asymptotic distribution of the estimator : ")

print(parameterEstimate)

Asymptotic distribution of the estimator :

Normal(mu = [-239.26,3.64268,-0.469834], sigma = [0.891274,0.778059,0.236181], R = [[ 1 -0.113124 -0.406653 ]

[ -0.113124 1 -0.706993 ]

[ -0.406653 -0.706993 1 ]])

We get the covariance matrix and the standard deviation of .

print("Cov matrix = \n", parameterEstimate.getCovariance())

print("Standard dev = ", parameterEstimate.getStandardDeviation())

Cov matrix =

[[ 0.79437 -0.0784475 -0.0856013 ]

[ -0.0784475 0.605376 -0.129919 ]

[ -0.0856013 -0.129919 0.0557815 ]]

Standard dev = [0.891274,0.778059,0.236181]

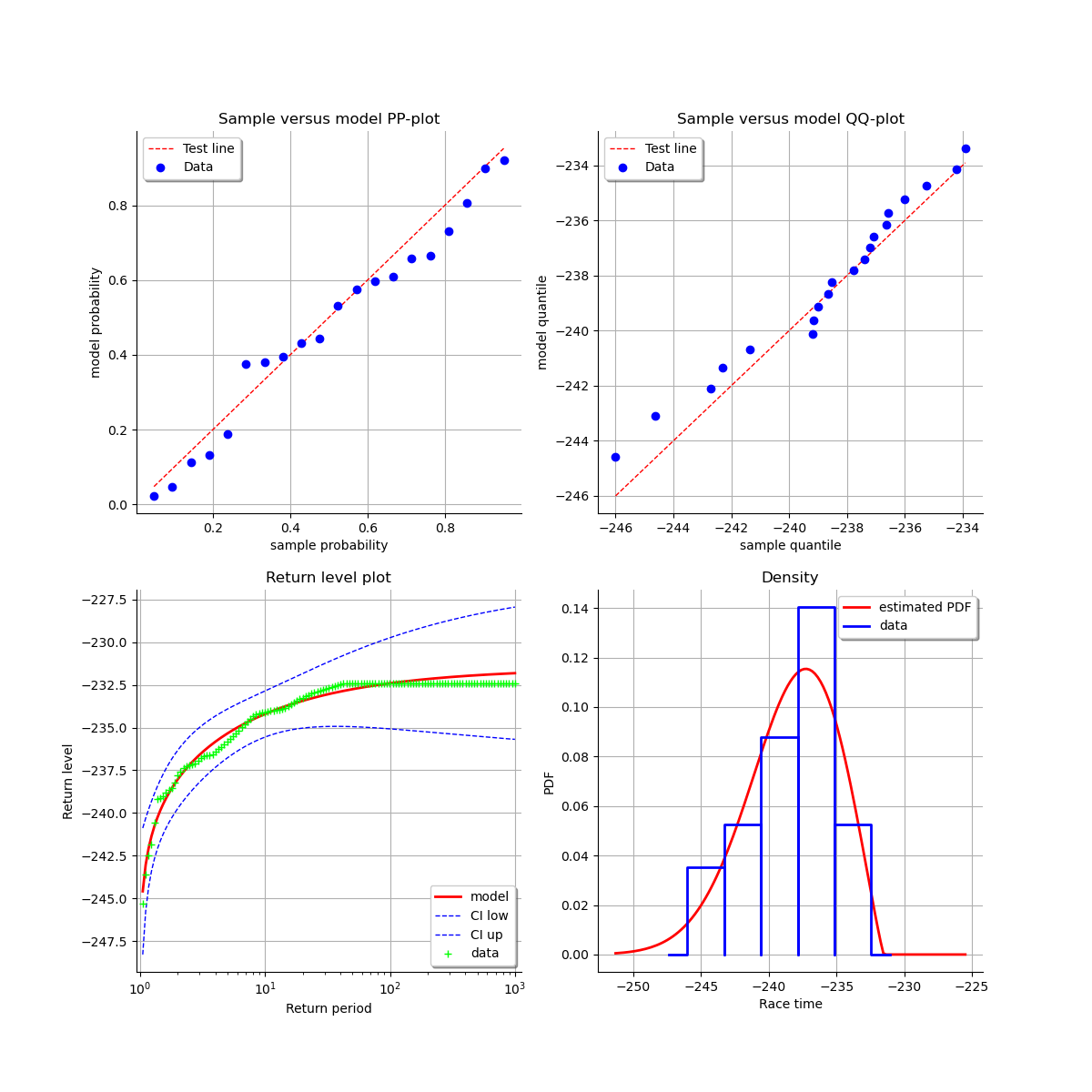

At last, we can validate the inference result thanks the 4 usual diagnostic plots:

the probability-probability pot,

the quantile-quantile pot,

the return level plot,

the data histogram and the density of the fitted model.

validation = otexp.GeneralizedExtremeValueValidation(result_LL, sample)

graph = validation.drawDiagnosticPlot()

view = otv.View(graph)

Stationary GEV modeling via the profile log-likelihood function

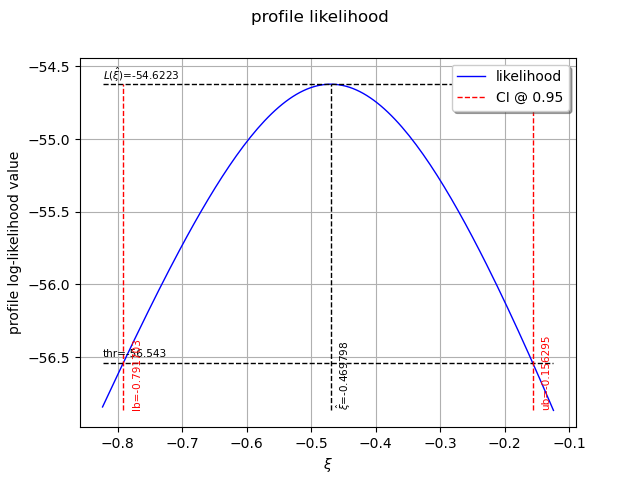

Now, we use the profile log-likehood function rather than log-likehood function to estimate the parameters of the GEV.

result_PLL = factory.buildMethodOfProfileLikelihoodMaximizationEstimator(sample)

The following graph allows one to get the profile log-likelihood plot.

It also indicates the optimal value of  , the maximum profile log-likelihood and

the confidence interval for of order 0.95 (which is the default value).

, the maximum profile log-likelihood and

the confidence interval for of order 0.95 (which is the default value).

order = 0.95

result_PLL.setConfidenceLevel(order)

view = otv.View(result_PLL.drawProfileLikelihoodFunction())

We can get the numerical values of the confidence interval: it appears to be a bit smaller with the interval obtained from the profile log-likelihood function than with the log-likelihood function. Note that if the order requested is too high, the confidence interval might not be calculated because one of its bound is out of the definition domain of the log-likelihood function.

try:

print("Confidence interval for xi = ", result_PLL.getParameterConfidenceInterval())

except Exception as ex:

print(type(ex))

pass

Confidence interval for xi = [-0.791703, -0.156295]

Return level estimate from the estimated stationary GEV

We estimate the  -block return level

-block return level  : it is computed as a particular quantile of the

GEV model estimated using the log-likelihood function. We just have to use the maximum log-likelihood

estimator built in the previous section.

The return level of and have opposite values.

: it is computed as a particular quantile of the

GEV model estimated using the log-likelihood function. We just have to use the maximum log-likelihood

estimator built in the previous section.

The return level of and have opposite values.

As the data are annual sea-levels, each block corresponds to one year: the 10-year return level

corresponds to  and the 100-year return level corresponds to

and the 100-year return level corresponds to  .

.

The method provides the asymptotic distribution of the estimator  of

which mean is the return-level estimate.

of

which mean is the return-level estimate.

zm_10 = factory.buildReturnLevelEstimator(result_LL, 10.0)

return_level_10 = zm_10.getMean()

print("Maximum log-likelihood function : ")

print(f"10-year return level={return_level_10}")

return_level_ci10 = zm_10.computeBilateralConfidenceInterval(0.95)

print(f"CI={return_level_ci10}")

Maximum log-likelihood function :

10-year return level=[-234.2]

CI=[-235.552, -232.849]

zm_100 = factory.buildReturnLevelEstimator(result_LL, 100.0)

return_level_100 = zm_100.getMean()

print(f"100-year return level={return_level_100}")

return_level_ci100 = zm_100.computeBilateralConfidenceInterval(0.95)

print(f"CI={return_level_ci100}")

100-year return level=[-232.4]

CI=[-235.071, -229.729]

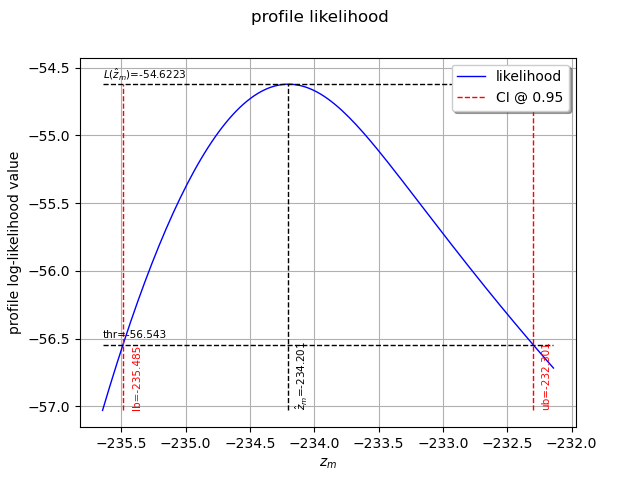

Return level estimate via the profile log-likelihood function of a stationary GEV

We can estimate the -block return level directly from the data using the profile

likelihood with respect to .

result_zm_10_PLL = factory.buildReturnLevelProfileLikelihoodEstimator(sample, 10.0)

zm_10_PLL = result_zm_10_PLL.getParameter()

print(f"10 years return level (profile)={zm_10_PLL}")

10 years return level (profile)=-234.20091228177077

We can get the confidence interval of : once more, it appears to be a bit smaller

than the interval obtained from the log-likelihood function.

As for the confidence interval of , dependeding on the order requested, the interval might

not be calculated.

result_zm_10_PLL.setConfidenceLevel(0.95)

try:

return_level_ci10 = result_zm_10_PLL.getParameterConfidenceInterval()

except Exception as ex:

print(type(ex))

pass

print("Maximum profile log-likelihood function : ")

print(f"CI={return_level_ci10}")

Maximum profile log-likelihood function :

CI=[-235.485, -232.301]

We can also plot the profile log-likelihood function and get the confidence interval, the optimal value

of and its confidence interval.

view = otv.View(result_zm_10_PLL.drawProfileLikelihoodFunction())

Non stationary GEV modeling via the log-likelihood function

If we look at the data carefully, we see that the pattern of variation has not remained constant over the observation period. There is an increase in the data through time. We want to model this trend because a slight increase in extreme sea-levels might have a significant impact on the safety of coastal flood defenses.

We still work on the variable.

First we need to get the time stamps (in years here).

timeStamps = data[:, 0]

Then, we define the functional basis for each parameter of the GEV model. Even if we have

the possibility to affect a time-varying model to each of the 3 parameters ,

it is strongly recommended not to vary the parameter and to let it constant.

For numerical reasons, it is strongly recommended to normalize all the data as follows:

where:

the CenterReduce method where

is the mean time stamps

and

is the mean time stamps

and  is the standard deviation of the time stamps;

is the standard deviation of the time stamps;the MinMax method where

is the initial time and

is the initial time and  the final time;

the final time;the None method where

and

and  : in that case, data are not normalized.

: in that case, data are not normalized.

We suppose that  is linear in time, and that the other parameters remain constant.

is linear in time, and that the other parameters remain constant.

constant = ot.SymbolicFunction(["t"], ["1.0"])

basis_lin = ot.Basis([constant, ot.SymbolicFunction(["t"], ["t"])])

basis_cst = ot.Basis([constant])

# basis for mu, sigma, xi

basis_coll = [basis_lin, basis_cst, basis_cst]

We can now estimate the list of coefficients  using the log-likelihood of the data.

We test the 3 normalizing methods and both initial points in order to evaluate their impact on the results.

We can see that:

using the log-likelihood of the data.

We test the 3 normalizing methods and both initial points in order to evaluate their impact on the results.

We can see that:

both normalization methods lead to the same result for

,

,  and

and  (note that

(note that  depends on the normalization function),

depends on the normalization function),both initial points lead to the same result when the data have been normalized,

it is very important to normalize all the data: if not, the result strongly depends on the initial point and it differs from the result obtained with normalized data. The results are not optimal in that case since the associated log-likelihood are much smaller than those obtained with normalized data.

initiPoint_list = list()

initiPoint_list.append("Gumbel")

initiPoint_list.append("Static")

normMethod_list = list()

normMethod_list.append("MinMax")

normMethod_list.append("CenterReduce")

normMethod_list.append("None")

ot.ResourceMap.SetAsUnsignedInteger(

"GeneralizedExtremeValueFactory-MaximumEvaluationNumber", 1000000

)

print("Linear mu(t) model: ")

for normMeth in normMethod_list:

for initPoint in initiPoint_list:

print("normMeth, initPoint = ", normMeth, initPoint)

# The ot.Function() is the identity function.

result = factory.buildTimeVarying(

sample, timeStamps, basis_coll, ot.Function(), initPoint, normMeth

)

beta = result.getOptimalParameter()

print("beta1, beta2, beta3, beta4 = ", beta)

print("Max log-likelihood = ", result.getLogLikelihood())

Linear mu(t) model:

normMeth, initPoint = MinMax Gumbel

beta1, beta2, beta3, beta4 = [-242.635,6.25764,2.73173,-0.201355]

Max log-likelihood = -51.8940418474017

normMeth, initPoint = MinMax Static

beta1, beta2, beta3, beta4 = [-242.635,6.25777,2.73171,-0.201359]

Max log-likelihood = -51.894041787764984

normMeth, initPoint = CenterReduce Gumbel

beta1, beta2, beta3, beta4 = [-239.506,1.94197,2.73166,-0.201303]

Max log-likelihood = -51.89404131401922

normMeth, initPoint = CenterReduce Static

beta1, beta2, beta3, beta4 = [-239.506,1.94201,2.73163,-0.201294]

Max log-likelihood = -51.894041292150014

normMeth, initPoint = None Gumbel

beta1, beta2, beta3, beta4 = [-239.942,-0.000578171,2.80599,0.0958746]

Max log-likelihood = -61.18805537945545

normMeth, initPoint = None Static

beta1, beta2, beta3, beta4 = [-239.26,1.15331e-06,3.6427,-0.469838]

Max log-likelihood = -54.622262531545104

According to the previous results, we choose the MinMax normalization method and the Gumbel initial point. This initial point is cheaper than the Static one as it requires no optimization computation.

result_NonStatLL = factory.buildTimeVarying(

sample, timeStamps, basis_coll, ot.Function(), "Gumbel", "MinMax"

)

beta = result_NonStatLL.getOptimalParameter()

print("Linear mu(t) model : ")

print("beta1, beta2, beta3, beta_4 = ", beta)

print(f"mu(t) = {beta[0]:.4f} + {beta[1]:.4f} * tau")

print(f"sigma = = {beta[2]:.4f}")

print(f"xi = = {beta[3]:.4f}")

Linear mu(t) model :

beta1, beta2, beta3, beta_4 = [-242.635,6.25764,2.73173,-0.201355]

mu(t) = -242.6347 + 6.2576 * tau

sigma = = 2.7317

xi = = -0.2014

You can get the expression of the normalizing function  :

:

normFunc = result_NonStatLL.getNormalizationFunction()

print("Function tau(t): ", normFunc)

print("c = ", normFunc.getEvaluation().getImplementation().getCenter()[0])

print("1/d = ", normFunc.getEvaluation().getImplementation().getLinear()[0, 0])

Function tau(t): class=LinearFunction name=Unnamed implementation=class=LinearEvaluation name=Unnamed center=[1972] constant=[0] linear=[[ 0.05 ]]

c = 1972.0

1/d = 0.05

You can get the function  where

where

.

.

functionTheta = result_NonStatLL.getParameterFunction()

We get the asymptotic distribution of  to compute some confidence intervals of

the estimates, for example of order

to compute some confidence intervals of

the estimates, for example of order  .

.

dist_beta = result_NonStatLL.getParameterDistribution()

condifence_level = 0.95

for i in range(beta.getSize()):

lower_bound = dist_beta.getMarginal(i).computeQuantile((1 - condifence_level) / 2)[

0

]

upper_bound = dist_beta.getMarginal(i).computeQuantile((1 + condifence_level) / 2)[

0

]

print(

"Conf interval for beta_"

+ str(i + 1)

+ " = ["

+ str(lower_bound)

+ "; "

+ str(upper_bound)

+ "]"

)

Conf interval for beta_1 = [-245.03004510773928; -240.23928366420085]

Conf interval for beta_2 = [1.4859157842994541; 11.029371024769661]

Conf interval for beta_3 = [1.4710369824709508; 3.992420337465557]

Conf interval for beta_4 = [-0.711193527267937; 0.3084838313738077]

In order to compare different modelings, we get the optimal log-likelihood of the data for both stationary and non stationary models. The difference is significant enough to be in favor of the non stationary model.

print("Max log-likelihood: ")

print("Stationary model = ", result_LL.getLogLikelihood())

print("Non stationary linear mu(t) model = ", result_NonStatLL.getLogLikelihood())

Max log-likelihood:

Stationary model = -54.622265554594776

Non stationary linear mu(t) model = -51.8940418474017

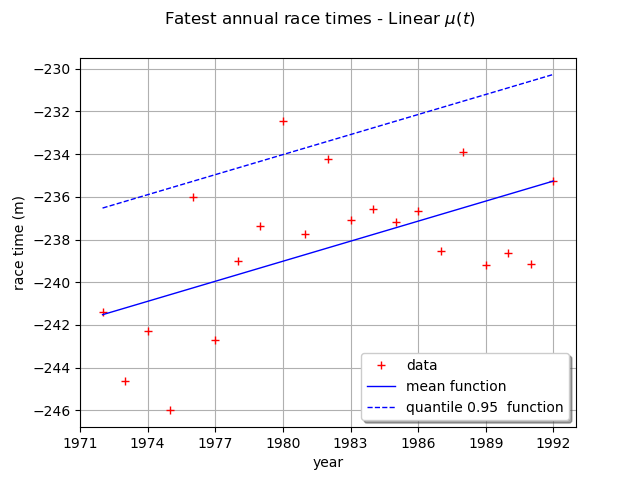

We can draw the mean function  . Be careful, it is not the function

. Be careful, it is not the function

. As a matter of fact, the mean is defined for

. As a matter of fact, the mean is defined for  only and in that case,

for

only and in that case,

for  , we have:

, we have:

and for  , we have:

, we have:

where  is the Euler constant.

is the Euler constant.

We can also draw the function  where

where  is the quantile of

order

is the quantile of

order  of the GEV distribution at time

of the GEV distribution at time  .

Here,

.

Here,  is a linear function and the other parameters are constant, so the mean and the quantile

functions are also linear functions.

is a linear function and the other parameters are constant, so the mean and the quantile

functions are also linear functions.

The graph confirms the increase of the annual maximum sea-levels through time.

graph = ot.Graph(

r"Fatest annual race times - Linear $\mu(t)$", "year", "race time (m)", True, ""

)

dataModified = data * ot.Point([1.0, -1.0])

graph.setIntegerXTick(True)

# data

cloud = ot.Cloud(dataModified)

cloud.setColor("red")

graph.add(cloud)

# mean function

meandata = [

result_NonStatLL.getDistribution(t).getMean()[0] for t in data[:, 0].asPoint()

]

curve_meanPoints = ot.Curve(data[:, 0].asPoint(), meandata)

graph.add(curve_meanPoints)

# quantile function

graphQuantile = result_NonStatLL.drawQuantileFunction(0.95)

drawQuant = graphQuantile.getDrawable(0)

drawQuant = graphQuantile.getDrawable(0)

drawQuant.setLineStyle("dashed")

graph.add(drawQuant)

graph.setLegends(["data", "mean function", "quantile 0.95 function"])

graph.setLegendPosition("bottomright")

view = otv.View(graph)

At last, we can test the validity of the stationary model  relative to the model with time varying parameters

relative to the model with time varying parameters  . The

model is parametrized by

. The

model is parametrized by  and the model

is parametrized by

and the model

is parametrized by  : so we have

: so we have

.

.

We use the Likelihood Ratio test. The null hypothesis is the stationary model .

The Type I error  is taken equal to 0.05.

is taken equal to 0.05.

This test confirms that the dependence through time is not negligible: it means that the linear model:math:mu(t) component explains a large variation in the data.

llh_LL = result_LL.getLogLikelihood()

llh_NonStatLL = result_NonStatLL.getLogLikelihood()

modelM0_Nb_param = 3

modelM1_Nb_param = 4

resultLikRatioTest = ot.HypothesisTest.LikelihoodRatioTest(

modelM0_Nb_param, llh_LL, modelM1_Nb_param, llh_NonStatLL, 0.05

)

accepted = resultLikRatioTest.getBinaryQualityMeasure()

print(

f"Hypothesis H0 (stationary model) vs H1 (linear mu(t) model): accepted ? = {accepted}"

)

Hypothesis H0 (stationary model) vs H1 (linear mu(t) model): accepted ? = False

We detail the statistics of the Likelihood Ratio test: the deviance statistics  follows

a

follows

a  distribution.

The model is rejected if the deviance statistics estimated on the data is greater than

the threshold

distribution.

The model is rejected if the deviance statistics estimated on the data is greater than

the threshold  or if the p-value is less than the Type I error

or if the p-value is less than the Type I error  .

.

print(f"Dp={resultLikRatioTest.getStatistic():.2f}")

print(f"alpha={resultLikRatioTest.getThreshold():.2f}")

print(f"p-value={resultLikRatioTest.getPValue():.2f}")

Dp=5.46

alpha=0.05

p-value=0.02

We can perform the same study with a quadratic model for :

basis_quad = ot.Basis(

[constant, ot.SymbolicFunction(["t"], ["t"]), ot.SymbolicFunction(["t"], ["t^2"])]

)

basis_coll_2 = [basis_quad, basis_cst, basis_cst]

result_NonStatLL_2 = factory.buildTimeVarying(

sample, timeStamps, basis_coll_2, ot.Function(), "Gumbel", "MinMax"

)

beta = result_NonStatLL_2.getOptimalParameter()

print("Quadratic mu(t) model : ")

print("beta1, beta2, beta3, beta4, beta5 = ", beta)

print(f"mu(t) = {beta[0]:.4f} + {beta[1]:.4f} * tau + {beta[2]:.4f} * tau^2")

print(f"sigma = {beta[3]:.4f}")

print(f"xi = {beta[4]:.4f}")

Quadratic mu(t) model :

beta1, beta2, beta3, beta4, beta5 = [-245.692,26.0513,-19.5972,2.28398,-0.182332]

mu(t) = -245.6916 + 26.0513 * tau + -19.5972 * tau^2

sigma = 2.2840

xi = -0.1823

We get the asymptotic distribution of to compute some confidence intervals of

the estimates, for example of order .

dist_beta = result_NonStatLL_2.getParameterDistribution()

condifence_level = 0.95

for i in range(beta.getSize()):

lower_bound = dist_beta.getMarginal(i).computeQuantile((1 - condifence_level) / 2)[

0

]

upper_bound = dist_beta.getMarginal(i).computeQuantile((1 + condifence_level) / 2)[

0

]

print(

"Conf interval for beta_"

+ str(i + 1)

+ " = ["

+ str(lower_bound)

+ "; "

+ str(upper_bound)

+ "]"

)

Conf interval for beta_1 = [-248.6277167489553; -242.7555038171466]

Conf interval for beta_2 = [9.891070937443686; 42.21154701845885]

Conf interval for beta_3 = [-35.56488628668891; -3.6294734809612716]

Conf interval for beta_4 = [1.4077955196970833; 3.160168420291918]

Conf interval for beta_5 = [-0.9157225566498194; 0.5510589288330662]

In order to compare different modelings, we get the optimal log-likelihood of the data for both stationary and non stationary models. The difference is significant enough to be in favor of the non stationary model.

print("Max log-likelihood = ")

print("Non stationary quadratic mu(t) model = ", result_NonStatLL_2.getLogLikelihood())

Max log-likelihood =

Non stationary quadratic mu(t) model = -48.4684335974957

At last, we can test the validity of the non stationary model

where is linear

relative to the model where is quadratic. The

model is parametrized by and the model

is parametrized by  : so we have

.

: so we have

.

We use the Likelihood Ratio test. The null hypothesis is the stationary model .

The Type I error is taken equal to 0.05.

This test confirms that the dependence through time is not negligible: it means that the

quadratic model explains even better a large variation in the data.

llh_NonStatLL_2 = result_NonStatLL_2.getLogLikelihood()

resultLikRatioTest = ot.HypothesisTest.LikelihoodRatioTest(

4, llh_NonStatLL, 5, llh_NonStatLL_2, 0.05

)

accepted = resultLikRatioTest.getBinaryQualityMeasure()

print(

f"Hypothesis H0 (linear mu(t) model) vs H1 (quadratic mu(t) model): accepted ? = {accepted}"

)

Hypothesis H0 (linear mu(t) model) vs H1 (quadratic mu(t) model): accepted ? = False

otv.View.ShowAll()

Total running time of the script: (0 minutes 10.332 seconds)