Tail dependence coefficients¶

The tail dependence coefficients helps to assess the asymptotic dependency of a bivariate random variables. We detail here the following ones:

the upper tail dependence coefficient denoted by

(which is the notation of the probability

community) as well as

(which is the notation of the probability

community) as well as  (which is the notation of the extreme value community),

(which is the notation of the extreme value community),the upper extremal dependence coefficient denoted by

,

,the lower tail dependence coefficient denoted by

,

,the upper extremal dependence coefficient denoted by

.

.

Readers should refer to [beirlant2004] to get more details.

Let  be a bivariate random vector with marginal distribution functions

be a bivariate random vector with marginal distribution functions

and

and  , and copula

, and copula  .

.

Upper tail dependence coefficient

We denote by or the upper tail dependence coefficient:

![\lambda_U = \chi = \lim_{u \to 1} \Pset[F_2(X_2) > u | F_1(X_1) > u]](data:image/svg+xml;base64,PD94bWwgdmVyc2lvbj0nMS4wJyBlbmNvZGluZz0nVVRGLTgnPz4KPCEtLSBUaGlzIGZpbGUgd2FzIGdlbmVyYXRlZCBieSBkdmlzdmdtIDMuMyAtLT4KPHN2ZyB2ZXJzaW9uPScxLjEnIHhtbG5zPSdodHRwOi8vd3d3LnczLm9yZy8yMDAwL3N2ZycgeG1sbnM6eGxpbms9J2h0dHA6Ly93d3cudzMub3JnLzE5OTkveGxpbmsnIHdpZHRoPScyMDYuMDAwOTY4cHQnIGhlaWdodD0nMTYuMTM5NDc0cHQnIHZpZXdCb3g9JzkxLjI3MTAxNSAtMTcuMzM0OTg4IDIwNi4wMDA5NjggMTYuMTM5NDc0Jz4KPGRlZnM+CjxwYXRoIGlkPSdnMC04MCcgZD0nTTMuMTMyMjU0LTMuNjgyMTkyQzMuMTgwMDc1LTMuNjgyMTkyIDMuNDMxMTMzLTMuNjgyMTkyIDMuNDU1MDQ0LTMuNjcwMjM3SDMuODYxNTE5QzYuMjg4NDE4LTMuNjcwMjM3IDcuMTYxMTQ2LTQuODA1OTc4IDcuMTYxMTQ2LTUuOTQxNzE5QzcuMTYxMTQ2LTcuNjM5MzUyIDUuNjMwODg0LTguMTg5MjkgNC4wODg2NjctOC4xODkyOUguNTk3NzU4Qy4zODI1NjUtOC4xODkyOSAuMTkxMjgzLTguMTg5MjkgLjE5MTI4My03Ljk3NDA5N0MuMTkxMjgzLTcuNzcwODU5IC40MTg0MzEtNy43NzA4NTkgLjUxNDA3Mi03Ljc3MDg1OUMxLjEzNTc0MS03Ljc3MDg1OSAxLjE4MzU2Mi03LjY3NTIxOCAxLjE4MzU2Mi03LjA4OTQxNVYtMS4wOTk4NzVDMS4xODM1NjItLjUxNDA3MiAxLjEzNTc0MS0uNDE4NDMxIC41MjYwMjctLjQxODQzMUMuNDA2NDc2LS40MTg0MzEgLjE5MTI4My0uNDE4NDMxIC4xOTEyODMtLjIxNTE5M0MuMTkxMjgzIDAgLjM4MjU2NSAwIC41OTc3NTggMEgzLjgwMTc0M0M0LjAxNjkzNiAwIDQuMTk2MjY0IDAgNC4xOTYyNjQtLjIxNTE5M0M0LjE5NjI2NC0uNDE4NDMxIDMuOTkzMDI2LS40MTg0MzEgMy44NjE1MTktLjQxODQzMUMzLjE4MDA3NS0uNDE4NDMxIDMuMTMyMjU0LS41MTQwNzIgMy4xMzIyNTQtMS4wOTk4NzVWLTMuNjgyMTkyWk01LjEwNDg1Ny00LjIyMDE3NEM1LjQ4NzQyMi00LjcyMjI5MSA1LjUyMzI4OC01LjQ3NTQ2NyA1LjUyMzI4OC01Ljk1MzY3NEM1LjUyMzI4OC02LjU4NzI5OCA1LjQ2MzUxMi03LjIyMDkyMiA1LjE1MjY3Ny03LjY2MzI2M0M1LjgxMDIxMi03LjUwNzg0NiA2Ljc0MjcxNS03LjE0OTE5MSA2Ljc0MjcxNS01Ljk0MTcxOUM2Ljc0MjcxNS01LjEwNDg1NyA2LjIwNDczMi00LjQ5NTE0MyA1LjEwNDg1Ny00LjIyMDE3NFpNMy4xMzIyNTQtNy4xMjUyOEMzLjEzMjI1NC03LjM2NDM4NCAzLjEzMjI1NC03Ljc3MDg1OSAzLjg0OTU2NC03Ljc3MDg1OUM0LjcxMDMzNi03Ljc3MDg1OSA1LjEwNDg1Ny03LjQ0ODA3IDUuMTA0ODU3LTUuOTUzNjc0QzUuMTA0ODU3LTQuMjQ0MDg1IDQuNDcxMjMzLTQuMTAwNjIzIDMuNzMwMDEyLTQuMTAwNjIzSDMuMTMyMjU0Vi03LjEyNTI4Wk0xLjUwNjM1MS0uNDE4NDMxQzEuNjAxOTkzLS42MzM2MjQgMS42MDE5OTMtLjkyMDU0OCAxLjYwMTk5My0xLjA3NTk2NVYtNy4xMTMzMjVDMS42MDE5OTMtNy4yNjg3NDIgMS42MDE5OTMtNy41NTU2NjYgMS41MDYzNTEtNy43NzA4NTlIMi44NjkyNEMyLjcxMzgyMy03LjU3OTU3NyAyLjcxMzgyMy03LjM0MDQ3MyAyLjcxMzgyMy03LjE2MTE0NlYtMS4wNzU5NjVDMi43MTM4MjMtLjk1NjQxMyAyLjcxMzgyMy0uNjMzNjI0IDIuODA5NDY1LS40MTg0MzFIMS41MDYzNTFaJy8+CjxwYXRoIGlkPSdnNS00OScgZD0nTTIuNTAyNjE1LTUuMDc2OTYxQzIuNTAyNjE1LTUuMjkyMTU0IDIuNDg2Njc1LTUuMzAwMTI1IDIuMjcxNDgyLTUuMzAwMTI1QzEuOTQ0NzA3LTQuOTgxMzIgMS41MjIyOTEtNC43OTAwMzcgLjc2NTEzMS00Ljc5MDAzN1YtNC41MjcwMjRDLjk4MDMyNC00LjUyNzAyNCAxLjQxMDcxLTQuNTI3MDI0IDEuODcyOTc2LTQuNzQyMjE3Vi0uNjUzNTQ5QzEuODcyOTc2LS4zNTg2NTUgMS44NDkwNjYtLjI2MzAxNCAxLjA5MTkwNS0uMjYzMDE0SC44MTI5NTFWMEMxLjEzOTcyNi0uMDIzOTEgMS44MjUxNTYtLjAyMzkxIDIuMTgzODExLS4wMjM5MVMzLjIzNTg2Ni0uMDIzOTEgMy41NjI2NCAwVi0uMjYzMDE0SDMuMjgzNjg2QzIuNTI2NTI2LS4yNjMwMTQgMi41MDI2MTUtLjM1ODY1NSAyLjUwMjYxNS0uNjUzNTQ5Vi01LjA3Njk2MVonLz4KPHBhdGggaWQ9J2c1LTUwJyBkPSdNMi4yNDc1NzItMS42MjU5MDNDMi4zNzUwOTMtMS43NDU0NTUgMi43MDk4MzgtMi4wMDg0NjggMi44MzczNi0yLjEyMDA1QzMuMzMxNTA3LTIuNTc0MzQ2IDMuODAxNzQzLTMuMDEyNzAyIDMuODAxNzQzLTMuNzM3OTgzQzMuODAxNzQzLTQuNjg2NDI2IDMuMDA0NzMyLTUuMzAwMTI1IDIuMDA4NDY4LTUuMzAwMTI1QzEuMDUyMDU1LTUuMzAwMTI1IC40MjI0MTYtNC41NzQ4NDQgLjQyMjQxNi0zLjg2NTUwNEMuNDIyNDE2LTMuNDc0OTY5IC43MzMyNS0zLjQxOTE3OCAuODQ0ODMyLTMuNDE5MTc4QzEuMDEyMjA0LTMuNDE5MTc4IDEuMjU5Mjc4LTMuNTM4NzMgMS4yNTkyNzgtMy44NDE1OTRDMS4yNTkyNzgtNC4yNTYwNCAuODYwNzcyLTQuMjU2MDQgLjc2NTEzMS00LjI1NjA0Qy45OTYyNjQtNC44Mzc4NTggMS41MzAyNjItNS4wMzcxMTEgMS45MjA3OTctNS4wMzcxMTFDMi42NjIwMTctNS4wMzcxMTEgMy4wNDQ1ODMtNC40MDc0NzIgMy4wNDQ1ODMtMy43Mzc5ODNDMy4wNDQ1ODMtMi45MDkwOTEgMi40NjI3NjUtMi4zMDMzNjIgMS41MjIyOTEtMS4zMzg5NzlMLjUxODA1Ny0uMzAyODY0Qy40MjI0MTYtLjIxNTE5MyAuNDIyNDE2LS4xOTkyNTMgLjQyMjQxNiAwSDMuNTcwNjFMMy44MDE3NDMtMS40MjY2NUgzLjU1NDY3QzMuNTMwNzYtMS4yNjcyNDggMy40NjY5OTktLjg2ODc0MiAzLjM3MTM1Ny0uNzE3MzFDMy4zMjM1MzctLjY1MzU0OSAyLjcxNzgwOC0uNjUzNTQ5IDIuNTkwMjg2LS42NTM1NDlIMS4xNzE2MDZMMi4yNDc1NzItMS42MjU5MDNaJy8+CjxwYXRoIGlkPSdnMi0xMDYnIGQ9J00xLjkwMDg3Mi04LjUzNTk5QzEuOTAwODcyLTguNzUxMTgzIDEuOTAwODcyLTguOTY2Mzc2IDEuNjYxNzY4LTguOTY2Mzc2UzEuNDIyNjY1LTguNzUxMTgzIDEuNDIyNjY1LTguNTM1OTlWMi41NTg0MDZDMS40MjI2NjUgMi43NzM1OTkgMS40MjI2NjUgMi45ODg3OTIgMS42NjE3NjggMi45ODg3OTJTMS45MDA4NzIgMi43NzM1OTkgMS45MDA4NzIgMi41NTg0MDZWLTguNTM1OTlaJy8+CjxwYXRoIGlkPSdnNi00MCcgZD0nTTMuODg1NDMgMi45MDUxMDZDMy44ODU0MyAyLjg2OTI0IDMuODg1NDMgMi44NDUzMyAzLjY4MjE5MiAyLjY0MjA5MkMyLjQ4NjY3NSAxLjQzNDYyIDEuODE3MTg2LS41Mzc5ODMgMS44MTcxODYtMi45NzY4MzdDMS44MTcxODYtNS4yOTYxMzkgMi4zNzkwNzgtNy4yOTI2NTMgMy43NjU4NzgtOC43MDMzNjJDMy44ODU0My04LjgxMDk1OSAzLjg4NTQzLTguODM0ODY5IDMuODg1NDMtOC44NzA3MzVDMy44ODU0My04Ljk0MjQ2NiAzLjgyNTY1NC04Ljk2NjM3NiAzLjc3NzgzMy04Ljk2NjM3NkMzLjYyMjQxNi04Ljk2NjM3NiAyLjY0MjA5Mi04LjEwNTYwNCAyLjA1NjI4OS02LjkzMzk5OEMxLjQ0NjU3NS01LjcyNjUyNiAxLjE3MTYwNi00LjQ0NzMyMyAxLjE3MTYwNi0yLjk3NjgzN0MxLjE3MTYwNi0xLjkxMjgyNyAxLjMzODk3OS0uNDkwMTYyIDEuOTYwNjQ4IC43ODkwNDFDMi42NjYwMDIgMi4yMjM2NjEgMy42NDYzMjYgMy4wMDA3NDcgMy43Nzc4MzMgMy4wMDA3NDdDMy44MjU2NTQgMy4wMDA3NDcgMy44ODU0MyAyLjk3NjgzNyAzLjg4NTQzIDIuOTA1MTA2WicvPgo8cGF0aCBpZD0nZzYtNDEnIGQ9J00zLjM3MTM1Ny0yLjk3NjgzN0MzLjM3MTM1Ny0zLjg4NTQzIDMuMjUxODA2LTUuMzY3ODcgMi41ODIzMTYtNi43NTQ2N0MxLjg3Njk2MS04LjE4OTI5IC44OTY2MzgtOC45NjYzNzYgLjc2NTEzMS04Ljk2NjM3NkMuNzE3MzEtOC45NjYzNzYgLjY1NzUzNC04Ljk0MjQ2NiAuNjU3NTM0LTguODcwNzM1Qy42NTc1MzQtOC44MzQ4NjkgLjY1NzUzNC04LjgxMDk1OSAuODYwNzcyLTguNjA3NzIxQzIuMDU2Mjg5LTcuNDAwMjQ5IDIuNzI1Nzc4LTUuNDI3NjQ2IDIuNzI1Nzc4LTIuOTg4NzkyQzIuNzI1Nzc4LS42Njk0ODkgMi4xNjM4ODUgMS4zMjcwMjQgLjc3NzA4NiAyLjczNzczM0MuNjU3NTM0IDIuODQ1MzMgLjY1NzUzNCAyLjg2OTI0IC42NTc1MzQgMi45MDUxMDZDLjY1NzUzNCAyLjk3NjgzNyAuNzE3MzEgMy4wMDA3NDcgLjc2NTEzMSAzLjAwMDc0N0MuOTIwNTQ4IDMuMDAwNzQ3IDEuOTAwODcyIDIuMTM5OTc1IDIuNDg2Njc1IC45NjgzNjlDMy4wOTYzODktLjI1MTA1OSAzLjM3MTM1Ny0xLjU0MjIxNyAzLjM3MTM1Ny0yLjk3NjgzN1onLz4KPHBhdGggaWQ9J2c2LTYxJyBkPSdNOC4wNjk3MzgtMy44NzM0NzRDOC4yMzcxMTEtMy44NzM0NzQgOC40NTIzMDQtMy44NzM0NzQgOC40NTIzMDQtNC4wODg2NjdDOC40NTIzMDQtNC4zMTU4MTYgOC4yNDkwNjYtNC4zMTU4MTYgOC4wNjk3MzgtNC4zMTU4MTZIMS4wMjgxNDRDLjg2MDc3Mi00LjMxNTgxNiAuNjQ1NTc5LTQuMzE1ODE2IC42NDU1NzktNC4xMDA2MjNDLjY0NTU3OS0zLjg3MzQ3NCAuODQ4ODE3LTMuODczNDc0IDEuMDI4MTQ0LTMuODczNDc0SDguMDY5NzM4Wk04LjA2OTczOC0xLjY0OTgxM0M4LjIzNzExMS0xLjY0OTgxMyA4LjQ1MjMwNC0xLjY0OTgxMyA4LjQ1MjMwNC0xLjg2NTAwNkM4LjQ1MjMwNC0yLjA5MjE1NCA4LjI0OTA2Ni0yLjA5MjE1NCA4LjA2OTczOC0yLjA5MjE1NEgxLjAyODE0NEMuODYwNzcyLTIuMDkyMTU0IC42NDU1NzktMi4wOTIxNTQgLjY0NTU3OS0xLjg3Njk2MUMuNjQ1NTc5LTEuNjQ5ODEzIC44NDg4MTctMS42NDk4MTMgMS4wMjgxNDQtMS42NDk4MTNIOC4wNjk3MzhaJy8+CjxwYXRoIGlkPSdnNi05MScgZD0nTTIuOTg4NzkyIDIuOTg4NzkyVjIuNTQ2NDUxSDEuODI5MTQxVi04LjUyNDAzNUgyLjk4ODc5MlYtOC45NjYzNzZIMS4zODY4VjIuOTg4NzkySDIuOTg4NzkyWicvPgo8cGF0aCBpZD0nZzYtOTMnIGQ9J00xLjg1MzA1MS04Ljk2NjM3NkguMjUxMDU5Vi04LjUyNDAzNUgxLjQxMDcxVjIuNTQ2NDUxSC4yNTEwNTlWMi45ODg3OTJIMS44NTMwNTFWLTguOTY2Mzc2WicvPgo8cGF0aCBpZD0nZzYtMTA1JyBkPSdNMi4wODAxOTktNy4zNjQzODRDMi4wODAxOTktNy42NzUyMTggMS44MjkxNDEtNy45NTAxODcgMS40OTQzOTYtNy45NTAxODdDMS4xODM1NjItNy45NTAxODcgLjkyMDU0OC03LjY5OTEyOCAuOTIwNTQ4LTcuMzc2MzM5Qy45MjA1NDgtNy4wMTc2ODQgMS4yMDc0NzItNi43OTA1MzUgMS40OTQzOTYtNi43OTA1MzVDMS44NjUwMDYtNi43OTA1MzUgMi4wODAxOTktNy4xMDEzNyAyLjA4MDE5OS03LjM2NDM4NFpNLjQzMDM4Ni01LjE0MDcyMlYtNC43OTQwMjJDMS4xOTU1MTctNC43OTQwMjIgMS4zMDMxMTMtNC43MjIyOTEgMS4zMDMxMTMtNC4xMzY0ODhWLS44ODQ2ODJDMS4zMDMxMTMtLjM0NjcgMS4xNzE2MDYtLjM0NjcgLjM5NDUyMS0uMzQ2N1YwQy43MjkyNjUtLjAyMzkxIDEuMzAzMTEzLS4wMjM5MSAxLjY0OTgxMy0uMDIzOTFDMS43ODEzMi0uMDIzOTEgMi40NzQ3Mi0uMDIzOTEgMi44ODExOTYgMFYtLjM0NjdDMi4xMDQxMS0uMzQ2NyAyLjA1NjI4OS0uNDA2NDc2IDIuMDU2Mjg5LS44NzI3MjdWLTUuMjcyMjI5TC40MzAzODYtNS4xNDA3MjJaJy8+CjxwYXRoIGlkPSdnNi0xMDgnIGQ9J00yLjA1NjI4OS04LjI5Njg4N0wuMzk0NTIxLTguMTY1MzhWLTcuODE4NjhDMS4yMDc0NzItNy44MTg2OCAxLjMwMzExMy03LjczNDk5NCAxLjMwMzExMy03LjE0OTE5MVYtLjg4NDY4MkMxLjMwMzExMy0uMzQ2NyAxLjE3MTYwNi0uMzQ2NyAuMzk0NTIxLS4zNDY3VjBDLjcyOTI2NS0uMDIzOTEgMS4zMTUwNjgtLjAyMzkxIDEuNjczNzI0LS4wMjM5MVMyLjYzMDEzNy0uMDIzOTEgMi45NjQ4ODIgMFYtLjM0NjdDMi4xOTk3NTEtLjM0NjcgMi4wNTYyODktLjM0NjcgMi4wNTYyODktLjg4NDY4MlYtOC4yOTY4ODdaJy8+CjxwYXRoIGlkPSdnNi0xMDknIGQ9J004LjU3MTg1Ni0yLjkwNTEwNkM4LjU3MTg1Ni00LjAxNjkzNiA4LjU3MTg1Ni00LjM1MTY4MSA4LjI5Njg4Ny00LjczNDI0N0M3Ljk1MDE4Ny01LjIwMDQ5OCA3LjM4ODI5NC01LjI3MjIyOSA2Ljk4MTgxOC01LjI3MjIyOUM1Ljk4OTUzOS01LjI3MjIyOSA1LjQ4NzQyMi00LjU1NDkxOSA1LjI5NjEzOS00LjA4ODY2N0M1LjEyODc2Ny01LjAwOTIxNSA0LjQ4MzE4OC01LjI3MjIyOSAzLjczMDAxMi01LjI3MjIyOUMyLjU3MDM2MS01LjI3MjIyOSAyLjExNjA2NS00LjI3OTk1IDIuMDIwNDIzLTQuMDQwODQ3SDIuMDA4NDY4Vi01LjI3MjIyOUwuMzgyNTY1LTUuMTQwNzIyVi00Ljc5NDAyMkMxLjE5NTUxNy00Ljc5NDAyMiAxLjI5MTE1OC00LjcxMDMzNiAxLjI5MTE1OC00LjEyNDUzM1YtLjg4NDY4MkMxLjI5MTE1OC0uMzQ2NyAxLjE1OTY1MS0uMzQ2NyAuMzgyNTY1LS4zNDY3VjBDLjY5MzQtLjAyMzkxIDEuMzM4OTc5LS4wMjM5MSAxLjY3MzcyNC0uMDIzOTFDMi4wMjA0MjMtLjAyMzkxIDIuNjY2MDAyLS4wMjM5MSAyLjk3NjgzNyAwVi0uMzQ2N0MyLjIxMTcwNi0uMzQ2NyAyLjA2ODI0NC0uMzQ2NyAyLjA2ODI0NC0uODg0NjgyVi0zLjEwODM0NEMyLjA2ODI0NC00LjM2MzYzNiAyLjg5MzE1MS01LjAzMzEyNiAzLjYzNDM3MS01LjAzMzEyNlM0LjU0Mjk2NC00LjQyMzQxMiA0LjU0Mjk2NC0zLjY5NDE0N1YtLjg4NDY4MkM0LjU0Mjk2NC0uMzQ2NyA0LjQxMTQ1Ny0uMzQ2NyAzLjYzNDM3MS0uMzQ2N1YwQzMuOTQ1MjA1LS4wMjM5MSA0LjU5MDc4NS0uMDIzOTEgNC45MjU1MjktLjAyMzkxQzUuMjcyMjI5LS4wMjM5MSA1LjkxNzgwOC0uMDIzOTEgNi4yMjg2NDMgMFYtLjM0NjdDNS40NjM1MTItLjM0NjcgNS4zMjAwNS0uMzQ2NyA1LjMyMDA1LS44ODQ2ODJWLTMuMTA4MzQ0QzUuMzIwMDUtNC4zNjM2MzYgNi4xNDQ5NTYtNS4wMzMxMjYgNi44ODYxNzctNS4wMzMxMjZTNy43OTQ3Ny00LjQyMzQxMiA3Ljc5NDc3LTMuNjk0MTQ3Vi0uODg0NjgyQzcuNzk0NzctLjM0NjcgNy42NjMyNjMtLjM0NjcgNi44ODYxNzctLjM0NjdWMEM3LjE5NzAxMS0uMDIzOTEgNy44NDI1OS0uMDIzOTEgOC4xNzczMzUtLjAyMzkxQzguNTI0MDM1LS4wMjM5MSA5LjE2OTYxNC0uMDIzOTEgOS40ODA0NDggMFYtLjM0NjdDOC44ODI2OS0uMzQ2NyA4LjU4MzgxMS0uMzQ2NyA4LjU3MTg1Ni0uNzA1MzU1Vi0yLjkwNTEwNlonLz4KPHBhdGggaWQ9J2czLTg1JyBkPSdNNS4zMTYwNjUtNC41NzQ4NDRDNS40MTE3MDYtNC45NjUzOCA1LjU5NTAxOS01LjE1NjY2MyA2LjE2MDg5Ny01LjE4MDU3M0M2LjI0MDU5OC01LjE4MDU3MyA2LjMwNDM1OS01LjIyODM5NCA2LjMwNDM1OS01LjMzMjAwNUM2LjMwNDM1OS01LjM3OTgyNiA2LjI2NDUwOC01LjQ0MzU4NyA2LjE4NDgwNy01LjQ0MzU4N0M2LjE0NDk1Ni01LjQ0MzU4NyA1Ljk2OTYxNC01LjQxOTY3NiA1LjM5NTc2Ni01LjQxOTY3NkM0Ljc1ODE1Ny01LjQxOTY3NiA0LjY1NDU0NS01LjQ0MzU4NyA0LjU4MjgxNC01LjQ0MzU4N0M0LjQ1NTI5My01LjQ0MzU4NyA0LjQzMTM4Mi01LjM1NTkxNSA0LjQzMTM4Mi01LjI5MjE1NEM0LjQzMTM4Mi01LjE4ODU0MyA0LjUzNDk5NC01LjE4MDU3MyA0LjYwNjcyNS01LjE4MDU3M0M1LjA5MjkwMi01LjE2NDYzMyA1LjA5MjkwMi00Ljk0OTQ0IDUuMDkyOTAyLTQuODM3ODU4QzUuMDkyOTAyLTQuNzkwMDM3IDUuMDg0OTMyLTQuNzUwMTg3IDUuMDc2OTYxLTQuNzAyMzY2QzUuMDYxMDIxLTQuNjQ2NTc1IDQuMzk5NTAyLTEuOTc2NTg4IDQuMzY3NjIxLTEuODcyOTc2QzQuMDgwNjk3LS43MjUyOCAzLjA3NjQ2My0uMDk1NjQxIDIuMjg3NDIyLS4wOTU2NDFDMS43Mzc0ODQtLjA5NTY0MSAxLjI0MzMzNy0uNDIyNDE2IDEuMjQzMzM3LTEuMTU1NjY2QzEuMjQzMzM3LTEuMjkxMTU4IDEuMjY3MjQ4LTEuNTA2MzUxIDEuMjk5MTI4LTEuNjMzODczTDIuMDk2MTM5LTQuODIxOTE4QzIuMTY3ODctNS4xMDg4NDIgMi4xODM4MTEtNS4xODA1NzMgMi43NjU2MjktNS4xODA1NzNDMi45MjUwMzEtNS4xODA1NzMgMy4wMjA2NzItNS4xODA1NzMgMy4wMjA2NzItNS4zMzIwMDVDMy4wMjA2NzItNS4zMzk5NzUgMy4wMTI3MDItNS40NDM1ODcgMi44ODUxODEtNS40NDM1ODdDMi43MzM3NDgtNS40NDM1ODcgMi41NDI0NjYtNS40Mjc2NDYgMi4zOTEwMzQtNS40MTk2NzZIMS44ODg5MTdDMS4xMjM3ODYtNS40MTk2NzYgLjkxNjU2My01LjQ0MzU4NyAuODYwNzcyLTUuNDQzNTg3Qy44Mjg4OTItNS40NDM1ODcgLjcwMTM3LTUuNDQzNTg3IC43MDEzNy01LjI5MjE1NEMuNzAxMzctNS4xODA1NzMgLjgwNDk4MS01LjE4MDU3MyAuOTMyNTAzLTUuMTgwNTczQzEuMTk1NTE3LTUuMTgwNTczIDEuNDI2NjUtNS4xODA1NzMgMS40MjY2NS01LjA1MzA1MUMxLjQyNjY1LTUuMDA1MjMgMS4zNTQ5MTktNC43MTgzMDYgMS4zMDcwOTgtNC41NTg5MDRMMS4xMzE3NTYtMy44NTc1MzRMLjcxNzMxLTIuMTY3ODdDLjYwNTcyOS0xLjcyOTUxNCAuNTczODQ4LTEuNjA5OTYzIC41NzM4NDgtMS4zOTQ3N0MuNTczODQ4LS40NjIyNjcgMS4zMDcwOTggLjE2NzM3MiAyLjI1NTU0MiAuMTY3MzcyQzMuMzM5NDc3IC4xNjczNzIgNC4zNTk2NTEtLjc0OTE5MSA0LjYxNDY5NS0xLjc3NzMzNUw1LjMxNjA2NS00LjU3NDg0NFonLz4KPHBhdGggaWQ9J2czLTExNycgZD0nTTIuOTg4NzkyLS44Njg3NDJDMi45NDg5NDEtLjcxNzMxIDIuNTc0MzQ2LS4xNDM0NjIgMi4wNDAzNDktLjE0MzQ2MkMxLjY0OTgxMy0uMTQzNDYyIDEuNTE0MzIxLS40MzAzODYgMS41MTQzMjEtLjc4OTA0MUMxLjUxNDMyMS0xLjI1OTI3OCAxLjc5MzI3NS0xLjk3NjU4OCAxLjk2ODYxOC0yLjQyMjkxNEMyLjA0ODMxOS0yLjYyMjE2NyAyLjA3MjIyOS0yLjY5Mzg5OCAyLjA3MjIyOS0yLjgzNzM2QzIuMDcyMjI5LTMuMjc1NzE2IDEuNzIxNTQ0LTMuNTE0ODE5IDEuMzU0OTE5LTMuNTE0ODE5Qy41NjU4NzgtMy41MTQ4MTkgLjIzOTEwMy0yLjM5MTAzNCAuMjM5MTAzLTIuMjk1MzkyQy4yMzkxMDMtMi4yMjM2NjEgLjI5NDg5NC0yLjE5MTc4MSAuMzU4NjU1LTIuMTkxNzgxQy40NjIyNjctMi4xOTE3ODEgLjQ3MDIzNy0yLjIzOTYwMSAuNDk0MTQ3LTIuMzE5MzAzQy43MDEzNy0zLjAyODY0MyAxLjA1MjA1NS0zLjI5MTY1NiAxLjMzMTAwOS0zLjI5MTY1NkMxLjQ1MDU2LTMuMjkxNjU2IDEuNTIyMjkxLTMuMjExOTU1IDEuNTIyMjkxLTMuMDI4NjQzUzEuNDUwNTYtMi42NjIwMTcgMS4zNDY5NDktMi4zODMwNjRDMS4wMTIyMDQtMS41MzgyMzIgLjk0MDQ3My0xLjE5NTUxNyAuOTQwNDczLS45MDg1OTNDLjk0MDQ3My0uMTI3NTIyIDEuNTMwMjYyIC4wNzk3MDEgMi4wMDA0OTggLjA3OTcwMUMyLjU5ODI1NyAuMDc5NzAxIDIuOTY0ODgyLS4zOTg1MDYgMi45OTY3NjItLjQzODM1NkMzLjEyNDI4NC0uMDYzNzYxIDMuNDgyOTM5IC4wNzk3MDEgMy43Njk4NjMgLjA3OTcwMUM0LjE0NDQ1OCAuMDc5NzAxIDQuMzI3NzcxLS4yMzkxMDMgNC4zODM1NjItLjM1ODY1NUM0LjU0Mjk2NC0uNjQ1NTc5IDQuNjU0NTQ1LTEuMTA3ODQ2IDQuNjU0NTQ1LTEuMTM5NzI2QzQuNjU0NTQ1LTEuMTg3NTQ3IDQuNjIyNjY1LTEuMjQzMzM3IDQuNTI3MDI0LTEuMjQzMzM3UzQuNDE1NDQyLTEuMjAzNDg3IDQuMzY3NjIxLS45OTYyNjRDNC4yNjQwMS0uNTk3NzU4IDQuMTIwNTQ4LS4xNDM0NjIgMy43OTM3NzMtLjE0MzQ2MkMzLjYxMDQ2MS0uMTQzNDYyIDMuNTM4NzMtLjI5NDg5NCAzLjUzODczLS41MTgwNTdDMy41Mzg3My0uNjUzNTQ5IDMuNjEwNDYxLS45MjQ1MzMgMy42NTgyODEtMS4xMjM3ODZTMy44MjU2NTQtMS44MDEyNDUgMy44NTc1MzQtMS45NDQ3MDdMNC4wMTY5MzYtMi41NTA0MzZDNC4wNjQ3NTctMi43NjU2MjkgNC4xNjAzOTktMy4xNDAyMjQgNC4xNjAzOTktMy4xODgwNDVDNC4xNjAzOTktMy4zODcyOTggNC4wMDA5OTYtMy40MzUxMTggMy45MDUzNTUtMy40MzUxMThDMy43OTM3NzMtMy40MzUxMTggMy42MTg0MzEtMy4zNjMzODcgMy41NjI2NC0zLjE3MjEwNUwyLjk4ODc5Mi0uODY4NzQyWicvPgo8cGF0aCBpZD0nZzEtMzMnIGQ9J002Ljk1NzkwOC0xLjgwOTIxNUM2LjY4NjkyNC0xLjYwOTk2MyA2LjQzOTg1MS0xLjM1NDkxOSA2LjI0ODU2OC0xLjA2Nzk5NUM1LjkwNTg1My0uNTQ5OTM4IDUuODE4MTgyLS4wMzk4NTEgNS44MTgxODItLjAwNzk3QzUuODE4MTgyIC4xMTE1ODIgNS45Mjk3NjMgLjExMTU4MiA2LjAwMTQ5NCAuMTExNTgyQzYuMDg5MTY2IC4xMTE1ODIgNi4xNjA4OTcgLjExMTU4MiA2LjE4NDgwNyAuMDA3OTdDNi4zOTIwMy0uODc2NzEyIDYuOTAyMTE3LTEuNTQ2MjAyIDcuODY2NTAxLTEuODcyOTc2QzcuOTMwMjYyLTEuODg4OTE3IDcuOTk0MDIyLTEuOTEyODI3IDcuOTk0MDIyLTEuOTkyNTI4UzcuOTIyMjkxLTIuMDk2MTM5IDcuODkwNDExLTIuMTA0MTFDNi44MzAzODYtMi40NjI3NjUgNi4zNjgxMi0zLjIxMTk1NSA2LjIwMDc0Ny0zLjkxMzMyNUM2LjE2MDg5Ny00LjA3MjcyNyA2LjE2MDg5Ny00LjA5NjYzOCA2LjAwMTQ5NC00LjA5NjYzOEM1LjkyOTc2My00LjA5NjYzOCA1LjgxODE4Mi00LjA5NjYzOCA1LjgxODE4Mi0zLjk3NzA4NkM1LjgxODE4Mi0zLjk2MTE0NiA1Ljg5Nzg4My0zLjQzNTExOCA2LjI0ODU2OC0yLjkwOTA5MUM2LjQ3OTcwMS0yLjU3NDM0NiA2Ljc1ODY1NS0yLjMyNzI3MyA2Ljk1NzkwOC0yLjE3NTg0MUguNzczMTAxQy42NDU1NzktMi4xNzU4NDEgLjQ3MDIzNy0yLjE3NTg0MSAuNDcwMjM3LTEuOTkyNTI4Uy42NDU1NzktMS44MDkyMTUgLjc3MzEwMS0xLjgwOTIxNUg2Ljk1NzkwOFonLz4KPHBhdGggaWQ9J2c0LTIxJyBkPSdNMy42OTQxNDctNy40NDgwN0MzLjM5NTI2OC04LjI5Njg4NyAyLjQ1MDgwOS04LjI5Njg4NyAyLjI5NTM5Mi04LjI5Njg4N0MyLjIyMzY2MS04LjI5Njg4NyAyLjA5MjE1NC04LjI5Njg4NyAyLjA5MjE1NC04LjE3NzMzNUMyLjA5MjE1NC04LjA4MTY5NCAyLjE2Mzg4NS04LjA2OTczOCAyLjIyMzY2MS04LjA1Nzc4M0MyLjQwMjk4OS04LjAzMzg3MyAyLjU0NjQ1MS04LjAwOTk2MyAyLjczNzczMy03LjY2MzI2M0MyLjg1NzI4NS03LjQzNjExNSA0LjA4ODY2Ny0zLjg2MTUxOSA0LjA4ODY2Ny0zLjgzNzYwOUM0LjA4ODY2Ny0zLjgyNTY1NCA0LjA3NjcxMi0zLjgxMzY5OSAzLjk4MTA3MS0zLjcxODA1N0wuODcyNzI3LS41NzM4NDhDLjcyOTI2NS0uNDMwMzg2IC42MzM2MjQtLjMzNDc0NSAuNjMzNjI0LS4xNzkzMjhDLjYzMzYyNC0uMDExOTU1IC43NzcwODYgLjEzMTUwNyAuOTY4MzY5IC4xMzE1MDdDMS4wMTYxODkgLjEzMTUwNyAxLjE0NzY5NiAuMTA3NTk3IDEuMjE5NDI3IC4wMzU4NjZDMS40MTA3MS0uMTQzNDYyIDMuMTIwMjk5LTIuMjM1NjE2IDQuMjA4MjE5LTMuNTI2Nzc1QzQuNTE5MDU0LTIuNTk0MjcxIDQuOTAxNjE5LTEuNDk0Mzk2IDUuMjcyMjI5LS40OTAxNjJDNS4zMzIwMDUtLjMxMDgzNCA1LjM5MTc4MS0uMTQzNDYyIDUuNTU5MTUzIC4wMTE5NTVDNS42Nzg3MDUgLjExOTU1MiA1LjcwMjYxNSAuMTE5NTUyIDYuMDM3MzYgLjExOTU1Mkg2LjI2NDUwOEM2LjMxMjMyOSAuMTE5NTUyIDYuMzk2MDE1IC4xMTk1NTIgNi4zOTYwMTUgLjAyMzkxQzYuMzk2MDE1LS4wMjM5MSA2LjM4NDA2LS4wMzU4NjYgNi4zMzYyMzktLjA4MzY4NkM2LjIyODY0My0uMjE1MTkzIDYuMTQ0OTU2LS40MzAzODYgNi4wOTcxMzYtLjU3Mzg0OEwzLjY5NDE0Ny03LjQ0ODA3WicvPgo8cGF0aCBpZD0nZzQtMzEnIGQ9J00zLjk0NTIwNS0xLjkyNDc4MkMzLjYyMjQxNi0yLjkxNzA2MSAzLjY5NDE0Ny0yLjgyMTQyIDMuMzk1MjY4LTMuNjU4MjgxQzMuMDI0NjU4LTQuNjg2NDI2IDIuOTI5MDE2LTQuNzcwMTEyIDIuNzYxNjQ0LTQuOTM3NDg0QzIuNTQ2NDUxLTUuMTI4NzY3IDIuMTM5OTc1LTUuMjcyMjI5IDEuNzIxNTQ0LTUuMjcyMjI5QzEuMDUyMDU1LTUuMjcyMjI5IC43MjkyNjUtNC42NTA1NiAuNzI5MjY1LTQuNDk1MTQzQy43MjkyNjUtNC40MjM0MTIgLjc4OTA0MS00LjM4NzU0NyAuODYwNzcyLTQuMzg3NTQ3Qy45NTY0MTMtNC4zODc1NDcgLjk4MDMyNC00LjQ0NzMyMyAuOTkyMjc5LTQuNDk1MTQzQzEuMTcxNjA2LTQuOTYxMzk1IDEuNTQyMjE3LTUuMDMzMTI2IDEuNjQ5ODEzLTUuMDMzMTI2QzEuOTk2NTEzLTUuMDMzMTI2IDIuMzMxMjU4LTQuMTcyMzU0IDIuNTQ2NDUxLTMuNTk4NTA2QzIuODMzMzc1LTIuODY5MjQgMi45NzY4MzctMi4zNjcxMjMgMy4yOTk2MjYtMS4yMDc0NzJMLjQ3ODIwNyAxLjk5NjUxM0MuMzcwNjEgMi4xMjgwMiAuMzcwNjEgMi4xNzU4NDEgLjM3MDYxIDIuMTg3Nzk2Qy4zNzA2MSAyLjI4MzQzNyAuNDMwMzg2IDIuMzA3MzQ3IC40NzgyMDcgMi4zMDczNDdTLjU2MTg5MyAyLjI4MzQzNyAuNTk3NzU4IDIuMjQ3NTcyQy45MzI1MDMgMS45MTI4MjcgMS42NzM3MjQgMS4wMjgxNDQgMS45ODQ1NTggLjY2OTQ4OUwzLjM3MTM1Ny0uOTA4NTkzQzMuOTU3MTYxIC45MzI1MDMgMy45NTcxNjEgLjk1NjQxMyA0LjEzNjQ4OCAxLjM5ODc1NUM0LjMyNzc3MSAxLjg1MzA1MSA0LjU3ODgyOSAyLjQzODg1NCA1LjU5NTAxOSAyLjQzODg1NEM2LjI3NjQ2MyAyLjQzODg1NCA2LjU4NzI5OCAxLjgyOTE0MSA2LjU4NzI5OCAxLjY2MTc2OEM2LjU4NzI5OCAxLjU3ODA4MiA2LjUxNTU2NyAxLjU1NDE3MiA2LjQ1NTc5MSAxLjU1NDE3MkM2LjM2MDE0OSAxLjU1NDE3MiA2LjM0ODE5NCAxLjYwMTk5MyA2LjMxMjMyOSAxLjY5NzYzNEM2LjE4MDgyMiAyLjAzMjM3OSA1Ljg2OTk4OCAyLjE5OTc1MSA1LjY3ODcwNSAyLjE5OTc1MUM1LjUyMzI4OCAyLjE5OTc1MSA1LjMzMjAwNSAyLjE5OTc1MSA0LjgwNTk3OCAuODcyNzI3QzQuNDk1MTQzIC4wNzE3MzEgNC4yMjAxNzQtLjg4NDY4MiA0LjAxNjkzNi0xLjYyNTkwM0w2Ljg1MDMxMS00Ljg1Mzc5OEM2Ljk0NTk1My00Ljk2MTM5NSA2Ljk1NzkwOC00Ljk3MzM1IDYuOTU3OTA4LTUuMDIxMTcxQzYuOTU3OTA4LTUuMTA0ODU3IDYuODk4MTMyLTUuMTQwNzIyIDYuODM4MzU2LTUuMTQwNzIyQzYuODAyNDkxLTUuMTQwNzIyIDYuNzY2NjI1LTUuMTQwNzIyIDYuNjQ3MDczLTUuMDA5MjE1TDMuOTQ1MjA1LTEuOTI0NzgyWicvPgo8cGF0aCBpZD0nZzQtNjInIGQ9J003Ljg3ODQ1Ni0yLjcyNTc3OEM4LjEwNTYwNC0yLjgzMzM3NSA4LjExNzU1OS0yLjkwNTEwNiA4LjExNzU1OS0yLjk4ODc5MkM4LjExNzU1OS0zLjA2MDUyMyA4LjA5MzY0OS0zLjE0NDIwOSA3Ljg3ODQ1Ni0zLjIzOTg1MUwxLjQxMDcxLTYuMjE2Njg3QzEuMjU1MjkzLTYuMjg4NDE4IDEuMjMxMzgyLTYuMzAwMzc0IDEuMjA3NDcyLTYuMzAwMzc0QzEuMDY0MDEtNi4zMDAzNzQgLjk4MDMyNC02LjE4MDgyMiAuOTgwMzI0LTYuMDg1MTgxQy45ODAzMjQtNS45NDE3MTkgMS4wNzU5NjUtNS44OTM4OTggMS4yMzEzODItNS44MjIxNjdMNy4zNzYzMzktMi45ODg3OTJMMS4yMTk0MjctLjE0MzQ2MkMuOTgwMzI0LS4wMzU4NjYgLjk4MDMyNCAuMDQ3ODIxIC45ODAzMjQgLjExOTU1MkMuOTgwMzI0IC4yMTUxOTMgMS4wNjQwMSAuMzM0NzQ1IDEuMjA3NDcyIC4zMzQ3NDVDMS4yMzEzODIgLjMzNDc0NSAxLjI0MzMzNyAuMzIyNzkgMS40MTA3MSAuMjUxMDU5TDcuODc4NDU2LTIuNzI1Nzc4WicvPgo8cGF0aCBpZD0nZzQtNzAnIGQ9J00zLjU1MDY4NS0zLjg5NzM4NUg0LjY5ODM4MUM1LjYwNjk3NC0zLjg5NzM4NSA1LjY3ODcwNS0zLjY5NDE0NyA1LjY3ODcwNS0zLjM0NzQ0N0M1LjY3ODcwNS0zLjE5MjAzIDUuNjU0Nzk1LTMuMDI0NjU4IDUuNTk1MDE5LTIuNzYxNjQ0QzUuNTcxMTA4LTIuNzEzODIzIDUuNTU5MTUzLTIuNjU0MDQ3IDUuNTU5MTUzLTIuNjMwMTM3QzUuNTU5MTUzLTIuNTQ2NDUxIDUuNjA2OTc0LTIuNDk4NjMgNS42OTA2Ni0yLjQ5ODYzQzUuNzg2MzAxLTIuNDk4NjMgNS43OTgyNTctMi41NDY0NTEgNS44NDYwNzctMi43Mzc3MzNMNi41Mzk0NzctNS41MjMyODhDNi41Mzk0NzctNS41NzExMDggNi41MDM2MTEtNS42NDI4MzkgNi40MTk5MjUtNS42NDI4MzlDNi4zMTIzMjktNS42NDI4MzkgNi4zMDAzNzQtNS41OTUwMTkgNi4yNTI1NTMtNS4zOTE3ODFDNi4wMDE0OTQtNC40OTUxNDMgNS43NjIzOTEtNC4yNDQwODUgNC43MjIyOTEtNC4yNDQwODVIMy42MzQzNzFMNC40MTE0NTctNy4zNDA0NzNDNC41MTkwNTQtNy43NTg5MDQgNC41NDI5NjQtNy43OTQ3NyA1LjAzMzEyNi03Ljc5NDc3SDYuNjM1MTE4QzguMTI5NTE0LTcuNzk0NzcgOC4zNDQ3MDctNy4zNTI0MjggOC4zNDQ3MDctNi41MDM2MTFDOC4zNDQ3MDctNi40MzE4OCA4LjM0NDcwNy02LjE2ODg2NyA4LjMwODg0Mi01Ljg1ODAzMkM4LjI5Njg4Ny01LjgxMDIxMiA4LjI3Mjk3Ni01LjY1NDc5NSA4LjI3Mjk3Ni01LjYwNjk3NEM4LjI3Mjk3Ni01LjUxMTMzMyA4LjMzMjc1Mi01LjQ3NTQ2NyA4LjQwNDQ4My01LjQ3NTQ2N0M4LjQ4ODE2OS01LjQ3NTQ2NyA4LjUzNTk5LTUuNTIzMjg4IDguNTU5OS01LjczODQ4MUw4LjgxMDk1OS03LjgzMDYzNUM4LjgxMDk1OS03Ljg2NjUwMSA4LjgzNDg2OS03Ljk4NjA1MiA4LjgzNDg2OS04LjAwOTk2M0M4LjgzNDg2OS04LjE0MTQ2OSA4LjcyNzI3My04LjE0MTQ2OSA4LjUxMjA4LTguMTQxNDY5SDIuODQ1MzNDMi42MTgxODItOC4xNDE0NjkgMi40OTg2My04LjE0MTQ2OSAyLjQ5ODYzLTcuOTI2Mjc2QzIuNDk4NjMtNy43OTQ3NyAyLjU4MjMxNi03Ljc5NDc3IDIuNzg1NTU0LTcuNzk0NzdDMy41MjY3NzUtNy43OTQ3NyAzLjUyNjc3NS03LjcxMTA4MyAzLjUyNjc3NS03LjU3OTU3N0MzLjUyNjc3NS03LjUxOTgwMSAzLjUxNDgxOS03LjQ3MTk4IDMuNDc4OTU0LTcuMzQwNDczTDEuODY1MDA2LS44ODQ2ODJDMS43NTc0MS0uNDY2MjUyIDEuNzMzNDk5LS4zNDY3IC44OTY2MzgtLjM0NjdDLjY2OTQ4OS0uMzQ2NyAuNTQ5OTM4LS4zNDY3IC41NDk5MzgtLjEzMTUwN0MuNTQ5OTM4IDAgLjY1NzUzNCAwIC43MjkyNjUgMEMuOTU2NDEzIDAgMS4xOTU1MTctLjAyMzkxIDEuNDIyNjY1LS4wMjM5MUgyLjk3NjgzN0MzLjIzOTg1MS0uMDIzOTEgMy41MjY3NzUgMCAzLjc4OTc4OCAwQzMuODk3Mzg1IDAgNC4wNDA4NDcgMCA0LjA0MDg0Ny0uMjE1MTkzQzQuMDQwODQ3LS4zNDY3IDMuOTY5MTE2LS4zNDY3IDMuNzA2MTAyLS4zNDY3QzIuNzYxNjQ0LS4zNDY3IDIuNzM3NzMzLS40MzAzODYgMi43Mzc3MzMtLjYwOTcxNEMyLjczNzczMy0uNjY5NDg5IDIuNzYxNjQ0LS43NjUxMzEgMi43ODU1NTQtLjg0ODgxN0wzLjU1MDY4NS0zLjg5NzM4NVonLz4KPHBhdGggaWQ9J2c0LTg4JyBkPSdNNS42Nzg3MDUtNC44NTM3OThMNC41NTQ5MTktNy40NzE5OEM0LjcxMDMzNi03Ljc1ODkwNCA1LjA2ODk5MS03LjgwNjcyNSA1LjIxMjQ1My03LjgxODY4QzUuMjg0MTg0LTcuODE4NjggNS40MTU2OTEtNy44MzA2MzUgNS40MTU2OTEtOC4wMzM4NzNDNS40MTU2OTEtOC4xNjUzOCA1LjMwODA5NS04LjE2NTM4IDUuMjM2MzY0LTguMTY1MzhDNS4wMzMxMjYtOC4xNjUzOCA0Ljc5NDAyMi04LjE0MTQ2OSA0LjU5MDc4NS04LjE0MTQ2OUgzLjg5NzM4NUMzLjE2ODEyLTguMTQxNDY5IDIuNjQyMDkyLTguMTY1MzggMi42MzAxMzctOC4xNjUzOEMyLjUzNDQ5Ni04LjE2NTM4IDIuNDE0OTQ0LTguMTY1MzggMi40MTQ5NDQtNy45MzgyMzJDMi40MTQ5NDQtNy44MTg2OCAyLjUyMjU0LTcuODE4NjggMi42Nzc5NTgtNy44MTg2OEMzLjM3MTM1Ny03LjgxODY4IDMuNDE5MTc4LTcuNjk5MTI4IDMuNTM4NzMtNy40MTIyMDRMNC45NjEzOTUtNC4wODg2NjdMMi4zNjcxMjMtMS4zMTUwNjhDMS45MzY3MzctLjg0ODgxNyAxLjQyMjY2NS0uMzk0NTIxIC41Mzc5ODMtLjM0NjdDLjM5NDUyMS0uMzM0NzQ1IC4yOTg4NzktLjMzNDc0NSAuMjk4ODc5LS4xMTk1NTJDLjI5ODg3OS0uMDgzNjg2IC4zMTA4MzQgMCAuNDQyMzQxIDBDLjYwOTcxNCAwIC43ODkwNDEtLjAyMzkxIC45NTY0MTMtLjAyMzkxSDEuNTE4MzA2QzEuOTAwODcyLS4wMjM5MSAyLjMxOTMwMyAwIDIuNjg5OTEzIDBDMi43NzM1OTkgMCAyLjkxNzA2MSAwIDIuOTE3MDYxLS4yMTUxOTNDMi45MTcwNjEtLjMzNDc0NSAyLjgzMzM3NS0uMzQ2NyAyLjc2MTY0NC0uMzQ2N0MyLjUyMjU0LS4zNzA2MSAyLjM2NzEyMy0uNTAyMTE3IDIuMzY3MTIzLS42OTM0QzIuMzY3MTIzLS44OTY2MzggMi41MTA1ODUtMS4wNDAxIDIuODU3Mjg1LTEuMzk4NzU1TDMuOTIxMjk1LTIuNTU4NDA2QzQuMTg0MzA5LTIuODMzMzc1IDQuODE3OTMzLTMuNTI2Nzc1IDUuMDgwOTQ2LTMuNzg5Nzg4TDYuMzM2MjM5LS44NDg4MTdDNi4zNDgxOTQtLjgyNDkwNyA2LjM5NjAxNS0uNzA1MzU1IDYuMzk2MDE1LS42OTM0QzYuMzk2MDE1LS41ODU4MDMgNi4xMzMwMDEtLjM3MDYxIDUuNzUwNDM2LS4zNDY3QzUuNjc4NzA1LS4zNDY3IDUuNTQ3MTk4LS4zMzQ3NDUgNS41NDcxOTgtLjExOTU1MkM1LjU0NzE5OCAwIDUuNjY2NzUgMCA1LjcyNjUyNiAwQzUuOTI5NzYzIDAgNi4xNjg4NjctLjAyMzkxIDYuMzcyMTA1LS4wMjM5MUg3LjY4NzE3M0M3LjkwMjM2Ni0uMDIzOTEgOC4xMjk1MTQgMCA4LjMzMjc1MiAwQzguNDE2NDM4IDAgOC41NDc5NDUgMCA4LjU0Nzk0NS0uMjI3MTQ4QzguNTQ3OTQ1LS4zNDY3IDguNDI4Mzk0LS4zNDY3IDguMzIwNzk3LS4zNDY3QzcuNjAzNDg3LS4zNTg2NTUgNy41Nzk1NzctLjQxODQzMSA3LjM3NjMzOS0uODYwNzcyTDUuNzk4MjU3LTQuNTY2ODc0TDcuMzE2NTYzLTYuMTkyNzc3QzcuNDM2MTE1LTYuMzEyMzI5IDcuNzExMDgzLTYuNjExMjA4IDcuODE4NjgtNi43MzA3NkM4LjMzMjc1Mi03LjI2ODc0MiA4LjgxMDk1OS03Ljc1ODkwNCA5Ljc3OTMyOC03LjgxODY4QzkuODk4ODc5LTcuODMwNjM1IDEwLjAxODQzMS03LjgzMDYzNSAxMC4wMTg0MzEtOC4wMzM4NzNDMTAuMDE4NDMxLTguMTY1MzggOS45MTA4MzQtOC4xNjUzOCA5Ljg2MzAxNC04LjE2NTM4QzkuNjk1NjQxLTguMTY1MzggOS41MTYzMTQtOC4xNDE0NjkgOS4zNDg5NDEtOC4xNDE0NjlIOC43OTkwMDRDOC40MTY0MzgtOC4xNDE0NjkgNy45OTgwMDctOC4xNjUzOCA3LjYyNzM5Ny04LjE2NTM4QzcuNTQzNzExLTguMTY1MzggNy40MDAyNDktOC4xNjUzOCA3LjQwMDI0OS03Ljk1MDE4N0M3LjQwMDI0OS03LjgzMDYzNSA3LjQ4MzkzNS03LjgxODY4IDcuNTU1NjY2LTcuODE4NjhDNy43NDY5NDktNy43OTQ3NyA3Ljk1MDE4Ny03LjY5OTEyOCA3Ljk1MDE4Ny03LjQ3MTk4TDcuOTM4MjMyLTcuNDQ4MDdDNy45MjYyNzYtNy4zNjQzODQgNy45MDIzNjYtNy4yNDQ4MzIgNy43NzA4NTktNy4xMDEzN0w1LjY3ODcwNS00Ljg1Mzc5OFonLz4KPHBhdGggaWQ9J2c0LTExNycgZD0nTTQuMDc2NzEyLS42OTM0QzQuMjMyMTMtLjAyMzkxIDQuODA1OTc4IC4xMTk1NTIgNS4wOTI5MDIgLjExOTU1MkM1LjQ3NTQ2NyAuMTE5NTUyIDUuNzYyMzkxLS4xMzE1MDcgNS45NTM2NzQtLjUzNzk4M0M2LjE1NjkxMi0uOTY4MzY5IDYuMzEyMzI5LTEuNjczNzI0IDYuMzEyMzI5LTEuNzA5NTg5QzYuMzEyMzI5LTEuNzY5MzY1IDYuMjY0NTA4LTEuODE3MTg2IDYuMTkyNzc3LTEuODE3MTg2QzYuMDg1MTgxLTEuODE3MTg2IDYuMDczMjI1LTEuNzU3NDEgNi4wMjU0MDUtMS41NzgwODJDNS44MTAyMTItLjc1MzE3NiA1LjU5NTAxOS0uMTE5NTUyIDUuMTE2ODEyLS4xMTk1NTJDNC43NTgxNTctLjExOTU1MiA0Ljc1ODE1Ny0uNTE0MDcyIDQuNzU4MTU3LS42Njk0ODlDNC43NTgxNTctLjk0NDQ1OCA0Ljc5NDAyMi0xLjA2NDAxIDQuOTEzNTc0LTEuNTY2MTI3QzQuOTk3MjYtMS44ODg5MTcgNS4wODA5NDYtMi4yMTE3MDYgNS4xNTI2NzctMi41NDY0NTFMNS42NDI4MzktNC40OTUxNDNDNS43MjY1MjYtNC43OTQwMjIgNS43MjY1MjYtNC44MTc5MzMgNS43MjY1MjYtNC44NTM3OThDNS43MjY1MjYtNS4wMzMxMjYgNS41ODMwNjQtNS4xNTI2NzcgNS40MDM3MzYtNS4xNTI2NzdDNS4wNTcwMzYtNS4xNTI2NzcgNC45NzMzNS00Ljg1Mzc5OCA0LjkwMTYxOS00LjU1NDkxOUM0Ljc4MjA2Ny00LjA4ODY2NyA0LjEzNjQ4OC0xLjUxODMwNiA0LjA1MjgwMi0xLjA5OTg3NUM0LjA0MDg0Ny0xLjA5OTg3NSAzLjU3NDU5NS0uMTE5NTUyIDIuNzAxODY4LS4xMTk1NTJDMi4wODAxOTktLjExOTU1MiAxLjk2MDY0OC0uNjU3NTM0IDEuOTYwNjQ4LTEuMDk5ODc1QzEuOTYwNjQ4LTEuNzgxMzIgMi4yOTUzOTItMi43Mzc3MzMgMi42MDYyMjctMy41Mzg3M0MyLjc0OTY4OS0zLjkyMTI5NSAyLjgwOTQ2NS00LjA3NjcxMiAyLjgwOTQ2NS00LjMxNTgxNkMyLjgwOTQ2NS00LjgyOTg4OCAyLjQzODg1NC01LjI3MjIyOSAxLjg2NTAwNi01LjI3MjIyOUMuNzY1MTMxLTUuMjcyMjI5IC4zMjI3OS0zLjUzODczIC4zMjI3OS0zLjQ0MzA4OEMuMzIyNzktMy4zOTUyNjggLjM3MDYxLTMuMzM1NDkyIC40NTQyOTYtMy4zMzU0OTJDLjU2MTg5My0zLjMzNTQ5MiAuNTczODQ4LTMuMzgzMzEzIC42MjE2NjktMy41NTA2ODVDLjkwODU5My00LjU3ODgyOSAxLjM3NDg0NC01LjAzMzEyNiAxLjgyOTE0MS01LjAzMzEyNkMxLjk0ODY5Mi01LjAzMzEyNiAyLjEzOTk3NS01LjAyMTE3MSAyLjEzOTk3NS00LjYzODYwNUMyLjEzOTk3NS00LjMyNzc3MSAyLjAwODQ2OC0zLjk4MTA3MSAxLjgyOTE0MS0zLjUyNjc3NUMxLjMwMzExMy0yLjEwNDExIDEuMjQzMzM3LTEuNjQ5ODEzIDEuMjQzMzM3LTEuMjkxMTU4QzEuMjQzMzM3LS4wNzE3MzEgMi4xNjM4ODUgLjExOTU1MiAyLjY1NDA0NyAuMTE5NTUyQzMuNDE5MTc4IC4xMTk1NTIgMy44Mzc2MDktLjQwNjQ3NiA0LjA3NjcxMi0uNjkzNFonLz4KPC9kZWZzPgo8ZyBpZD0ncGFnZTEnPgo8dXNlIHg9JzkxLjI3MTAxNScgeT0nLTguMzY4NjEyJyB4bGluazpocmVmPScjZzQtMjEnLz4KPHVzZSB4PSc5OC4wOTk1MDQnIHk9Jy02LjU3NTM0OScgeGxpbms6aHJlZj0nI2czLTg1Jy8+Cjx1c2UgeD0nMTA4LjQ5NjM2NycgeT0nLTguMzY4NjEyJyB4bGluazpocmVmPScjZzYtNjEnLz4KPHVzZSB4PScxMjAuOTIxODQ4JyB5PSctOC4zNjg2MTInIHhsaW5rOmhyZWY9JyNnNC0zMScvPgo8dXNlIHg9JzEzMS41NzYyMzQnIHk9Jy04LjM2ODYxMicgeGxpbms6aHJlZj0nI2c2LTYxJy8+Cjx1c2UgeD0nMTQ0LjY3NTMyMScgeT0nLTguMzY4NjEyJyB4bGluazpocmVmPScjZzYtMTA4Jy8+Cjx1c2UgeD0nMTQ3LjkyNjk4MicgeT0nLTguMzY4NjEyJyB4bGluazpocmVmPScjZzYtMTA1Jy8+Cjx1c2UgeD0nMTUxLjE3ODY0NCcgeT0nLTguMzY4NjEyJyB4bGluazpocmVmPScjZzYtMTA5Jy8+Cjx1c2UgeD0nMTQ0LjAwMTcxNScgeT0nLTEuMTk1NTE0JyB4bGluazpocmVmPScjZzMtMTE3Jy8+Cjx1c2UgeD0nMTQ4LjkwNDY4NScgeT0nLTEuMTk1NTE0JyB4bGluazpocmVmPScjZzEtMzMnLz4KPHVzZSB4PScxNTcuMzczMDUxJyB5PSctMS4xOTU1MTQnIHhsaW5rOmhyZWY9JyNnNS00OScvPgo8dXNlIHg9JzE2My41OTk3MzEnIHk9Jy04LjM2ODYxMicgeGxpbms6aHJlZj0nI2cwLTgwJy8+Cjx1c2UgeD0nMTcwLjkwNTY4NScgeT0nLTguMzY4NjEyJyB4bGluazpocmVmPScjZzYtOTEnLz4KPHVzZSB4PScxNzQuMTU3MzQ2JyB5PSctOC4zNjg2MTInIHhsaW5rOmhyZWY9JyNnNC03MCcvPgo8dXNlIHg9JzE4MS43MzUxMzEnIHk9Jy02LjU3NTM0OScgeGxpbms6aHJlZj0nI2c1LTUwJy8+Cjx1c2UgeD0nMTg2LjQ2NzQ0NicgeT0nLTguMzY4NjEyJyB4bGluazpocmVmPScjZzYtNDAnLz4KPHVzZSB4PScxOTEuMDE5NzcxJyB5PSctOC4zNjg2MTInIHhsaW5rOmhyZWY9JyNnNC04OCcvPgo8dXNlIHg9JzIwMC43MzQ5OTknIHk9Jy02LjU3NTM0OScgeGxpbms6aHJlZj0nI2c1LTUwJy8+Cjx1c2UgeD0nMjA1LjQ2NzMxMycgeT0nLTguMzY4NjEyJyB4bGluazpocmVmPScjZzYtNDEnLz4KPHVzZSB4PScyMTMuMzQwNDY5JyB5PSctOC4zNjg2MTInIHhsaW5rOmhyZWY9JyNnNC02MicvPgo8dXNlIHg9JzIyNS43NjU5NDknIHk9Jy04LjM2ODYxMicgeGxpbms6aHJlZj0nI2c0LTExNycvPgo8dXNlIHg9JzIzMi40MjgzODknIHk9Jy04LjM2ODYxMicgeGxpbms6aHJlZj0nI2cyLTEwNicvPgo8dXNlIHg9JzIzNS43NDkyNzknIHk9Jy04LjM2ODYxMicgeGxpbms6aHJlZj0nI2c0LTcwJy8+Cjx1c2UgeD0nMjQzLjMyNzA2NCcgeT0nLTYuNTc1MzQ5JyB4bGluazpocmVmPScjZzUtNDknLz4KPHVzZSB4PScyNDguMDU5Mzc4JyB5PSctOC4zNjg2MTInIHhsaW5rOmhyZWY9JyNnNi00MCcvPgo8dXNlIHg9JzI1Mi42MTE3MDQnIHk9Jy04LjM2ODYxMicgeGxpbms6aHJlZj0nI2c0LTg4Jy8+Cjx1c2UgeD0nMjYyLjMyNjkzMicgeT0nLTYuNTc1MzQ5JyB4bGluazpocmVmPScjZzUtNDknLz4KPHVzZSB4PScyNjcuMDU5MjQ2JyB5PSctOC4zNjg2MTInIHhsaW5rOmhyZWY9JyNnNi00MScvPgo8dXNlIHg9JzI3NC45MzI0MDEnIHk9Jy04LjM2ODYxMicgeGxpbms6aHJlZj0nI2c0LTYyJy8+Cjx1c2UgeD0nMjg3LjM1Nzg4MicgeT0nLTguMzY4NjEyJyB4bGluazpocmVmPScjZzQtMTE3Jy8+Cjx1c2UgeD0nMjk0LjAyMDMyMicgeT0nLTguMzY4NjEyJyB4bGluazpocmVmPScjZzYtOTMnLz4KPC9nPgo8L3N2Zz4KPCEtLSBERVBUSD0wIC0tPg==)

provided that the limit exists.

The coefficient can be interpreted as the tendency for one variable to take extreme high values

given that the other variable is extremely high.

The variables  are said to be:

are said to be:

asymptotically independent if and only if

,

,asymptotically dependent if and only if

.

.

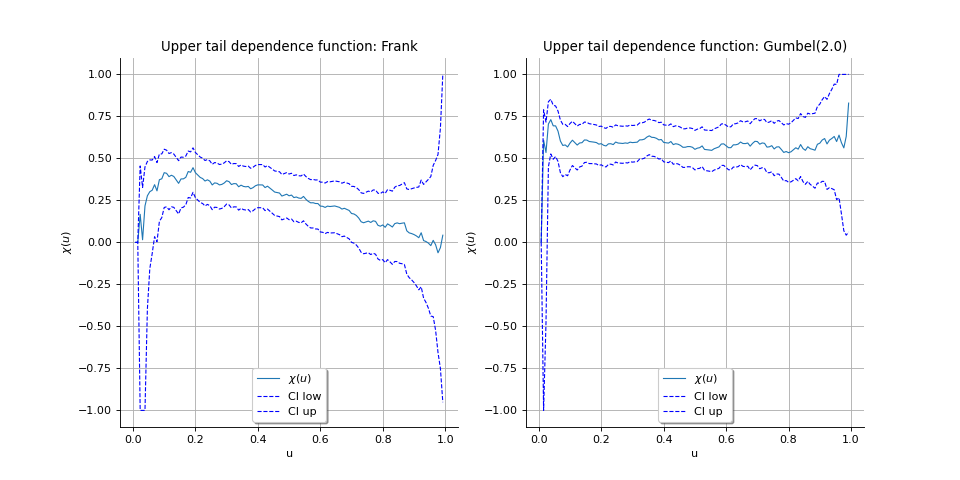

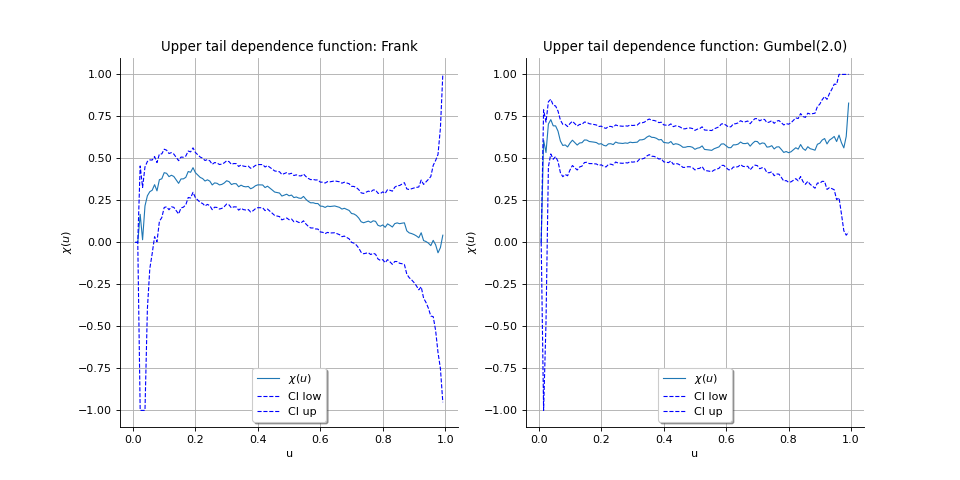

Now, we define the function  defined by:

defined by:

![\chi(u) = 2 - \frac{\log C(u,u)}{\log u}, \forall u \in [0,1]](data:image/svg+xml;base64,PD94bWwgdmVyc2lvbj0nMS4wJyBlbmNvZGluZz0nVVRGLTgnPz4KPCEtLSBUaGlzIGZpbGUgd2FzIGdlbmVyYXRlZCBieSBkdmlzdmdtIDMuMyAtLT4KPHN2ZyB2ZXJzaW9uPScxLjEnIHhtbG5zPSdodHRwOi8vd3d3LnczLm9yZy8yMDAwL3N2ZycgeG1sbnM6eGxpbms9J2h0dHA6Ly93d3cudzMub3JnLzE5OTkveGxpbmsnIHdpZHRoPScxNzIuMzM2NDU4cHQnIGhlaWdodD0nMjcuNTc5NDA0cHQnIHZpZXdCb3g9JzEwOC4xMDMyNjQgLTI3LjU3OTM5MyAxNzIuMzM2NDU4IDI3LjU3OTQwNCc+CjxkZWZzPgo8cGF0aCBpZD0nZzAtMCcgZD0nTTcuODc4NDU2LTIuNzQ5Njg5QzguMDgxNjk0LTIuNzQ5Njg5IDguMjk2ODg3LTIuNzQ5Njg5IDguMjk2ODg3LTIuOTg4NzkyUzguMDgxNjk0LTMuMjI3ODk1IDcuODc4NDU2LTMuMjI3ODk1SDEuNDEwNzFDMS4yMDc0NzItMy4yMjc4OTUgLjk5MjI3OS0zLjIyNzg5NSAuOTkyMjc5LTIuOTg4NzkyUzEuMjA3NDcyLTIuNzQ5Njg5IDEuNDEwNzEtMi43NDk2ODlINy44Nzg0NTZaJy8+CjxwYXRoIGlkPSdnMC01MCcgZD0nTTYuNTUxNDMyLTIuNzQ5Njg5QzYuNzU0NjctMi43NDk2ODkgNi45Njk4NjMtMi43NDk2ODkgNi45Njk4NjMtMi45ODg3OTJTNi43NTQ2Ny0zLjIyNzg5NSA2LjU1MTQzMi0zLjIyNzg5NUgxLjQ4MjQ0MUMxLjYyNTkwMy00LjgyOTg4OCAzLjAwMDc0Ny01Ljk3NzU4NCA0LjY4NjQyNi01Ljk3NzU4NEg2LjU1MTQzMkM2Ljc1NDY3LTUuOTc3NTg0IDYuOTY5ODYzLTUuOTc3NTg0IDYuOTY5ODYzLTYuMjE2Njg3UzYuNzU0NjctNi40NTU3OTEgNi41NTE0MzItNi40NTU3OTFINC42NjI1MTZDMi42MTgxODItNi40NTU3OTEgLjk5MjI3OS00LjkwMTYxOSAuOTkyMjc5LTIuOTg4NzkyUzIuNjE4MTgyIC40NzgyMDcgNC42NjI1MTYgLjQ3ODIwN0g2LjU1MTQzMkM2Ljc1NDY3IC40NzgyMDcgNi45Njk4NjMgLjQ3ODIwNyA2Ljk2OTg2MyAuMjM5MTAzUzYuNzU0NjcgMCA2LjU1MTQzMiAwSDQuNjg2NDI2QzMuMDAwNzQ3IDAgMS42MjU5MDMtMS4xNDc2OTYgMS40ODI0NDEtMi43NDk2ODlINi41NTE0MzJaJy8+CjxwYXRoIGlkPSdnMC01NicgZD0nTTYuNTg3Mjk4LTcuODQyNTlDNi42NDcwNzMtNy45NzQwOTcgNi42NDcwNzMtNy45OTgwMDcgNi42NDcwNzMtOC4wNTc3ODNDNi42NDcwNzMtOC4xNzczMzUgNi41NTE0MzItOC4yOTY4ODcgNi40MDc5Ny04LjI5Njg4N0M2LjI1MjU1My04LjI5Njg4NyA2LjE4MDgyMi04LjE1MzQyNSA2LjEzMzAwMS04LjAyMTkxOEw1LjE0MDcyMi01LjM5MTc4MUgxLjUwNjM1MUwuNTE0MDcyLTguMDIxOTE4Qy40NTQyOTYtOC4xODkyOSAuMzk0NTIxLTguMjk2ODg3IC4yMzkxMDMtOC4yOTY4ODdDLjExOTU1Mi04LjI5Njg4NyAwLTguMTc3MzM1IDAtOC4wNTc3ODNDMC04LjAzMzg3MyAwLTguMDA5OTYzIC4wNzE3MzEtNy44NDI1OUwzLjA0ODU2OC0uMDExOTU1QzMuMTA4MzQ0IC4xNTU0MTcgMy4xNjgxMiAuMjYzMDE0IDMuMzIzNTM3IC4yNjMwMTRDMy40OTA5MDkgLjI2MzAxNCAzLjUzODczIC4xMzE1MDcgMy41ODY1NSAuMDExOTU1TDYuNTg3Mjk4LTcuODQyNTlaTTEuNjk3NjM0LTQuOTEzNTc0SDQuOTQ5NDRMMy4zMjM1MzctLjY1NzUzNEwxLjY5NzYzNC00LjkxMzU3NFonLz4KPHBhdGggaWQ9J2cyLTQwJyBkPSdNMy44ODU0MyAyLjkwNTEwNkMzLjg4NTQzIDIuODY5MjQgMy44ODU0MyAyLjg0NTMzIDMuNjgyMTkyIDIuNjQyMDkyQzIuNDg2Njc1IDEuNDM0NjIgMS44MTcxODYtLjUzNzk4MyAxLjgxNzE4Ni0yLjk3NjgzN0MxLjgxNzE4Ni01LjI5NjEzOSAyLjM3OTA3OC03LjI5MjY1MyAzLjc2NTg3OC04LjcwMzM2MkMzLjg4NTQzLTguODEwOTU5IDMuODg1NDMtOC44MzQ4NjkgMy44ODU0My04Ljg3MDczNUMzLjg4NTQzLTguOTQyNDY2IDMuODI1NjU0LTguOTY2Mzc2IDMuNzc3ODMzLTguOTY2Mzc2QzMuNjIyNDE2LTguOTY2Mzc2IDIuNjQyMDkyLTguMTA1NjA0IDIuMDU2Mjg5LTYuOTMzOTk4QzEuNDQ2NTc1LTUuNzI2NTI2IDEuMTcxNjA2LTQuNDQ3MzIzIDEuMTcxNjA2LTIuOTc2ODM3QzEuMTcxNjA2LTEuOTEyODI3IDEuMzM4OTc5LS40OTAxNjIgMS45NjA2NDggLjc4OTA0MUMyLjY2NjAwMiAyLjIyMzY2MSAzLjY0NjMyNiAzLjAwMDc0NyAzLjc3NzgzMyAzLjAwMDc0N0MzLjgyNTY1NCAzLjAwMDc0NyAzLjg4NTQzIDIuOTc2ODM3IDMuODg1NDMgMi45MDUxMDZaJy8+CjxwYXRoIGlkPSdnMi00MScgZD0nTTMuMzcxMzU3LTIuOTc2ODM3QzMuMzcxMzU3LTMuODg1NDMgMy4yNTE4MDYtNS4zNjc4NyAyLjU4MjMxNi02Ljc1NDY3QzEuODc2OTYxLTguMTg5MjkgLjg5NjYzOC04Ljk2NjM3NiAuNzY1MTMxLTguOTY2Mzc2Qy43MTczMS04Ljk2NjM3NiAuNjU3NTM0LTguOTQyNDY2IC42NTc1MzQtOC44NzA3MzVDLjY1NzUzNC04LjgzNDg2OSAuNjU3NTM0LTguODEwOTU5IC44NjA3NzItOC42MDc3MjFDMi4wNTYyODktNy40MDAyNDkgMi43MjU3NzgtNS40Mjc2NDYgMi43MjU3NzgtMi45ODg3OTJDMi43MjU3NzgtLjY2OTQ4OSAyLjE2Mzg4NSAxLjMyNzAyNCAuNzc3MDg2IDIuNzM3NzMzQy42NTc1MzQgMi44NDUzMyAuNjU3NTM0IDIuODY5MjQgLjY1NzUzNCAyLjkwNTEwNkMuNjU3NTM0IDIuOTc2ODM3IC43MTczMSAzLjAwMDc0NyAuNzY1MTMxIDMuMDAwNzQ3Qy45MjA1NDggMy4wMDA3NDcgMS45MDA4NzIgMi4xMzk5NzUgMi40ODY2NzUgLjk2ODM2OUMzLjA5NjM4OS0uMjUxMDU5IDMuMzcxMzU3LTEuNTQyMjE3IDMuMzcxMzU3LTIuOTc2ODM3WicvPgo8cGF0aCBpZD0nZzItNDgnIGQ9J001LjM1NTkxNS0zLjgyNTY1NEM1LjM1NTkxNS00LjgxNzkzMyA1LjI5NjEzOS01Ljc4NjMwMSA0Ljg2NTc1My02LjY5NDg5NEM0LjM3NTU5Mi03LjY4NzE3MyAzLjUxNDgxOS03Ljk1MDE4NyAyLjkyOTAxNi03Ljk1MDE4N0MyLjIzNTYxNi03Ljk1MDE4NyAxLjM4NjgtNy42MDM0ODcgLjk0NDQ1OC02LjYxMTIwOEMuNjA5NzE0LTUuODU4MDMyIC40OTAxNjItNS4xMTY4MTIgLjQ5MDE2Mi0zLjgyNTY1NEMuNDkwMTYyLTIuNjY2MDAyIC41NzM4NDgtMS43OTMyNzUgMS4wMDQyMzQtLjk0NDQ1OEMxLjQ3MDQ4Ni0uMDM1ODY2IDIuMjk1MzkyIC4yNTEwNTkgMi45MTcwNjEgLjI1MTA1OUMzLjk1NzE2MSAuMjUxMDU5IDQuNTU0OTE5LS4zNzA2MSA0LjkwMTYxOS0xLjA2NDAxQzUuMzMyMDA1LTEuOTYwNjQ4IDUuMzU1OTE1LTMuMTMyMjU0IDUuMzU1OTE1LTMuODI1NjU0Wk0yLjkxNzA2MSAuMDExOTU1QzIuNTM0NDk2IC4wMTE5NTUgMS43NTc0MS0uMjAzMjM4IDEuNTMwMjYyLTEuNTA2MzUxQzEuMzk4NzU1LTIuMjIzNjYxIDEuMzk4NzU1LTMuMTMyMjU0IDEuMzk4NzU1LTMuOTY5MTE2QzEuMzk4NzU1LTQuOTQ5NDQgMS4zOTg3NTUtNS44MzQxMjIgMS41OTAwMzctNi41Mzk0NzdDMS43OTMyNzUtNy4zNDA0NzMgMi40MDI5ODktNy43MTEwODMgMi45MTcwNjEtNy43MTEwODNDMy4zNzEzNTctNy43MTEwODMgNC4wNjQ3NTctNy40MzYxMTUgNC4yOTE5MDUtNi40MDc5N0M0LjQ0NzMyMy01LjcyNjUyNiA0LjQ0NzMyMy00Ljc4MjA2NyA0LjQ0NzMyMy0zLjk2OTExNkM0LjQ0NzMyMy0zLjE2ODEyIDQuNDQ3MzIzLTIuMjU5NTI3IDQuMzE1ODE2LTEuNTMwMjYyQzQuMDg4NjY3LS4yMTUxOTMgMy4zMzU0OTIgLjAxMTk1NSAyLjkxNzA2MSAuMDExOTU1WicvPgo8cGF0aCBpZD0nZzItNDknIGQ9J00zLjQ0MzA4OC03LjY2MzI2M0MzLjQ0MzA4OC03LjkzODIzMiAzLjQ0MzA4OC03Ljk1MDE4NyAzLjIwMzk4NS03Ljk1MDE4N0MyLjkxNzA2MS03LjYyNzM5NyAyLjMxOTMwMy03LjE4NTA1NiAxLjA4NzkyLTcuMTg1MDU2Vi02LjgzODM1NkMxLjM2Mjg4OS02LjgzODM1NiAxLjk2MDY0OC02LjgzODM1NiAyLjYxODE4Mi03LjE0OTE5MVYtLjkyMDU0OEMyLjYxODE4Mi0uNDkwMTYyIDIuNTgyMzE2LS4zNDY3IDEuNTMwMjYyLS4zNDY3SDEuMTU5NjUxVjBDMS40ODI0NDEtLjAyMzkxIDIuNjQyMDkyLS4wMjM5MSAzLjAzNjYxMy0uMDIzOTFTNC41Nzg4MjktLjAyMzkxIDQuOTAxNjE5IDBWLS4zNDY3SDQuNTMxMDA5QzMuNDc4OTU0LS4zNDY3IDMuNDQzMDg4LS40OTAxNjIgMy40NDMwODgtLjkyMDU0OFYtNy42NjMyNjNaJy8+CjxwYXRoIGlkPSdnMi01MCcgZD0nTTUuMjYwMjc0LTIuMDA4NDY4SDQuOTk3MjZDNC45NjEzOTUtMS44MDUyMyA0Ljg2NTc1My0xLjE0NzY5NiA0Ljc0NjIwMi0uOTU2NDEzQzQuNjYyNTE2LS44NDg4MTcgMy45ODEwNzEtLjg0ODgxNyAzLjYyMjQxNi0uODQ4ODE3SDEuNDEwNzFDMS43MzM0OTktMS4xMjM3ODYgMi40NjI3NjUtMS44ODg5MTcgMi43NzM1OTktMi4xNzU4NDFDNC41OTA3ODUtMy44NDk1NjQgNS4yNjAyNzQtNC40NzEyMzMgNS4yNjAyNzQtNS42NTQ3OTVDNS4yNjAyNzQtNy4wMjk2MzkgNC4xNzIzNTQtNy45NTAxODcgMi43ODU1NTQtNy45NTAxODdTLjU4NTgwMy02Ljc2NjYyNSAuNTg1ODAzLTUuNzM4NDgxQy41ODU4MDMtNS4xMjg3NjcgMS4xMTE4MzEtNS4xMjg3NjcgMS4xNDc2OTYtNS4xMjg3NjdDMS4zOTg3NTUtNS4xMjg3NjcgMS43MDk1ODktNS4zMDgwOTUgMS43MDk1ODktNS42OTA2NkMxLjcwOTU4OS02LjAyNTQwNSAxLjQ4MjQ0MS02LjI1MjU1MyAxLjE0NzY5Ni02LjI1MjU1M0MxLjA0MDEtNi4yNTI1NTMgMS4wMTYxODktNi4yNTI1NTMgLjk4MDMyNC02LjI0MDU5OEMxLjIwNzQ3Mi03LjA1MzU0OSAxLjg1MzA1MS03LjYwMzQ4NyAyLjYzMDEzNy03LjYwMzQ4N0MzLjY0NjMyNi03LjYwMzQ4NyA0LjI2Nzk5NS02Ljc1NDY3IDQuMjY3OTk1LTUuNjU0Nzk1QzQuMjY3OTk1LTQuNjM4NjA1IDMuNjgyMTkyLTMuNzUzOTIzIDMuMDAwNzQ3LTIuOTg4NzkyTC41ODU4MDMtLjI4NjkyNFYwSDQuOTQ5NDRMNS4yNjAyNzQtMi4wMDg0NjhaJy8+CjxwYXRoIGlkPSdnMi02MScgZD0nTTguMDY5NzM4LTMuODczNDc0QzguMjM3MTExLTMuODczNDc0IDguNDUyMzA0LTMuODczNDc0IDguNDUyMzA0LTQuMDg4NjY3QzguNDUyMzA0LTQuMzE1ODE2IDguMjQ5MDY2LTQuMzE1ODE2IDguMDY5NzM4LTQuMzE1ODE2SDEuMDI4MTQ0Qy44NjA3NzItNC4zMTU4MTYgLjY0NTU3OS00LjMxNTgxNiAuNjQ1NTc5LTQuMTAwNjIzQy42NDU1NzktMy44NzM0NzQgLjg0ODgxNy0zLjg3MzQ3NCAxLjAyODE0NC0zLjg3MzQ3NEg4LjA2OTczOFpNOC4wNjk3MzgtMS42NDk4MTNDOC4yMzcxMTEtMS42NDk4MTMgOC40NTIzMDQtMS42NDk4MTMgOC40NTIzMDQtMS44NjUwMDZDOC40NTIzMDQtMi4wOTIxNTQgOC4yNDkwNjYtMi4wOTIxNTQgOC4wNjk3MzgtMi4wOTIxNTRIMS4wMjgxNDRDLjg2MDc3Mi0yLjA5MjE1NCAuNjQ1NTc5LTIuMDkyMTU0IC42NDU1NzktMS44NzY5NjFDLjY0NTU3OS0xLjY0OTgxMyAuODQ4ODE3LTEuNjQ5ODEzIDEuMDI4MTQ0LTEuNjQ5ODEzSDguMDY5NzM4WicvPgo8cGF0aCBpZD0nZzItOTEnIGQ9J00yLjk4ODc5MiAyLjk4ODc5MlYyLjU0NjQ1MUgxLjgyOTE0MVYtOC41MjQwMzVIMi45ODg3OTJWLTguOTY2Mzc2SDEuMzg2OFYyLjk4ODc5MkgyLjk4ODc5MlonLz4KPHBhdGggaWQ9J2cyLTkzJyBkPSdNMS44NTMwNTEtOC45NjYzNzZILjI1MTA1OVYtOC41MjQwMzVIMS40MTA3MVYyLjU0NjQ1MUguMjUxMDU5VjIuOTg4NzkySDEuODUzMDUxVi04Ljk2NjM3NlonLz4KPHBhdGggaWQ9J2cyLTEwMycgZD0nTTEuNDIyNjY1LTIuMTYzODg1QzEuOTg0NTU4LTEuNzkzMjc1IDIuNDYyNzY1LTEuNzkzMjc1IDIuNTk0MjcxLTEuNzkzMjc1QzMuNjcwMjM3LTEuNzkzMjc1IDQuNDcxMjMzLTIuNjA2MjI3IDQuNDcxMjMzLTMuNTI2Nzc1QzQuNDcxMjMzLTMuODQ5NTY0IDQuMzc1NTkyLTQuMzAzODYxIDMuOTkzMDI2LTQuNjg2NDI2QzQuNDU5Mjc4LTUuMTY0NjMzIDUuMDIxMTcxLTUuMTY0NjMzIDUuMDgwOTQ2LTUuMTY0NjMzQzUuMTI4NzY3LTUuMTY0NjMzIDUuMTg4NTQzLTUuMTY0NjMzIDUuMjM2MzY0LTUuMTQwNzIyQzUuMTE2ODEyLTUuMDkyOTAyIDUuMDU3MDM2LTQuOTczMzUgNS4wNTcwMzYtNC44NDE4NDNDNS4wNTcwMzYtNC42NzQ0NzEgNS4xNzY1ODgtNC41MzEwMDkgNS4zNjc4Ny00LjUzMTAwOUM1LjQ2MzUxMi00LjUzMTAwOSA1LjY3ODcwNS00LjU5MDc4NSA1LjY3ODcwNS00Ljg1Mzc5OEM1LjY3ODcwNS01LjA2ODk5MSA1LjUxMTMzMy01LjQwMzczNiA1LjA5MjkwMi01LjQwMzczNkM0LjQ3MTIzMy01LjQwMzczNiA0LjAwNDk4MS01LjAyMTE3MSAzLjgzNzYwOS00Ljg0MTg0M0MzLjQ3ODk1NC01LjExNjgxMiAzLjA2MDUyMy01LjI3MjIyOSAyLjYwNjIyNy01LjI3MjIyOUMxLjUzMDI2Mi01LjI3MjIyOSAuNzI5MjY1LTQuNDU5Mjc4IC43MjkyNjUtMy41Mzg3M0MuNzI5MjY1LTIuODU3Mjg1IDEuMTQ3Njk2LTIuNDE0OTQ0IDEuMjY3MjQ4LTIuMzA3MzQ3QzEuMTIzNzg2LTIuMTI4MDIgLjkwODU5My0xLjc4MTMyIC45MDg1OTMtMS4zMTUwNjhDLjkwODU5My0uNjIxNjY5IDEuMzI3MDI0LS4zMjI3OSAxLjQyMjY2NS0uMjYzMDE0Qy44NzI3MjctLjEwNzU5NyAuMzIyNzkgLjMyMjc5IC4zMjI3OSAuOTQ0NDU4Qy4zMjI3OSAxLjc2OTM2NSAxLjQ0NjU3NSAyLjQ1MDgwOSAyLjkxNzA2MSAyLjQ1MDgwOUM0LjMzOTcyNiAyLjQ1MDgwOSA1LjUyMzI4OCAxLjgxNzE4NiA1LjUyMzI4OCAuOTIwNTQ4QzUuNTIzMjg4IC42MjE2NjkgNS40Mzk2MDEtLjA4MzY4NiA0LjcyMjI5MS0uNDU0Mjk2QzQuMTEyNTc4LS43NjUxMzEgMy41MTQ4MTktLjc2NTEzMSAyLjQ4NjY3NS0uNzY1MTMxQzEuNzU3NDEtLjc2NTEzMSAxLjY3MzcyNC0uNzY1MTMxIDEuNDU4NTMxLS45OTIyNzlDMS4zMzg5NzktMS4xMTE4MzEgMS4yMzEzODItMS4zMzg5NzkgMS4yMzEzODItMS41OTAwMzdDMS4yMzEzODItMS43OTMyNzUgMS4zMDMxMTMtMS45OTY1MTMgMS40MjI2NjUtMi4xNjM4ODVaTTIuNjA2MjI3LTIuMDQ0MzM0QzEuNTU0MTcyLTIuMDQ0MzM0IDEuNTU0MTcyLTMuMjUxODA2IDEuNTU0MTcyLTMuNTI2Nzc1QzEuNTU0MTcyLTMuNzQxOTY4IDEuNTU0MTcyLTQuMjMyMTMgMS43NTc0MS00LjU1NDkxOUMxLjk4NDU1OC00LjkwMTYxOSAyLjM0MzIxMy01LjAyMTE3MSAyLjU5NDI3MS01LjAyMTE3MUMzLjY0NjMyNi01LjAyMTE3MSAzLjY0NjMyNi0zLjgxMzY5OSAzLjY0NjMyNi0zLjUzODczQzMuNjQ2MzI2LTMuMzIzNTM3IDMuNjQ2MzI2LTIuODMzMzc1IDMuNDQzMDg4LTIuNTEwNTg1QzMuMjE1OTQtMi4xNjM4ODUgMi44NTcyODUtMi4wNDQzMzQgMi42MDYyMjctMi4wNDQzMzRaTTIuOTI5MDE2IDIuMTk5NzUxQzEuNzgxMzIgMi4xOTk3NTEgLjkwODU5MyAxLjYxMzk0OCAuOTA4NTkzIC45MzI1MDNDLjkwODU5MyAuODM2ODYyIC45MzI1MDMgLjM3MDYxIDEuMzg2OCAuMDU5Nzc2QzEuNjQ5ODEzLS4xMDc1OTcgMS43NTc0MS0uMTA3NTk3IDIuNTk0MjcxLS4xMDc1OTdDMy41ODY1NS0uMTA3NTk3IDQuOTM3NDg0LS4xMDc1OTcgNC45Mzc0ODQgLjkzMjUwM0M0LjkzNzQ4NCAxLjYzNzg1OCA0LjAyODg5MiAyLjE5OTc1MSAyLjkyOTAxNiAyLjE5OTc1MVonLz4KPHBhdGggaWQ9J2cyLTEwOCcgZD0nTTIuMDU2Mjg5LTguMjk2ODg3TC4zOTQ1MjEtOC4xNjUzOFYtNy44MTg2OEMxLjIwNzQ3Mi03LjgxODY4IDEuMzAzMTEzLTcuNzM0OTk0IDEuMzAzMTEzLTcuMTQ5MTkxVi0uODg0NjgyQzEuMzAzMTEzLS4zNDY3IDEuMTcxNjA2LS4zNDY3IC4zOTQ1MjEtLjM0NjdWMEMuNzI5MjY1LS4wMjM5MSAxLjMxNTA2OC0uMDIzOTEgMS42NzM3MjQtLjAyMzkxUzIuNjMwMTM3LS4wMjM5MSAyLjk2NDg4MiAwVi0uMzQ2N0MyLjE5OTc1MS0uMzQ2NyAyLjA1NjI4OS0uMzQ2NyAyLjA1NjI4OS0uODg0NjgyVi04LjI5Njg4N1onLz4KPHBhdGggaWQ9J2cyLTExMScgZD0nTTUuNDg3NDIyLTIuNTU4NDA2QzUuNDg3NDIyLTQuMTAwNjIzIDQuMzE1ODE2LTUuMzMyMDA1IDIuOTI5MDE2LTUuMzMyMDA1QzEuNDk0Mzk2LTUuMzMyMDA1IC4zNTg2NTUtNC4wNjQ3NTcgLjM1ODY1NS0yLjU1ODQwNkMuMzU4NjU1LTEuMDI4MTQ0IDEuNTU0MTcyIC4xMTk1NTIgMi45MTcwNjEgLjExOTU1MkM0LjMyNzc3MSAuMTE5NTUyIDUuNDg3NDIyLTEuMDUyMDU1IDUuNDg3NDIyLTIuNTU4NDA2Wk0yLjkyOTAxNi0uMTQzNDYyQzIuNDg2Njc1LS4xNDM0NjIgMS45NDg2OTItLjMzNDc0NSAxLjYwMTk5My0uOTIwNTQ4QzEuMjc5MjAzLTEuNDU4NTMxIDEuMjY3MjQ4LTIuMTYzODg1IDEuMjY3MjQ4LTIuNjY2MDAyQzEuMjY3MjQ4LTMuMTIwMjk5IDEuMjY3MjQ4LTMuODQ5NTY0IDEuNjM3ODU4LTQuMzg3NTQ3QzEuOTcyNjAzLTQuOTAxNjE5IDIuNDk4NjMtNS4wOTI5MDIgMi45MTcwNjEtNS4wOTI5MDJDMy4zODMzMTMtNS4wOTI5MDIgMy44ODU0My00Ljg3NzcwOSA0LjIwODIxOS00LjQxMTQ1N0M0LjU3ODgyOS0zLjg2MTUxOSA0LjU3ODgyOS0zLjEwODM0NCA0LjU3ODgyOS0yLjY2NjAwMkM0LjU3ODgyOS0yLjI0NzU3MiA0LjU3ODgyOS0xLjUwNjM1MSA0LjI2Nzk5NS0uOTQ0NDU4QzMuOTMzMjUtLjM3MDYxIDMuMzgzMzEzLS4xNDM0NjIgMi45MjkwMTYtLjE0MzQ2MlonLz4KPHBhdGggaWQ9J2cxLTMxJyBkPSdNMy45NDUyMDUtMS45MjQ3ODJDMy42MjI0MTYtMi45MTcwNjEgMy42OTQxNDctMi44MjE0MiAzLjM5NTI2OC0zLjY1ODI4MUMzLjAyNDY1OC00LjY4NjQyNiAyLjkyOTAxNi00Ljc3MDExMiAyLjc2MTY0NC00LjkzNzQ4NEMyLjU0NjQ1MS01LjEyODc2NyAyLjEzOTk3NS01LjI3MjIyOSAxLjcyMTU0NC01LjI3MjIyOUMxLjA1MjA1NS01LjI3MjIyOSAuNzI5MjY1LTQuNjUwNTYgLjcyOTI2NS00LjQ5NTE0M0MuNzI5MjY1LTQuNDIzNDEyIC43ODkwNDEtNC4zODc1NDcgLjg2MDc3Mi00LjM4NzU0N0MuOTU2NDEzLTQuMzg3NTQ3IC45ODAzMjQtNC40NDczMjMgLjk5MjI3OS00LjQ5NTE0M0MxLjE3MTYwNi00Ljk2MTM5NSAxLjU0MjIxNy01LjAzMzEyNiAxLjY0OTgxMy01LjAzMzEyNkMxLjk5NjUxMy01LjAzMzEyNiAyLjMzMTI1OC00LjE3MjM1NCAyLjU0NjQ1MS0zLjU5ODUwNkMyLjgzMzM3NS0yLjg2OTI0IDIuOTc2ODM3LTIuMzY3MTIzIDMuMjk5NjI2LTEuMjA3NDcyTC40NzgyMDcgMS45OTY1MTNDLjM3MDYxIDIuMTI4MDIgLjM3MDYxIDIuMTc1ODQxIC4zNzA2MSAyLjE4Nzc5NkMuMzcwNjEgMi4yODM0MzcgLjQzMDM4NiAyLjMwNzM0NyAuNDc4MjA3IDIuMzA3MzQ3Uy41NjE4OTMgMi4yODM0MzcgLjU5Nzc1OCAyLjI0NzU3MkMuOTMyNTAzIDEuOTEyODI3IDEuNjczNzI0IDEuMDI4MTQ0IDEuOTg0NTU4IC42Njk0ODlMMy4zNzEzNTctLjkwODU5M0MzLjk1NzE2MSAuOTMyNTAzIDMuOTU3MTYxIC45NTY0MTMgNC4xMzY0ODggMS4zOTg3NTVDNC4zMjc3NzEgMS44NTMwNTEgNC41Nzg4MjkgMi40Mzg4NTQgNS41OTUwMTkgMi40Mzg4NTRDNi4yNzY0NjMgMi40Mzg4NTQgNi41ODcyOTggMS44MjkxNDEgNi41ODcyOTggMS42NjE3NjhDNi41ODcyOTggMS41NzgwODIgNi41MTU1NjcgMS41NTQxNzIgNi40NTU3OTEgMS41NTQxNzJDNi4zNjAxNDkgMS41NTQxNzIgNi4zNDgxOTQgMS42MDE5OTMgNi4zMTIzMjkgMS42OTc2MzRDNi4xODA4MjIgMi4wMzIzNzkgNS44Njk5ODggMi4xOTk3NTEgNS42Nzg3MDUgMi4xOTk3NTFDNS41MjMyODggMi4xOTk3NTEgNS4zMzIwMDUgMi4xOTk3NTEgNC44MDU5NzggLjg3MjcyN0M0LjQ5NTE0MyAuMDcxNzMxIDQuMjIwMTc0LS44ODQ2ODIgNC4wMTY5MzYtMS42MjU5MDNMNi44NTAzMTEtNC44NTM3OThDNi45NDU5NTMtNC45NjEzOTUgNi45NTc5MDgtNC45NzMzNSA2Ljk1NzkwOC01LjAyMTE3MUM2Ljk1NzkwOC01LjEwNDg1NyA2Ljg5ODEzMi01LjE0MDcyMiA2LjgzODM1Ni01LjE0MDcyMkM2LjgwMjQ5MS01LjE0MDcyMiA2Ljc2NjYyNS01LjE0MDcyMiA2LjY0NzA3My01LjAwOTIxNUwzLjk0NTIwNS0xLjkyNDc4MlonLz4KPHBhdGggaWQ9J2cxLTU5JyBkPSdNMi4zMzEyNTggLjA0NzgyMUMyLjMzMTI1OC0uNjQ1NTc5IDIuMTA0MTEtMS4xNTk2NTEgMS42MTM5NDgtMS4xNTk2NTFDMS4yMzEzODItMS4xNTk2NTEgMS4wNDAxLS44NDg4MTcgMS4wNDAxLS41ODU4MDNTMS4yMTk0MjcgMCAxLjYyNTkwMyAwQzEuNzgxMzIgMCAxLjkxMjgyNy0uMDQ3ODIxIDIuMDIwNDIzLS4xNTU0MTdDMi4wNDQzMzQtLjE3OTMyOCAyLjA1NjI4OS0uMTc5MzI4IDIuMDY4MjQ0LS4xNzkzMjhDMi4wOTIxNTQtLjE3OTMyOCAyLjA5MjE1NC0uMDExOTU1IDIuMDkyMTU0IC4wNDc4MjFDMi4wOTIxNTQgLjQ0MjM0MSAyLjAyMDQyMyAxLjIxOTQyNyAxLjMyNzAyNCAxLjk5NjUxM0MxLjE5NTUxNyAyLjEzOTk3NSAxLjE5NTUxNyAyLjE2Mzg4NSAxLjE5NTUxNyAyLjE4Nzc5NkMxLjE5NTUxNyAyLjI0NzU3MiAxLjI1NTI5MyAyLjMwNzM0NyAxLjMxNTA2OCAyLjMwNzM0N0MxLjQxMDcxIDIuMzA3MzQ3IDIuMzMxMjU4IDEuNDIyNjY1IDIuMzMxMjU4IC4wNDc4MjFaJy8+CjxwYXRoIGlkPSdnMS02NycgZD0nTTguOTMwNTExLTguMzA4ODQyQzguOTMwNTExLTguNDE2NDM4IDguODQ2ODI0LTguNDE2NDM4IDguODIyOTE0LTguNDE2NDM4UzguNzUxMTgzLTguNDE2NDM4IDguNjU1NTQyLTguMjk2ODg3TDcuODMwNjM1LTcuMjkyNjUzQzcuNDEyMjA0LTguMDA5OTYzIDYuNzU0NjctOC40MTY0MzggNS44NTgwMzItOC40MTY0MzhDMy4yNzU3MTYtOC40MTY0MzggLjU5Nzc1OC01Ljc5ODI1NyAuNTk3NzU4LTIuOTg4NzkyQy41OTc3NTgtLjk5MjI3OSAxLjk5NjUxMyAuMjUxMDU5IDMuNzQxOTY4IC4yNTEwNTlDNC42OTgzODEgLjI1MTA1OSA1LjUzNTI0My0uMTU1NDE3IDYuMjI4NjQzLS43NDEyMkM3LjI2ODc0Mi0xLjYxMzk0OCA3LjU3OTU3Ny0yLjc3MzU5OSA3LjU3OTU3Ny0yLjg2OTI0QzcuNTc5NTc3LTIuOTc2ODM3IDcuNDgzOTM1LTIuOTc2ODM3IDcuNDQ4MDctMi45NzY4MzdDNy4zNDA0NzMtMi45NzY4MzcgNy4zMjg1MTgtMi45MDUxMDYgNy4zMDQ2MDgtMi44NTcyODVDNi43NTQ2Ny0uOTkyMjc5IDUuMTQwNzIyLS4wOTU2NDEgMy45NDUyMDUtLjA5NTY0MUMyLjY3Nzk1OC0uMDk1NjQxIDEuNTc4MDgyLS45MDg1OTMgMS41NzgwODItMi42MDYyMjdDMS41NzgwODItMi45ODg3OTIgMS42OTc2MzQtNS4wNjg5OTEgMy4wNDg1NjgtNi42MzUxMThDMy43MDYxMDItNy40MDAyNDkgNC44Mjk4ODgtOC4wNjk3MzggNS45NjU2MjktOC4wNjk3MzhDNy4yODA2OTctOC4wNjk3MzggNy44NjY1MDEtNi45ODE4MTggNy44NjY1MDEtNS43NjIzOTFDNy44NjY1MDEtNS40NTE1NTcgNy44MzA2MzUtNS4xODg1NDMgNy44MzA2MzUtNS4xNDA3MjJDNy44MzA2MzUtNS4wMzMxMjYgNy45NTAxODctNS4wMzMxMjYgNy45ODYwNTItNS4wMzMxMjZDOC4xMTc1NTktNS4wMzMxMjYgOC4xMjk1MTQtNS4wNDUwODEgOC4xNzczMzUtNS4yNjAyNzRMOC45MzA1MTEtOC4zMDg4NDJaJy8+CjxwYXRoIGlkPSdnMS0xMTcnIGQ9J000LjA3NjcxMi0uNjkzNEM0LjIzMjEzLS4wMjM5MSA0LjgwNTk3OCAuMTE5NTUyIDUuMDkyOTAyIC4xMTk1NTJDNS40NzU0NjcgLjExOTU1MiA1Ljc2MjM5MS0uMTMxNTA3IDUuOTUzNjc0LS41Mzc5ODNDNi4xNTY5MTItLjk2ODM2OSA2LjMxMjMyOS0xLjY3MzcyNCA2LjMxMjMyOS0xLjcwOTU4OUM2LjMxMjMyOS0xLjc2OTM2NSA2LjI2NDUwOC0xLjgxNzE4NiA2LjE5Mjc3Ny0xLjgxNzE4NkM2LjA4NTE4MS0xLjgxNzE4NiA2LjA3MzIyNS0xLjc1NzQxIDYuMDI1NDA1LTEuNTc4MDgyQzUuODEwMjEyLS43NTMxNzYgNS41OTUwMTktLjExOTU1MiA1LjExNjgxMi0uMTE5NTUyQzQuNzU4MTU3LS4xMTk1NTIgNC43NTgxNTctLjUxNDA3MiA0Ljc1ODE1Ny0uNjY5NDg5QzQuNzU4MTU3LS45NDQ0NTggNC43OTQwMjItMS4wNjQwMSA0LjkxMzU3NC0xLjU2NjEyN0M0Ljk5NzI2LTEuODg4OTE3IDUuMDgwOTQ2LTIuMjExNzA2IDUuMTUyNjc3LTIuNTQ2NDUxTDUuNjQyODM5LTQuNDk1MTQzQzUuNzI2NTI2LTQuNzk0MDIyIDUuNzI2NTI2LTQuODE3OTMzIDUuNzI2NTI2LTQuODUzNzk4QzUuNzI2NTI2LTUuMDMzMTI2IDUuNTgzMDY0LTUuMTUyNjc3IDUuNDAzNzM2LTUuMTUyNjc3QzUuMDU3MDM2LTUuMTUyNjc3IDQuOTczMzUtNC44NTM3OTggNC45MDE2MTktNC41NTQ5MTlDNC43ODIwNjctNC4wODg2NjcgNC4xMzY0ODgtMS41MTgzMDYgNC4wNTI4MDItMS4wOTk4NzVDNC4wNDA4NDctMS4wOTk4NzUgMy41NzQ1OTUtLjExOTU1MiAyLjcwMTg2OC0uMTE5NTUyQzIuMDgwMTk5LS4xMTk1NTIgMS45NjA2NDgtLjY1NzUzNCAxLjk2MDY0OC0xLjA5OTg3NUMxLjk2MDY0OC0xLjc4MTMyIDIuMjk1MzkyLTIuNzM3NzMzIDIuNjA2MjI3LTMuNTM4NzNDMi43NDk2ODktMy45MjEyOTUgMi44MDk0NjUtNC4wNzY3MTIgMi44MDk0NjUtNC4zMTU4MTZDMi44MDk0NjUtNC44Mjk4ODggMi40Mzg4NTQtNS4yNzIyMjkgMS44NjUwMDYtNS4yNzIyMjlDLjc2NTEzMS01LjI3MjIyOSAuMzIyNzktMy41Mzg3MyAuMzIyNzktMy40NDMwODhDLjMyMjc5LTMuMzk1MjY4IC4zNzA2MS0zLjMzNTQ5MiAuNDU0Mjk2LTMuMzM1NDkyQy41NjE4OTMtMy4zMzU0OTIgLjU3Mzg0OC0zLjM4MzMxMyAuNjIxNjY5LTMuNTUwNjg1Qy45MDg1OTMtNC41Nzg4MjkgMS4zNzQ4NDQtNS4wMzMxMjYgMS44MjkxNDEtNS4wMzMxMjZDMS45NDg2OTItNS4wMzMxMjYgMi4xMzk5NzUtNS4wMjExNzEgMi4xMzk5NzUtNC42Mzg2MDVDMi4xMzk5NzUtNC4zMjc3NzEgMi4wMDg0NjgtMy45ODEwNzEgMS44MjkxNDEtMy41MjY3NzVDMS4zMDMxMTMtMi4xMDQxMSAxLjI0MzMzNy0xLjY0OTgxMyAxLjI0MzMzNy0xLjI5MTE1OEMxLjI0MzMzNy0uMDcxNzMxIDIuMTYzODg1IC4xMTk1NTIgMi42NTQwNDcgLjExOTU1MkMzLjQxOTE3OCAuMTE5NTUyIDMuODM3NjA5LS40MDY0NzYgNC4wNzY3MTItLjY5MzRaJy8+CjwvZGVmcz4KPGcgaWQ9J3BhZ2UxJz4KPHVzZSB4PScxMDguMTAzMjY0JyB5PSctMTAuNTI1MjU4JyB4bGluazpocmVmPScjZzEtMzEnLz4KPHVzZSB4PScxMTUuNDM2ODIxJyB5PSctMTAuNTI1MjU4JyB4bGluazpocmVmPScjZzItNDAnLz4KPHVzZSB4PScxMTkuOTg5MTQ3JyB5PSctMTAuNTI1MjU4JyB4bGluazpocmVmPScjZzEtMTE3Jy8+Cjx1c2UgeD0nMTI2LjY1MTU4NicgeT0nLTEwLjUyNTI1OCcgeGxpbms6aHJlZj0nI2cyLTQxJy8+Cjx1c2UgeD0nMTM0LjUyNDc0MScgeT0nLTEwLjUyNTI1OCcgeGxpbms6aHJlZj0nI2cyLTYxJy8+Cjx1c2UgeD0nMTQ2Ljk1MDIyMicgeT0nLTEwLjUyNTI1OCcgeGxpbms6aHJlZj0nI2cyLTUwJy8+Cjx1c2UgeD0nMTU1LjQ1OTg3NicgeT0nLTEwLjUyNTI1OCcgeGxpbms6aHJlZj0nI2cwLTAnLz4KPHVzZSB4PScxNjguNjEwNTUnIHk9Jy0xOC42MTMwMTcnIHhsaW5rOmhyZWY9JyNnMi0xMDgnLz4KPHVzZSB4PScxNzEuODYyMjEyJyB5PSctMTguNjEzMDE3JyB4bGluazpocmVmPScjZzItMTExJy8+Cjx1c2UgeD0nMTc3LjcxNTIwMicgeT0nLTE4LjYxMzAxNycgeGxpbms6aHJlZj0nI2cyLTEwMycvPgo8dXNlIHg9JzE4NS43MjMyNzMnIHk9Jy0xOC42MTMwMTcnIHhsaW5rOmhyZWY9JyNnMS02NycvPgo8dXNlIHg9JzE5NC45NTY4ODUnIHk9Jy0xOC42MTMwMTcnIHhsaW5rOmhyZWY9JyNnMi00MCcvPgo8dXNlIHg9JzE5OS41MDkyMScgeT0nLTE4LjYxMzAxNycgeGxpbms6aHJlZj0nI2cxLTExNycvPgo8dXNlIHg9JzIwNi4xNzE2NScgeT0nLTE4LjYxMzAxNycgeGxpbms6aHJlZj0nI2cxLTU5Jy8+Cjx1c2UgeD0nMjExLjQxNTgwOScgeT0nLTE4LjYxMzAxNycgeGxpbms6aHJlZj0nI2cxLTExNycvPgo8dXNlIHg9JzIxOC4wNzgyNDgnIHk9Jy0xOC42MTMwMTcnIHhsaW5rOmhyZWY9JyNnMi00MScvPgo8cmVjdCB4PScxNjguNjEwNTUnIHk9Jy0xMy43NTMxNDQnIGhlaWdodD0nLjQ3ODE4Nycgd2lkdGg9JzU0LjAyMDAyJy8+Cjx1c2UgeD0nMTgzLjczMjk3OScgeT0nLTIuMzI0NTk2JyB4bGluazpocmVmPScjZzItMTA4Jy8+Cjx1c2UgeD0nMTg2Ljk4NDY0MScgeT0nLTIuMzI0NTk2JyB4bGluazpocmVmPScjZzItMTExJy8+Cjx1c2UgeD0nMTkyLjgzNzYzMScgeT0nLTIuMzI0NTk2JyB4bGluazpocmVmPScjZzItMTAzJy8+Cjx1c2UgeD0nMjAwLjg0NTcwMicgeT0nLTIuMzI0NTk2JyB4bGluazpocmVmPScjZzEtMTE3Jy8+Cjx1c2UgeD0nMjIzLjgyNjA4NCcgeT0nLTEwLjUyNTI1OCcgeGxpbms6aHJlZj0nI2cxLTU5Jy8+Cjx1c2UgeD0nMjI5LjA3MDI0MycgeT0nLTEwLjUyNTI1OCcgeGxpbms6aHJlZj0nI2cwLTU2Jy8+Cjx1c2UgeD0nMjM1LjcxMjAyMycgeT0nLTEwLjUyNTI1OCcgeGxpbms6aHJlZj0nI2cxLTExNycvPgo8dXNlIHg9JzI0NS42OTUyOTInIHk9Jy0xMC41MjUyNTgnIHhsaW5rOmhyZWY9JyNnMC01MCcvPgo8dXNlIHg9JzI1Ni45ODYyNicgeT0nLTEwLjUyNTI1OCcgeGxpbms6aHJlZj0nI2cyLTkxJy8+Cjx1c2UgeD0nMjYwLjIzNzkyMicgeT0nLTEwLjUyNTI1OCcgeGxpbms6aHJlZj0nI2cyLTQ4Jy8+Cjx1c2UgeD0nMjY2LjA5MDkxMicgeT0nLTEwLjUyNTI1OCcgeGxpbms6aHJlZj0nI2cxLTU5Jy8+Cjx1c2UgeD0nMjcxLjMzNTA3MScgeT0nLTEwLjUyNTI1OCcgeGxpbms6aHJlZj0nI2cyLTQ5Jy8+Cjx1c2UgeD0nMjc3LjE4ODA2MScgeT0nLTEwLjUyNTI1OCcgeGxpbms6aHJlZj0nI2cyLTkzJy8+CjwvZz4KPC9zdmc+CjwhLS0gREVQVEg9MCAtLT4=)

We can see the tail dependence coefficient as the limit of the function when  tends

to

tends

to  . As a matter of fact, when is close to , we have:

. As a matter of fact, when is close to , we have:

![\chi(u) = 2 - \frac{1-C(u,u)}{1-u} + o(1) = \Pset[F_2(X_2) > u | F1(X_1) > u] + o(1)](data:image/svg+xml;base64,PD94bWwgdmVyc2lvbj0nMS4wJyBlbmNvZGluZz0nVVRGLTgnPz4KPCEtLSBUaGlzIGZpbGUgd2FzIGdlbmVyYXRlZCBieSBkdmlzdmdtIDMuMyAtLT4KPHN2ZyB2ZXJzaW9uPScxLjEnIHhtbG5zPSdodHRwOi8vd3d3LnczLm9yZy8yMDAwL3N2ZycgeG1sbnM6eGxpbms9J2h0dHA6Ly93d3cudzMub3JnLzE5OTkveGxpbmsnIHdpZHRoPSczNDEuMjQ2MDg4cHQnIGhlaWdodD0nMjYuMjUxMDY5cHQnIHZpZXdCb3g9JzIzLjY0ODQ3IC0yNi4yNTEwNjEgMzQxLjI0NjA4OCAyNi4yNTEwNjknPgo8ZGVmcz4KPHBhdGggaWQ9J2czLTQ5JyBkPSdNMi41MDI2MTUtNS4wNzY5NjFDMi41MDI2MTUtNS4yOTIxNTQgMi40ODY2NzUtNS4zMDAxMjUgMi4yNzE0ODItNS4zMDAxMjVDMS45NDQ3MDctNC45ODEzMiAxLjUyMjI5MS00Ljc5MDAzNyAuNzY1MTMxLTQuNzkwMDM3Vi00LjUyNzAyNEMuOTgwMzI0LTQuNTI3MDI0IDEuNDEwNzEtNC41MjcwMjQgMS44NzI5NzYtNC43NDIyMTdWLS42NTM1NDlDMS44NzI5NzYtLjM1ODY1NSAxLjg0OTA2Ni0uMjYzMDE0IDEuMDkxOTA1LS4yNjMwMTRILjgxMjk1MVYwQzEuMTM5NzI2LS4wMjM5MSAxLjgyNTE1Ni0uMDIzOTEgMi4xODM4MTEtLjAyMzkxUzMuMjM1ODY2LS4wMjM5MSAzLjU2MjY0IDBWLS4yNjMwMTRIMy4yODM2ODZDMi41MjY1MjYtLjI2MzAxNCAyLjUwMjYxNS0uMzU4NjU1IDIuNTAyNjE1LS42NTM1NDlWLTUuMDc2OTYxWicvPgo8cGF0aCBpZD0nZzMtNTAnIGQ9J00yLjI0NzU3Mi0xLjYyNTkwM0MyLjM3NTA5My0xLjc0NTQ1NSAyLjcwOTgzOC0yLjAwODQ2OCAyLjgzNzM2LTIuMTIwMDVDMy4zMzE1MDctMi41NzQzNDYgMy44MDE3NDMtMy4wMTI3MDIgMy44MDE3NDMtMy43Mzc5ODNDMy44MDE3NDMtNC42ODY0MjYgMy4wMDQ3MzItNS4zMDAxMjUgMi4wMDg0NjgtNS4zMDAxMjVDMS4wNTIwNTUtNS4zMDAxMjUgLjQyMjQxNi00LjU3NDg0NCAuNDIyNDE2LTMuODY1NTA0Qy40MjI0MTYtMy40NzQ5NjkgLjczMzI1LTMuNDE5MTc4IC44NDQ4MzItMy40MTkxNzhDMS4wMTIyMDQtMy40MTkxNzggMS4yNTkyNzgtMy41Mzg3MyAxLjI1OTI3OC0zLjg0MTU5NEMxLjI1OTI3OC00LjI1NjA0IC44NjA3NzItNC4yNTYwNCAuNzY1MTMxLTQuMjU2MDRDLjk5NjI2NC00LjgzNzg1OCAxLjUzMDI2Mi01LjAzNzExMSAxLjkyMDc5Ny01LjAzNzExMUMyLjY2MjAxNy01LjAzNzExMSAzLjA0NDU4My00LjQwNzQ3MiAzLjA0NDU4My0zLjczNzk4M0MzLjA0NDU4My0yLjkwOTA5MSAyLjQ2Mjc2NS0yLjMwMzM2MiAxLjUyMjI5MS0xLjMzODk3OUwuNTE4MDU3LS4zMDI4NjRDLjQyMjQxNi0uMjE1MTkzIC40MjI0MTYtLjE5OTI1MyAuNDIyNDE2IDBIMy41NzA2MUwzLjgwMTc0My0xLjQyNjY1SDMuNTU0NjdDMy41MzA3Ni0xLjI2NzI0OCAzLjQ2Njk5OS0uODY4NzQyIDMuMzcxMzU3LS43MTczMUMzLjMyMzUzNy0uNjUzNTQ5IDIuNzE3ODA4LS42NTM1NDkgMi41OTAyODYtLjY1MzU0OUgxLjE3MTYwNkwyLjI0NzU3Mi0xLjYyNTkwM1onLz4KPHBhdGggaWQ9J2cwLTgwJyBkPSdNMy4xMzIyNTQtMy42ODIxOTJDMy4xODAwNzUtMy42ODIxOTIgMy40MzExMzMtMy42ODIxOTIgMy40NTUwNDQtMy42NzAyMzdIMy44NjE1MTlDNi4yODg0MTgtMy42NzAyMzcgNy4xNjExNDYtNC44MDU5NzggNy4xNjExNDYtNS45NDE3MTlDNy4xNjExNDYtNy42MzkzNTIgNS42MzA4ODQtOC4xODkyOSA0LjA4ODY2Ny04LjE4OTI5SC41OTc3NThDLjM4MjU2NS04LjE4OTI5IC4xOTEyODMtOC4xODkyOSAuMTkxMjgzLTcuOTc0MDk3Qy4xOTEyODMtNy43NzA4NTkgLjQxODQzMS03Ljc3MDg1OSAuNTE0MDcyLTcuNzcwODU5QzEuMTM1NzQxLTcuNzcwODU5IDEuMTgzNTYyLTcuNjc1MjE4IDEuMTgzNTYyLTcuMDg5NDE1Vi0xLjA5OTg3NUMxLjE4MzU2Mi0uNTE0MDcyIDEuMTM1NzQxLS40MTg0MzEgLjUyNjAyNy0uNDE4NDMxQy40MDY0NzYtLjQxODQzMSAuMTkxMjgzLS40MTg0MzEgLjE5MTI4My0uMjE1MTkzQy4xOTEyODMgMCAuMzgyNTY1IDAgLjU5Nzc1OCAwSDMuODAxNzQzQzQuMDE2OTM2IDAgNC4xOTYyNjQgMCA0LjE5NjI2NC0uMjE1MTkzQzQuMTk2MjY0LS40MTg0MzEgMy45OTMwMjYtLjQxODQzMSAzLjg2MTUxOS0uNDE4NDMxQzMuMTgwMDc1LS40MTg0MzEgMy4xMzIyNTQtLjUxNDA3MiAzLjEzMjI1NC0xLjA5OTg3NVYtMy42ODIxOTJaTTUuMTA0ODU3LTQuMjIwMTc0QzUuNDg3NDIyLTQuNzIyMjkxIDUuNTIzMjg4LTUuNDc1NDY3IDUuNTIzMjg4LTUuOTUzNjc0QzUuNTIzMjg4LTYuNTg3Mjk4IDUuNDYzNTEyLTcuMjIwOTIyIDUuMTUyNjc3LTcuNjYzMjYzQzUuODEwMjEyLTcuNTA3ODQ2IDYuNzQyNzE1LTcuMTQ5MTkxIDYuNzQyNzE1LTUuOTQxNzE5QzYuNzQyNzE1LTUuMTA0ODU3IDYuMjA0NzMyLTQuNDk1MTQzIDUuMTA0ODU3LTQuMjIwMTc0Wk0zLjEzMjI1NC03LjEyNTI4QzMuMTMyMjU0LTcuMzY0Mzg0IDMuMTMyMjU0LTcuNzcwODU5IDMuODQ5NTY0LTcuNzcwODU5QzQuNzEwMzM2LTcuNzcwODU5IDUuMTA0ODU3LTcuNDQ4MDcgNS4xMDQ4NTctNS45NTM2NzRDNS4xMDQ4NTctNC4yNDQwODUgNC40NzEyMzMtNC4xMDA2MjMgMy43MzAwMTItNC4xMDA2MjNIMy4xMzIyNTRWLTcuMTI1MjhaTTEuNTA2MzUxLS40MTg0MzFDMS42MDE5OTMtLjYzMzYyNCAxLjYwMTk5My0uOTIwNTQ4IDEuNjAxOTkzLTEuMDc1OTY1Vi03LjExMzMyNUMxLjYwMTk5My03LjI2ODc0MiAxLjYwMTk5My03LjU1NTY2NiAxLjUwNjM1MS03Ljc3MDg1OUgyLjg2OTI0QzIuNzEzODIzLTcuNTc5NTc3IDIuNzEzODIzLTcuMzQwNDczIDIuNzEzODIzLTcuMTYxMTQ2Vi0xLjA3NTk2NUMyLjcxMzgyMy0uOTU2NDEzIDIuNzEzODIzLS42MzM2MjQgMi44MDk0NjUtLjQxODQzMUgxLjUwNjM1MVonLz4KPHBhdGggaWQ9J2cxLTAnIGQ9J003Ljg3ODQ1Ni0yLjc0OTY4OUM4LjA4MTY5NC0yLjc0OTY4OSA4LjI5Njg4Ny0yLjc0OTY4OSA4LjI5Njg4Ny0yLjk4ODc5MlM4LjA4MTY5NC0zLjIyNzg5NSA3Ljg3ODQ1Ni0zLjIyNzg5NUgxLjQxMDcxQzEuMjA3NDcyLTMuMjI3ODk1IC45OTIyNzktMy4yMjc4OTUgLjk5MjI3OS0yLjk4ODc5MlMxLjIwNzQ3Mi0yLjc0OTY4OSAxLjQxMDcxLTIuNzQ5Njg5SDcuODc4NDU2WicvPgo8cGF0aCBpZD0nZzEtMTA2JyBkPSdNMS45MDA4NzItOC41MzU5OUMxLjkwMDg3Mi04Ljc1MTE4MyAxLjkwMDg3Mi04Ljk2NjM3NiAxLjY2MTc2OC04Ljk2NjM3NlMxLjQyMjY2NS04Ljc1MTE4MyAxLjQyMjY2NS04LjUzNTk5VjIuNTU4NDA2QzEuNDIyNjY1IDIuNzczNTk5IDEuNDIyNjY1IDIuOTg4NzkyIDEuNjYxNzY4IDIuOTg4NzkyUzEuOTAwODcyIDIuNzczNTk5IDEuOTAwODcyIDIuNTU4NDA2Vi04LjUzNTk5WicvPgo8cGF0aCBpZD0nZzQtNDAnIGQ9J00zLjg4NTQzIDIuOTA1MTA2QzMuODg1NDMgMi44NjkyNCAzLjg4NTQzIDIuODQ1MzMgMy42ODIxOTIgMi42NDIwOTJDMi40ODY2NzUgMS40MzQ2MiAxLjgxNzE4Ni0uNTM3OTgzIDEuODE3MTg2LTIuOTc2ODM3QzEuODE3MTg2LTUuMjk2MTM5IDIuMzc5MDc4LTcuMjkyNjUzIDMuNzY1ODc4LTguNzAzMzYyQzMuODg1NDMtOC44MTA5NTkgMy44ODU0My04LjgzNDg2OSAzLjg4NTQzLTguODcwNzM1QzMuODg1NDMtOC45NDI0NjYgMy44MjU2NTQtOC45NjYzNzYgMy43Nzc4MzMtOC45NjYzNzZDMy42MjI0MTYtOC45NjYzNzYgMi42NDIwOTItOC4xMDU2MDQgMi4wNTYyODktNi45MzM5OThDMS40NDY1NzUtNS43MjY1MjYgMS4xNzE2MDYtNC40NDczMjMgMS4xNzE2MDYtMi45NzY4MzdDMS4xNzE2MDYtMS45MTI4MjcgMS4zMzg5NzktLjQ5MDE2MiAxLjk2MDY0OCAuNzg5MDQxQzIuNjY2MDAyIDIuMjIzNjYxIDMuNjQ2MzI2IDMuMDAwNzQ3IDMuNzc3ODMzIDMuMDAwNzQ3QzMuODI1NjU0IDMuMDAwNzQ3IDMuODg1NDMgMi45NzY4MzcgMy44ODU0MyAyLjkwNTEwNlonLz4KPHBhdGggaWQ9J2c0LTQxJyBkPSdNMy4zNzEzNTctMi45NzY4MzdDMy4zNzEzNTctMy44ODU0MyAzLjI1MTgwNi01LjM2Nzg3IDIuNTgyMzE2LTYuNzU0NjdDMS44NzY5NjEtOC4xODkyOSAuODk2NjM4LTguOTY2Mzc2IC43NjUxMzEtOC45NjYzNzZDLjcxNzMxLTguOTY2Mzc2IC42NTc1MzQtOC45NDI0NjYgLjY1NzUzNC04Ljg3MDczNUMuNjU3NTM0LTguODM0ODY5IC42NTc1MzQtOC44MTA5NTkgLjg2MDc3Mi04LjYwNzcyMUMyLjA1NjI4OS03LjQwMDI0OSAyLjcyNTc3OC01LjQyNzY0NiAyLjcyNTc3OC0yLjk4ODc5MkMyLjcyNTc3OC0uNjY5NDg5IDIuMTYzODg1IDEuMzI3MDI0IC43NzcwODYgMi43Mzc3MzNDLjY1NzUzNCAyLjg0NTMzIC42NTc1MzQgMi44NjkyNCAuNjU3NTM0IDIuOTA1MTA2Qy42NTc1MzQgMi45NzY4MzcgLjcxNzMxIDMuMDAwNzQ3IC43NjUxMzEgMy4wMDA3NDdDLjkyMDU0OCAzLjAwMDc0NyAxLjkwMDg3MiAyLjEzOTk3NSAyLjQ4NjY3NSAuOTY4MzY5QzMuMDk2Mzg5LS4yNTEwNTkgMy4zNzEzNTctMS41NDIyMTcgMy4zNzEzNTctMi45NzY4MzdaJy8+CjxwYXRoIGlkPSdnNC00MycgZD0nTTQuNzcwMTEyLTIuNzYxNjQ0SDguMDY5NzM4QzguMjM3MTExLTIuNzYxNjQ0IDguNDUyMzA0LTIuNzYxNjQ0IDguNDUyMzA0LTIuOTc2ODM3QzguNDUyMzA0LTMuMjAzOTg1IDguMjQ5MDY2LTMuMjAzOTg1IDguMDY5NzM4LTMuMjAzOTg1SDQuNzcwMTEyVi02LjUwMzYxMUM0Ljc3MDExMi02LjY3MDk4NCA0Ljc3MDExMi02Ljg4NjE3NyA0LjU1NDkxOS02Ljg4NjE3N0M0LjMyNzc3MS02Ljg4NjE3NyA0LjMyNzc3MS02LjY4MjkzOSA0LjMyNzc3MS02LjUwMzYxMVYtMy4yMDM5ODVIMS4wMjgxNDRDLjg2MDc3Mi0zLjIwMzk4NSAuNjQ1NTc5LTMuMjAzOTg1IC42NDU1NzktMi45ODg3OTJDLjY0NTU3OS0yLjc2MTY0NCAuODQ4ODE3LTIuNzYxNjQ0IDEuMDI4MTQ0LTIuNzYxNjQ0SDQuMzI3NzcxVi41Mzc5ODNDNC4zMjc3NzEgLjcwNTM1NSA0LjMyNzc3MSAuOTIwNTQ4IDQuNTQyOTY0IC45MjA1NDhDNC43NzAxMTIgLjkyMDU0OCA0Ljc3MDExMiAuNzE3MzEgNC43NzAxMTIgLjUzNzk4M1YtMi43NjE2NDRaJy8+CjxwYXRoIGlkPSdnNC00OScgZD0nTTMuNDQzMDg4LTcuNjYzMjYzQzMuNDQzMDg4LTcuOTM4MjMyIDMuNDQzMDg4LTcuOTUwMTg3IDMuMjAzOTg1LTcuOTUwMTg3QzIuOTE3MDYxLTcuNjI3Mzk3IDIuMzE5MzAzLTcuMTg1MDU2IDEuMDg3OTItNy4xODUwNTZWLTYuODM4MzU2QzEuMzYyODg5LTYuODM4MzU2IDEuOTYwNjQ4LTYuODM4MzU2IDIuNjE4MTgyLTcuMTQ5MTkxVi0uOTIwNTQ4QzIuNjE4MTgyLS40OTAxNjIgMi41ODIzMTYtLjM0NjcgMS41MzAyNjItLjM0NjdIMS4xNTk2NTFWMEMxLjQ4MjQ0MS0uMDIzOTEgMi42NDIwOTItLjAyMzkxIDMuMDM2NjEzLS4wMjM5MVM0LjU3ODgyOS0uMDIzOTEgNC45MDE2MTkgMFYtLjM0NjdINC41MzEwMDlDMy40Nzg5NTQtLjM0NjcgMy40NDMwODgtLjQ5MDE2MiAzLjQ0MzA4OC0uOTIwNTQ4Vi03LjY2MzI2M1onLz4KPHBhdGggaWQ9J2c0LTUwJyBkPSdNNS4yNjAyNzQtMi4wMDg0NjhINC45OTcyNkM0Ljk2MTM5NS0xLjgwNTIzIDQuODY1NzUzLTEuMTQ3Njk2IDQuNzQ2MjAyLS45NTY0MTNDNC42NjI1MTYtLjg0ODgxNyAzLjk4MTA3MS0uODQ4ODE3IDMuNjIyNDE2LS44NDg4MTdIMS40MTA3MUMxLjczMzQ5OS0xLjEyMzc4NiAyLjQ2Mjc2NS0xLjg4ODkxNyAyLjc3MzU5OS0yLjE3NTg0MUM0LjU5MDc4NS0zLjg0OTU2NCA1LjI2MDI3NC00LjQ3MTIzMyA1LjI2MDI3NC01LjY1NDc5NUM1LjI2MDI3NC03LjAyOTYzOSA0LjE3MjM1NC03Ljk1MDE4NyAyLjc4NTU1NC03Ljk1MDE4N1MuNTg1ODAzLTYuNzY2NjI1IC41ODU4MDMtNS43Mzg0ODFDLjU4NTgwMy01LjEyODc2NyAxLjExMTgzMS01LjEyODc2NyAxLjE0NzY5Ni01LjEyODc2N0MxLjM5ODc1NS01LjEyODc2NyAxLjcwOTU4OS01LjMwODA5NSAxLjcwOTU4OS01LjY5MDY2QzEuNzA5NTg5LTYuMDI1NDA1IDEuNDgyNDQxLTYuMjUyNTUzIDEuMTQ3Njk2LTYuMjUyNTUzQzEuMDQwMS02LjI1MjU1MyAxLjAxNjE4OS02LjI1MjU1MyAuOTgwMzI0LTYuMjQwNTk4QzEuMjA3NDcyLTcuMDUzNTQ5IDEuODUzMDUxLTcuNjAzNDg3IDIuNjMwMTM3LTcuNjAzNDg3QzMuNjQ2MzI2LTcuNjAzNDg3IDQuMjY3OTk1LTYuNzU0NjcgNC4yNjc5OTUtNS42NTQ3OTVDNC4yNjc5OTUtNC42Mzg2MDUgMy42ODIxOTItMy43NTM5MjMgMy4wMDA3NDctMi45ODg3OTJMLjU4NTgwMy0uMjg2OTI0VjBINC45NDk0NEw1LjI2MDI3NC0yLjAwODQ2OFonLz4KPHBhdGggaWQ9J2c0LTYxJyBkPSdNOC4wNjk3MzgtMy44NzM0NzRDOC4yMzcxMTEtMy44NzM0NzQgOC40NTIzMDQtMy44NzM0NzQgOC40NTIzMDQtNC4wODg2NjdDOC40NTIzMDQtNC4zMTU4MTYgOC4yNDkwNjYtNC4zMTU4MTYgOC4wNjk3MzgtNC4zMTU4MTZIMS4wMjgxNDRDLjg2MDc3Mi00LjMxNTgxNiAuNjQ1NTc5LTQuMzE1ODE2IC42NDU1NzktNC4xMDA2MjNDLjY0NTU3OS0zLjg3MzQ3NCAuODQ4ODE3LTMuODczNDc0IDEuMDI4MTQ0LTMuODczNDc0SDguMDY5NzM4Wk04LjA2OTczOC0xLjY0OTgxM0M4LjIzNzExMS0xLjY0OTgxMyA4LjQ1MjMwNC0xLjY0OTgxMyA4LjQ1MjMwNC0xLjg2NTAwNkM4LjQ1MjMwNC0yLjA5MjE1NCA4LjI0OTA2Ni0yLjA5MjE1NCA4LjA2OTczOC0yLjA5MjE1NEgxLjAyODE0NEMuODYwNzcyLTIuMDkyMTU0IC42NDU1NzktMi4wOTIxNTQgLjY0NTU3OS0xLjg3Njk2MUMuNjQ1NTc5LTEuNjQ5ODEzIC44NDg4MTctMS42NDk4MTMgMS4wMjgxNDQtMS42NDk4MTNIOC4wNjk3MzhaJy8+CjxwYXRoIGlkPSdnNC05MScgZD0nTTIuOTg4NzkyIDIuOTg4NzkyVjIuNTQ2NDUxSDEuODI5MTQxVi04LjUyNDAzNUgyLjk4ODc5MlYtOC45NjYzNzZIMS4zODY4VjIuOTg4NzkySDIuOTg4NzkyWicvPgo8cGF0aCBpZD0nZzQtOTMnIGQ9J00xLjg1MzA1MS04Ljk2NjM3NkguMjUxMDU5Vi04LjUyNDAzNUgxLjQxMDcxVjIuNTQ2NDUxSC4yNTEwNTlWMi45ODg3OTJIMS44NTMwNTFWLTguOTY2Mzc2WicvPgo8cGF0aCBpZD0nZzItMzEnIGQ9J00zLjk0NTIwNS0xLjkyNDc4MkMzLjYyMjQxNi0yLjkxNzA2MSAzLjY5NDE0Ny0yLjgyMTQyIDMuMzk1MjY4LTMuNjU4MjgxQzMuMDI0NjU4LTQuNjg2NDI2IDIuOTI5MDE2LTQuNzcwMTEyIDIuNzYxNjQ0LTQuOTM3NDg0QzIuNTQ2NDUxLTUuMTI4NzY3IDIuMTM5OTc1LTUuMjcyMjI5IDEuNzIxNTQ0LTUuMjcyMjI5QzEuMDUyMDU1LTUuMjcyMjI5IC43MjkyNjUtNC42NTA1NiAuNzI5MjY1LTQuNDk1MTQzQy43MjkyNjUtNC40MjM0MTIgLjc4OTA0MS00LjM4NzU0NyAuODYwNzcyLTQuMzg3NTQ3Qy45NTY0MTMtNC4zODc1NDcgLjk4MDMyNC00LjQ0NzMyMyAuOTkyMjc5LTQuNDk1MTQzQzEuMTcxNjA2LTQuOTYxMzk1IDEuNTQyMjE3LTUuMDMzMTI2IDEuNjQ5ODEzLTUuMDMzMTI2QzEuOTk2NTEzLTUuMDMzMTI2IDIuMzMxMjU4LTQuMTcyMzU0IDIuNTQ2NDUxLTMuNTk4NTA2QzIuODMzMzc1LTIuODY5MjQgMi45NzY4MzctMi4zNjcxMjMgMy4yOTk2MjYtMS4yMDc0NzJMLjQ3ODIwNyAxLjk5NjUxM0MuMzcwNjEgMi4xMjgwMiAuMzcwNjEgMi4xNzU4NDEgLjM3MDYxIDIuMTg3Nzk2Qy4zNzA2MSAyLjI4MzQzNyAuNDMwMzg2IDIuMzA3MzQ3IC40NzgyMDcgMi4zMDczNDdTLjU2MTg5MyAyLjI4MzQzNyAuNTk3NzU4IDIuMjQ3NTcyQy45MzI1MDMgMS45MTI4MjcgMS42NzM3MjQgMS4wMjgxNDQgMS45ODQ1NTggLjY2OTQ4OUwzLjM3MTM1Ny0uOTA4NTkzQzMuOTU3MTYxIC45MzI1MDMgMy45NTcxNjEgLjk1NjQxMyA0LjEzNjQ4OCAxLjM5ODc1NUM0LjMyNzc3MSAxLjg1MzA1MSA0LjU3ODgyOSAyLjQzODg1NCA1LjU5NTAxOSAyLjQzODg1NEM2LjI3NjQ2MyAyLjQzODg1NCA2LjU4NzI5OCAxLjgyOTE0MSA2LjU4NzI5OCAxLjY2MTc2OEM2LjU4NzI5OCAxLjU3ODA4MiA2LjUxNTU2NyAxLjU1NDE3MiA2LjQ1NTc5MSAxLjU1NDE3MkM2LjM2MDE0OSAxLjU1NDE3MiA2LjM0ODE5NCAxLjYwMTk5MyA2LjMxMjMyOSAxLjY5NzYzNEM2LjE4MDgyMiAyLjAzMjM3OSA1Ljg2OTk4OCAyLjE5OTc1MSA1LjY3ODcwNSAyLjE5OTc1MUM1LjUyMzI4OCAyLjE5OTc1MSA1LjMzMjAwNSAyLjE5OTc1MSA0LjgwNTk3OCAuODcyNzI3QzQuNDk1MTQzIC4wNzE3MzEgNC4yMjAxNzQtLjg4NDY4MiA0LjAxNjkzNi0xLjYyNTkwM0w2Ljg1MDMxMS00Ljg1Mzc5OEM2Ljk0NTk1My00Ljk2MTM5NSA2Ljk1NzkwOC00Ljk3MzM1IDYuOTU3OTA4LTUuMDIxMTcxQzYuOTU3OTA4LTUuMTA0ODU3IDYuODk4MTMyLTUuMTQwNzIyIDYuODM4MzU2LTUuMTQwNzIyQzYuODAyNDkxLTUuMTQwNzIyIDYuNzY2NjI1LTUuMTQwNzIyIDYuNjQ3MDczLTUuMDA5MjE1TDMuOTQ1MjA1LTEuOTI0NzgyWicvPgo8cGF0aCBpZD0nZzItNTknIGQ9J00yLjMzMTI1OCAuMDQ3ODIxQzIuMzMxMjU4LS42NDU1NzkgMi4xMDQxMS0xLjE1OTY1MSAxLjYxMzk0OC0xLjE1OTY1MUMxLjIzMTM4Mi0xLjE1OTY1MSAxLjA0MDEtLjg0ODgxNyAxLjA0MDEtLjU4NTgwM1MxLjIxOTQyNyAwIDEuNjI1OTAzIDBDMS43ODEzMiAwIDEuOTEyODI3LS4wNDc4MjEgMi4wMjA0MjMtLjE1NTQxN0MyLjA0NDMzNC0uMTc5MzI4IDIuMDU2Mjg5LS4xNzkzMjggMi4wNjgyNDQtLjE3OTMyOEMyLjA5MjE1NC0uMTc5MzI4IDIuMDkyMTU0LS4wMTE5NTUgMi4wOTIxNTQgLjA0NzgyMUMyLjA5MjE1NCAuNDQyMzQxIDIuMDIwNDIzIDEuMjE5NDI3IDEuMzI3MDI0IDEuOTk2NTEzQzEuMTk1NTE3IDIuMTM5OTc1IDEuMTk1NTE3IDIuMTYzODg1IDEuMTk1NTE3IDIuMTg3Nzk2QzEuMTk1NTE3IDIuMjQ3NTcyIDEuMjU1MjkzIDIuMzA3MzQ3IDEuMzE1MDY4IDIuMzA3MzQ3QzEuNDEwNzEgMi4zMDczNDcgMi4zMzEyNTggMS40MjI2NjUgMi4zMzEyNTggLjA0NzgyMVonLz4KPHBhdGggaWQ9J2cyLTYyJyBkPSdNNy44Nzg0NTYtMi43MjU3NzhDOC4xMDU2MDQtMi44MzMzNzUgOC4xMTc1NTktMi45MDUxMDYgOC4xMTc1NTktMi45ODg3OTJDOC4xMTc1NTktMy4wNjA1MjMgOC4wOTM2NDktMy4xNDQyMDkgNy44Nzg0NTYtMy4yMzk4NTFMMS40MTA3MS02LjIxNjY4N0MxLjI1NTI5My02LjI4ODQxOCAxLjIzMTM4Mi02LjMwMDM3NCAxLjIwNzQ3Mi02LjMwMDM3NEMxLjA2NDAxLTYuMzAwMzc0IC45ODAzMjQtNi4xODA4MjIgLjk4MDMyNC02LjA4NTE4MUMuOTgwMzI0LTUuOTQxNzE5IDEuMDc1OTY1LTUuODkzODk4IDEuMjMxMzgyLTUuODIyMTY3TDcuMzc2MzM5LTIuOTg4NzkyTDEuMjE5NDI3LS4xNDM0NjJDLjk4MDMyNC0uMDM1ODY2IC45ODAzMjQgLjA0NzgyMSAuOTgwMzI0IC4xMTk1NTJDLjk4MDMyNCAuMjE1MTkzIDEuMDY0MDEgLjMzNDc0NSAxLjIwNzQ3MiAuMzM0NzQ1QzEuMjMxMzgyIC4zMzQ3NDUgMS4yNDMzMzcgLjMyMjc5IDEuNDEwNzEgLjI1MTA1OUw3Ljg3ODQ1Ni0yLjcyNTc3OFonLz4KPHBhdGggaWQ9J2cyLTY3JyBkPSdNOC45MzA1MTEtOC4zMDg4NDJDOC45MzA1MTEtOC40MTY0MzggOC44NDY4MjQtOC40MTY0MzggOC44MjI5MTQtOC40MTY0MzhTOC43NTExODMtOC40MTY0MzggOC42NTU1NDItOC4yOTY4ODdMNy44MzA2MzUtNy4yOTI2NTNDNy40MTIyMDQtOC4wMDk5NjMgNi43NTQ2Ny04LjQxNjQzOCA1Ljg1ODAzMi04LjQxNjQzOEMzLjI3NTcxNi04LjQxNjQzOCAuNTk3NzU4LTUuNzk4MjU3IC41OTc3NTgtMi45ODg3OTJDLjU5Nzc1OC0uOTkyMjc5IDEuOTk2NTEzIC4yNTEwNTkgMy43NDE5NjggLjI1MTA1OUM0LjY5ODM4MSAuMjUxMDU5IDUuNTM1MjQzLS4xNTU0MTcgNi4yMjg2NDMtLjc0MTIyQzcuMjY4NzQyLTEuNjEzOTQ4IDcuNTc5NTc3LTIuNzczNTk5IDcuNTc5NTc3LTIuODY5MjRDNy41Nzk1NzctMi45NzY4MzcgNy40ODM5MzUtMi45NzY4MzcgNy40NDgwNy0yLjk3NjgzN0M3LjM0MDQ3My0yLjk3NjgzNyA3LjMyODUxOC0yLjkwNTEwNiA3LjMwNDYwOC0yLjg1NzI4NUM2Ljc1NDY3LS45OTIyNzkgNS4xNDA3MjItLjA5NTY0MSAzLjk0NTIwNS0uMDk1NjQxQzIuNjc3OTU4LS4wOTU2NDEgMS41NzgwODItLjkwODU5MyAxLjU3ODA4Mi0yLjYwNjIyN0MxLjU3ODA4Mi0yLjk4ODc5MiAxLjY5NzYzNC01LjA2ODk5MSAzLjA0ODU2OC02LjYzNTExOEMzLjcwNjEwMi03LjQwMDI0OSA0LjgyOTg4OC04LjA2OTczOCA1Ljk2NTYyOS04LjA2OTczOEM3LjI4MDY5Ny04LjA2OTczOCA3Ljg2NjUwMS02Ljk4MTgxOCA3Ljg2NjUwMS01Ljc2MjM5MUM3Ljg2NjUwMS01LjQ1MTU1NyA3LjgzMDYzNS01LjE4ODU0MyA3LjgzMDYzNS01LjE0MDcyMkM3LjgzMDYzNS01LjAzMzEyNiA3Ljk1MDE4Ny01LjAzMzEyNiA3Ljk4NjA1Mi01LjAzMzEyNkM4LjExNzU1OS01LjAzMzEyNiA4LjEyOTUxNC01LjA0NTA4MSA4LjE3NzMzNS01LjI2MDI3NEw4LjkzMDUxMS04LjMwODg0MlonLz4KPHBhdGggaWQ9J2cyLTcwJyBkPSdNMy41NTA2ODUtMy44OTczODVINC42OTgzODFDNS42MDY5NzQtMy44OTczODUgNS42Nzg3MDUtMy42OTQxNDcgNS42Nzg3MDUtMy4zNDc0NDdDNS42Nzg3MDUtMy4xOTIwMyA1LjY1NDc5NS0zLjAyNDY1OCA1LjU5NTAxOS0yLjc2MTY0NEM1LjU3MTEwOC0yLjcxMzgyMyA1LjU1OTE1My0yLjY1NDA0NyA1LjU1OTE1My0yLjYzMDEzN0M1LjU1OTE1My0yLjU0NjQ1MSA1LjYwNjk3NC0yLjQ5ODYzIDUuNjkwNjYtMi40OTg2M0M1Ljc4NjMwMS0yLjQ5ODYzIDUuNzk4MjU3LTIuNTQ2NDUxIDUuODQ2MDc3LTIuNzM3NzMzTDYuNTM5NDc3LTUuNTIzMjg4QzYuNTM5NDc3LTUuNTcxMTA4IDYuNTAzNjExLTUuNjQyODM5IDYuNDE5OTI1LTUuNjQyODM5QzYuMzEyMzI5LTUuNjQyODM5IDYuMzAwMzc0LTUuNTk1MDE5IDYuMjUyNTUzLTUuMzkxNzgxQzYuMDAxNDk0LTQuNDk1MTQzIDUuNzYyMzkxLTQuMjQ0MDg1IDQuNzIyMjkxLTQuMjQ0MDg1SDMuNjM0MzcxTDQuNDExNDU3LTcuMzQwNDczQzQuNTE5MDU0LTcuNzU4OTA0IDQuNTQyOTY0LTcuNzk0NzcgNS4wMzMxMjYtNy43OTQ3N0g2LjYzNTExOEM4LjEyOTUxNC03Ljc5NDc3IDguMzQ0NzA3LTcuMzUyNDI4IDguMzQ0NzA3LTYuNTAzNjExQzguMzQ0NzA3LTYuNDMxODggOC4zNDQ3MDctNi4xNjg4NjcgOC4zMDg4NDItNS44NTgwMzJDOC4yOTY4ODctNS44MTAyMTIgOC4yNzI5NzYtNS42NTQ3OTUgOC4yNzI5NzYtNS42MDY5NzRDOC4yNzI5NzYtNS41MTEzMzMgOC4zMzI3NTItNS40NzU0NjcgOC40MDQ0ODMtNS40NzU0NjdDOC40ODgxNjktNS40NzU0NjcgOC41MzU5OS01LjUyMzI4OCA4LjU1OTktNS43Mzg0ODFMOC44MTA5NTktNy44MzA2MzVDOC44MTA5NTktNy44NjY1MDEgOC44MzQ4NjktNy45ODYwNTIgOC44MzQ4NjktOC4wMDk5NjNDOC44MzQ4NjktOC4xNDE0NjkgOC43MjcyNzMtOC4xNDE0NjkgOC41MTIwOC04LjE0MTQ2OUgyLjg0NTMzQzIuNjE4MTgyLTguMTQxNDY5IDIuNDk4NjMtOC4xNDE0NjkgMi40OTg2My03LjkyNjI3NkMyLjQ5ODYzLTcuNzk0NzcgMi41ODIzMTYtNy43OTQ3NyAyLjc4NTU1NC03Ljc5NDc3QzMuNTI2Nzc1LTcuNzk0NzcgMy41MjY3NzUtNy43MTEwODMgMy41MjY3NzUtNy41Nzk1NzdDMy41MjY3NzUtNy41MTk4MDEgMy41MTQ4MTktNy40NzE5OCAzLjQ3ODk1NC03LjM0MDQ3M0wxLjg2NTAwNi0uODg0NjgyQzEuNzU3NDEtLjQ2NjI1MiAxLjczMzQ5OS0uMzQ2NyAuODk2NjM4LS4zNDY3Qy42Njk0ODktLjM0NjcgLjU0OTkzOC0uMzQ2NyAuNTQ5OTM4LS4xMzE1MDdDLjU0OTkzOCAwIC42NTc1MzQgMCAuNzI5MjY1IDBDLjk1NjQxMyAwIDEuMTk1NTE3LS4wMjM5MSAxLjQyMjY2NS0uMDIzOTFIMi45NzY4MzdDMy4yMzk4NTEtLjAyMzkxIDMuNTI2Nzc1IDAgMy43ODk3ODggMEMzLjg5NzM4NSAwIDQuMDQwODQ3IDAgNC4wNDA4NDctLjIxNTE5M0M0LjA0MDg0Ny0uMzQ2NyAzLjk2OTExNi0uMzQ2NyAzLjcwNjEwMi0uMzQ2N0MyLjc2MTY0NC0uMzQ2NyAyLjczNzczMy0uNDMwMzg2IDIuNzM3NzMzLS42MDk3MTRDMi43Mzc3MzMtLjY2OTQ4OSAyLjc2MTY0NC0uNzY1MTMxIDIuNzg1NTU0LS44NDg4MTdMMy41NTA2ODUtMy44OTczODVaJy8+CjxwYXRoIGlkPSdnMi04OCcgZD0nTTUuNjc4NzA1LTQuODUzNzk4TDQuNTU0OTE5LTcuNDcxOThDNC43MTAzMzYtNy43NTg5MDQgNS4wNjg5OTEtNy44MDY3MjUgNS4yMTI0NTMtNy44MTg2OEM1LjI4NDE4NC03LjgxODY4IDUuNDE1NjkxLTcuODMwNjM1IDUuNDE1NjkxLTguMDMzODczQzUuNDE1NjkxLTguMTY1MzggNS4zMDgwOTUtOC4xNjUzOCA1LjIzNjM2NC04LjE2NTM4QzUuMDMzMTI2LTguMTY1MzggNC43OTQwMjItOC4xNDE0NjkgNC41OTA3ODUtOC4xNDE0NjlIMy44OTczODVDMy4xNjgxMi04LjE0MTQ2OSAyLjY0MjA5Mi04LjE2NTM4IDIuNjMwMTM3LTguMTY1MzhDMi41MzQ0OTYtOC4xNjUzOCAyLjQxNDk0NC04LjE2NTM4IDIuNDE0OTQ0LTcuOTM4MjMyQzIuNDE0OTQ0LTcuODE4NjggMi41MjI1NC03LjgxODY4IDIuNjc3OTU4LTcuODE4NjhDMy4zNzEzNTctNy44MTg2OCAzLjQxOTE3OC03LjY5OTEyOCAzLjUzODczLTcuNDEyMjA0TDQuOTYxMzk1LTQuMDg4NjY3TDIuMzY3MTIzLTEuMzE1MDY4QzEuOTM2NzM3LS44NDg4MTcgMS40MjI2NjUtLjM5NDUyMSAuNTM3OTgzLS4zNDY3Qy4zOTQ1MjEtLjMzNDc0NSAuMjk4ODc5LS4zMzQ3NDUgLjI5ODg3OS0uMTE5NTUyQy4yOTg4NzktLjA4MzY4NiAuMzEwODM0IDAgLjQ0MjM0MSAwQy42MDk3MTQgMCAuNzg5MDQxLS4wMjM5MSAuOTU2NDEzLS4wMjM5MUgxLjUxODMwNkMxLjkwMDg3Mi0uMDIzOTEgMi4zMTkzMDMgMCAyLjY4OTkxMyAwQzIuNzczNTk5IDAgMi45MTcwNjEgMCAyLjkxNzA2MS0uMjE1MTkzQzIuOTE3MDYxLS4zMzQ3NDUgMi44MzMzNzUtLjM0NjcgMi43NjE2NDQtLjM0NjdDMi41MjI1NC0uMzcwNjEgMi4zNjcxMjMtLjUwMjExNyAyLjM2NzEyMy0uNjkzNEMyLjM2NzEyMy0uODk2NjM4IDIuNTEwNTg1LTEuMDQwMSAyLjg1NzI4NS0xLjM5ODc1NUwzLjkyMTI5NS0yLjU1ODQwNkM0LjE4NDMwOS0yLjgzMzM3NSA0LjgxNzkzMy0zLjUyNjc3NSA1LjA4MDk0Ni0zLjc4OTc4OEw2LjMzNjIzOS0uODQ4ODE3QzYuMzQ4MTk0LS44MjQ5MDcgNi4zOTYwMTUtLjcwNTM1NSA2LjM5NjAxNS0uNjkzNEM2LjM5NjAxNS0uNTg1ODAzIDYuMTMzMDAxLS4zNzA2MSA1Ljc1MDQzNi0uMzQ2N0M1LjY3ODcwNS0uMzQ2NyA1LjU0NzE5OC0uMzM0NzQ1IDUuNTQ3MTk4LS4xMTk1NTJDNS41NDcxOTggMCA1LjY2Njc1IDAgNS43MjY1MjYgMEM1LjkyOTc2MyAwIDYuMTY4ODY3LS4wMjM5MSA2LjM3MjEwNS0uMDIzOTFINy42ODcxNzNDNy45MDIzNjYtLjAyMzkxIDguMTI5NTE0IDAgOC4zMzI3NTIgMEM4LjQxNjQzOCAwIDguNTQ3OTQ1IDAgOC41NDc5NDUtLjIyNzE0OEM4LjU0Nzk0NS0uMzQ2NyA4LjQyODM5NC0uMzQ2NyA4LjMyMDc5Ny0uMzQ2N0M3LjYwMzQ4Ny0uMzU4NjU1IDcuNTc5NTc3LS40MTg0MzEgNy4zNzYzMzktLjg2MDc3Mkw1Ljc5ODI1Ny00LjU2Njg3NEw3LjMxNjU2My02LjE5Mjc3N0M3LjQzNjExNS02LjMxMjMyOSA3LjcxMTA4My02LjYxMTIwOCA3LjgxODY4LTYuNzMwNzZDOC4zMzI3NTItNy4yNjg3NDIgOC44MTA5NTktNy43NTg5MDQgOS43NzkzMjgtNy44MTg2OEM5Ljg5ODg3OS03LjgzMDYzNSAxMC4wMTg0MzEtNy44MzA2MzUgMTAuMDE4NDMxLTguMDMzODczQzEwLjAxODQzMS04LjE2NTM4IDkuOTEwODM0LTguMTY1MzggOS44NjMwMTQtOC4xNjUzOEM5LjY5NTY0MS04LjE2NTM4IDkuNTE2MzE0LTguMTQxNDY5IDkuMzQ4OTQxLTguMTQxNDY5SDguNzk5MDA0QzguNDE2NDM4LTguMTQxNDY5IDcuOTk4MDA3LTguMTY1MzggNy42MjczOTctOC4xNjUzOEM3LjU0MzcxMS04LjE2NTM4IDcuNDAwMjQ5LTguMTY1MzggNy40MDAyNDktNy45NTAxODdDNy40MDAyNDktNy44MzA2MzUgNy40ODM5MzUtNy44MTg2OCA3LjU1NTY2Ni03LjgxODY4QzcuNzQ2OTQ5LTcuNzk0NzcgNy45NTAxODctNy42OTkxMjggNy45NTAxODctNy40NzE5OEw3LjkzODIzMi03LjQ0ODA3QzcuOTI2Mjc2LTcuMzY0Mzg0IDcuOTAyMzY2LTcuMjQ0ODMyIDcuNzcwODU5LTcuMTAxMzdMNS42Nzg3MDUtNC44NTM3OThaJy8+CjxwYXRoIGlkPSdnMi0xMTEnIGQ9J001LjQ1MTU1Ny0zLjI4NzY3MUM1LjQ1MTU1Ny00LjQyMzQxMiA0LjcxMDMzNi01LjI3MjIyOSAzLjYyMjQxNi01LjI3MjIyOUMyLjA0NDMzNC01LjI3MjIyOSAuNDkwMTYyLTMuNTUwNjg1IC40OTAxNjItMS44NjUwMDZDLjQ5MDE2Mi0uNzI5MjY1IDEuMjMxMzgyIC4xMTk1NTIgMi4zMTkzMDMgLjExOTU1MkMzLjkwOTM0IC4xMTk1NTIgNS40NTE1NTctMS42MDE5OTMgNS40NTE1NTctMy4yODc2NzFaTTIuMzMxMjU4LS4xMTk1NTJDMS43MzM0OTktLjExOTU1MiAxLjI5MTE1OC0uNTk3NzU4IDEuMjkxMTU4LTEuNDM0NjJDMS4yOTExNTgtMS45ODQ1NTggMS41NzgwODItMy4yMDM5ODUgMS45MTI4MjctMy44MDE3NDNDMi40NTA4MDktNC43MjIyOTEgMy4xMjAyOTktNS4wMzMxMjYgMy42MTA0NjEtNS4wMzMxMjZDNC4xOTYyNjQtNS4wMzMxMjYgNC42NTA1Ni00LjU1NDkxOSA0LjY1MDU2LTMuNzE4MDU3QzQuNjUwNTYtMy4yMzk4NTEgNC4zOTk1MDItMS45NjA2NDggMy45NDUyMDUtMS4yMzEzODJDMy40NTUwNDQtLjQzMDM4NiAyLjc5NzUwOS0uMTE5NTUyIDIuMzMxMjU4LS4xMTk1NTJaJy8+CjxwYXRoIGlkPSdnMi0xMTcnIGQ9J000LjA3NjcxMi0uNjkzNEM0LjIzMjEzLS4wMjM5MSA0LjgwNTk3OCAuMTE5NTUyIDUuMDkyOTAyIC4xMTk1NTJDNS40NzU0NjcgLjExOTU1MiA1Ljc2MjM5MS0uMTMxNTA3IDUuOTUzNjc0LS41Mzc5ODNDNi4xNTY5MTItLjk2ODM2OSA2LjMxMjMyOS0xLjY3MzcyNCA2LjMxMjMyOS0xLjcwOTU4OUM2LjMxMjMyOS0xLjc2OTM2NSA2LjI2NDUwOC0xLjgxNzE4NiA2LjE5Mjc3Ny0xLjgxNzE4NkM2LjA4NTE4MS0xLjgxNzE4NiA2LjA3MzIyNS0xLjc1NzQxIDYuMDI1NDA1LTEuNTc4MDgyQzUuODEwMjEyLS43NTMxNzYgNS41OTUwMTktLjExOTU1MiA1LjExNjgxMi0uMTE5NTUyQzQuNzU4MTU3LS4xMTk1NTIgNC43NTgxNTctLjUxNDA3MiA0Ljc1ODE1Ny0uNjY5NDg5QzQuNzU4MTU3LS45NDQ0NTggNC43OTQwMjItMS4wNjQwMSA0LjkxMzU3NC0xLjU2NjEyN0M0Ljk5NzI2LTEuODg4OTE3IDUuMDgwOTQ2LTIuMjExNzA2IDUuMTUyNjc3LTIuNTQ2NDUxTDUuNjQyODM5LTQuNDk1MTQzQzUuNzI2NTI2LTQuNzk0MDIyIDUuNzI2NTI2LTQuODE3OTMzIDUuNzI2NTI2LTQuODUzNzk4QzUuNzI2NTI2LTUuMDMzMTI2IDUuNTgzMDY0LTUuMTUyNjc3IDUuNDAzNzM2LTUuMTUyNjc3QzUuMDU3MDM2LTUuMTUyNjc3IDQuOTczMzUtNC44NTM3OTggNC45MDE2MTktNC41NTQ5MTlDNC43ODIwNjctNC4wODg2NjcgNC4xMzY0ODgtMS41MTgzMDYgNC4wNTI4MDItMS4wOTk4NzVDNC4wNDA4NDctMS4wOTk4NzUgMy41NzQ1OTUtLjExOTU1MiAyLjcwMTg2OC0uMTE5NTUyQzIuMDgwMTk5LS4xMTk1NTIgMS45NjA2NDgtLjY1NzUzNCAxLjk2MDY0OC0xLjA5OTg3NUMxLjk2MDY0OC0xLjc4MTMyIDIuMjk1MzkyLTIuNzM3NzMzIDIuNjA2MjI3LTMuNTM4NzNDMi43NDk2ODktMy45MjEyOTUgMi44MDk0NjUtNC4wNzY3MTIgMi44MDk0NjUtNC4zMTU4MTZDMi44MDk0NjUtNC44Mjk4ODggMi40Mzg4NTQtNS4yNzIyMjkgMS44NjUwMDYtNS4yNzIyMjlDLjc2NTEzMS01LjI3MjIyOSAuMzIyNzktMy41Mzg3MyAuMzIyNzktMy40NDMwODhDLjMyMjc5LTMuMzk1MjY4IC4zNzA2MS0zLjMzNTQ5MiAuNDU0Mjk2LTMuMzM1NDkyQy41NjE4OTMtMy4zMzU0OTIgLjU3Mzg0OC0zLjM4MzMxMyAuNjIxNjY5LTMuNTUwNjg1Qy45MDg1OTMtNC41Nzg4MjkgMS4zNzQ4NDQtNS4wMzMxMjYgMS44MjkxNDEtNS4wMzMxMjZDMS45NDg2OTItNS4wMzMxMjYgMi4xMzk5NzUtNS4wMjExNzEgMi4xMzk5NzUtNC42Mzg2MDVDMi4xMzk5NzUtNC4zMjc3NzEgMi4wMDg0NjgtMy45ODEwNzEgMS44MjkxNDEtMy41MjY3NzVDMS4zMDMxMTMtMi4xMDQxMSAxLjI0MzMzNy0xLjY0OTgxMyAxLjI0MzMzNy0xLjI5MTE1OEMxLjI0MzMzNy0uMDcxNzMxIDIuMTYzODg1IC4xMTk1NTIgMi42NTQwNDcgLjExOTU1MkMzLjQxOTE3OCAuMTE5NTUyIDMuODM3NjA5LS40MDY0NzYgNC4wNzY3MTItLjY5MzRaJy8+CjwvZGVmcz4KPGcgaWQ9J3BhZ2UxJz4KPHVzZSB4PScyMy42NDg0NycgeT0nLTkuMTk2OTI2JyB4bGluazpocmVmPScjZzItMzEnLz4KPHVzZSB4PSczMC45ODIwMjcnIHk9Jy05LjE5NjkyNicgeGxpbms6aHJlZj0nI2c0LTQwJy8+Cjx1c2UgeD0nMzUuNTM0MzUzJyB5PSctOS4xOTY5MjYnIHhsaW5rOmhyZWY9JyNnMi0xMTcnLz4KPHVzZSB4PSc0Mi4xOTY3OTInIHk9Jy05LjE5NjkyNicgeGxpbms6aHJlZj0nI2c0LTQxJy8+Cjx1c2UgeD0nNTAuMDY5OTQ3JyB5PSctOS4xOTY5MjYnIHhsaW5rOmhyZWY9JyNnNC02MScvPgo8dXNlIHg9JzYyLjQ5NTQyOCcgeT0nLTkuMTk2OTI2JyB4bGluazpocmVmPScjZzQtNTAnLz4KPHVzZSB4PSc3MS4wMDUwODInIHk9Jy05LjE5NjkyNicgeGxpbms6aHJlZj0nI2cxLTAnLz4KPHVzZSB4PSc4NC4xNTU3NTYnIHk9Jy0xNy4yODQ2ODUnIHhsaW5rOmhyZWY9JyNnNC00OScvPgo8dXNlIHg9JzkyLjY2NTQxJyB5PSctMTcuMjg0Njg1JyB4bGluazpocmVmPScjZzEtMCcvPgo8dXNlIHg9JzEwNC42MjA1NycgeT0nLTE3LjI4NDY4NScgeGxpbms6aHJlZj0nI2cyLTY3Jy8+Cjx1c2UgeD0nMTEzLjg1NDE4MicgeT0nLTE3LjI4NDY4NScgeGxpbms6aHJlZj0nI2c0LTQwJy8+Cjx1c2UgeD0nMTE4LjQwNjUwOCcgeT0nLTE3LjI4NDY4NScgeGxpbms6aHJlZj0nI2cyLTExNycvPgo8dXNlIHg9JzEyNS4wNjg5NDgnIHk9Jy0xNy4yODQ2ODUnIHhsaW5rOmhyZWY9JyNnMi01OScvPgo8dXNlIHg9JzEzMC4zMTMxMDcnIHk9Jy0xNy4yODQ2ODUnIHhsaW5rOmhyZWY9JyNnMi0xMTcnLz4KPHVzZSB4PScxMzYuOTc1NTQ2JyB5PSctMTcuMjg0Njg1JyB4bGluazpocmVmPScjZzQtNDEnLz4KPHJlY3QgeD0nODQuMTU1NzU2JyB5PSctMTIuNDI0ODEyJyBoZWlnaHQ9Jy40NzgxODcnIHdpZHRoPSc1Ny4zNzIxMDQnLz4KPHVzZSB4PSc5OS4yNzgxODUnIHk9Jy0uOTk2MjY0JyB4bGluazpocmVmPScjZzQtNDknLz4KPHVzZSB4PScxMDcuNzg3ODM5JyB5PSctLjk5NjI2NCcgeGxpbms6aHJlZj0nI2cxLTAnLz4KPHVzZSB4PScxMTkuNzQyOTk5JyB5PSctLjk5NjI2NCcgeGxpbms6aHJlZj0nI2cyLTExNycvPgo8dXNlIHg9JzE0NS4zODAwMzgnIHk9Jy05LjE5NjkyNicgeGxpbms6aHJlZj0nI2c0LTQzJy8+Cjx1c2UgeD0nMTU3LjE0MTM1MycgeT0nLTkuMTk2OTI2JyB4bGluazpocmVmPScjZzItMTExJy8+Cjx1c2UgeD0nMTYyLjc2ODc5JyB5PSctOS4xOTY5MjYnIHhsaW5rOmhyZWY9JyNnNC00MCcvPgo8dXNlIHg9JzE2Ny4zMjExMTYnIHk9Jy05LjE5NjkyNicgeGxpbms6aHJlZj0nI2c0LTQ5Jy8+Cjx1c2UgeD0nMTczLjE3NDEwNicgeT0nLTkuMTk2OTI2JyB4bGluazpocmVmPScjZzQtNDEnLz4KPHVzZSB4PScxODEuMDQ3MjYxJyB5PSctOS4xOTY5MjYnIHhsaW5rOmhyZWY9JyNnNC02MScvPgo8dXNlIHg9JzE5My40NzI3NDInIHk9Jy05LjE5NjkyNicgeGxpbms6aHJlZj0nI2cwLTgwJy8+Cjx1c2UgeD0nMjAwLjc3ODY5NicgeT0nLTkuMTk2OTI2JyB4bGluazpocmVmPScjZzQtOTEnLz4KPHVzZSB4PScyMDQuMDMwMzU3JyB5PSctOS4xOTY5MjYnIHhsaW5rOmhyZWY9JyNnMi03MCcvPgo8dXNlIHg9JzIxMS42MDgxNDInIHk9Jy03LjQwMzY2MycgeGxpbms6aHJlZj0nI2czLTUwJy8+Cjx1c2UgeD0nMjE2LjM0MDQ1NycgeT0nLTkuMTk2OTI2JyB4bGluazpocmVmPScjZzQtNDAnLz4KPHVzZSB4PScyMjAuODkyNzgyJyB5PSctOS4xOTY5MjYnIHhsaW5rOmhyZWY9JyNnMi04OCcvPgo8dXNlIHg9JzIzMC42MDgwMScgeT0nLTcuNDAzNjYzJyB4bGluazpocmVmPScjZzMtNTAnLz4KPHVzZSB4PScyMzUuMzQwMzI1JyB5PSctOS4xOTY5MjYnIHhsaW5rOmhyZWY9JyNnNC00MScvPgo8dXNlIHg9JzI0My4yMTM0OCcgeT0nLTkuMTk2OTI2JyB4bGluazpocmVmPScjZzItNjInLz4KPHVzZSB4PScyNTUuNjM4OTYxJyB5PSctOS4xOTY5MjYnIHhsaW5rOmhyZWY9JyNnMi0xMTcnLz4KPHVzZSB4PScyNjIuMzAxNCcgeT0nLTkuMTk2OTI2JyB4bGluazpocmVmPScjZzEtMTA2Jy8+Cjx1c2UgeD0nMjY1LjYyMjI5JyB5PSctOS4xOTY5MjYnIHhsaW5rOmhyZWY9JyNnMi03MCcvPgo8dXNlIHg9JzI3NC44MjU5MDUnIHk9Jy05LjE5NjkyNicgeGxpbms6aHJlZj0nI2c0LTQ5Jy8+Cjx1c2UgeD0nMjgwLjY3ODg5NicgeT0nLTkuMTk2OTI2JyB4bGluazpocmVmPScjZzQtNDAnLz4KPHVzZSB4PScyODUuMjMxMjIxJyB5PSctOS4xOTY5MjYnIHhsaW5rOmhyZWY9JyNnMi04OCcvPgo8dXNlIHg9JzI5NC45NDY0NDknIHk9Jy03LjQwMzY2MycgeGxpbms6aHJlZj0nI2czLTQ5Jy8+Cjx1c2UgeD0nMjk5LjY3ODc2NCcgeT0nLTkuMTk2OTI2JyB4bGluazpocmVmPScjZzQtNDEnLz4KPHVzZSB4PSczMDcuNTUxOTE5JyB5PSctOS4xOTY5MjYnIHhsaW5rOmhyZWY9JyNnMi02MicvPgo8dXNlIHg9JzMxOS45Nzc0JyB5PSctOS4xOTY5MjYnIHhsaW5rOmhyZWY9JyNnMi0xMTcnLz4KPHVzZSB4PSczMjYuNjM5ODM5JyB5PSctOS4xOTY5MjYnIHhsaW5rOmhyZWY9JyNnNC05MycvPgo8dXNlIHg9JzMzMi41NDgxNjQnIHk9Jy05LjE5NjkyNicgeGxpbms6aHJlZj0nI2c0LTQzJy8+Cjx1c2UgeD0nMzQ0LjMwOTQ3OScgeT0nLTkuMTk2OTI2JyB4bGluazpocmVmPScjZzItMTExJy8+Cjx1c2UgeD0nMzQ5LjkzNjkxNicgeT0nLTkuMTk2OTI2JyB4bGluazpocmVmPScjZzQtNDAnLz4KPHVzZSB4PSczNTQuNDg5MjQyJyB5PSctOS4xOTY5MjYnIHhsaW5rOmhyZWY9JyNnNC00OScvPgo8dXNlIHg9JzM2MC4zNDIyMzInIHk9Jy05LjE5NjkyNicgeGxpbms6aHJlZj0nI2c0LTQxJy8+CjwvZz4KPC9zdmc+CjwhLS0gREVQVEg9MCAtLT4=)

which proves that:

Next to providing the limit , the function also provides some insight in the

dependence structure of the variables at lower quantile levels: the larger  the more

correlated are the variables.

the more

correlated are the variables.

The function is estimated on data for several which must not be too high because

of a problem of lack of data greater than . Condifence intervals can be estimated on each

. If the confidence interval contains the zero value when tends to , then we can assume that .

Within the class of asymptotically dependent variables, the value of increases with increasing degree of dependence at extreme levels.

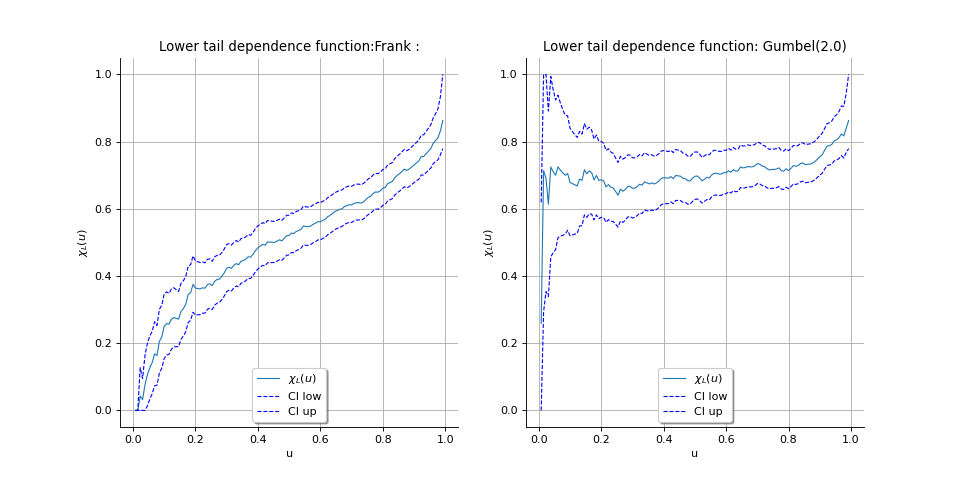

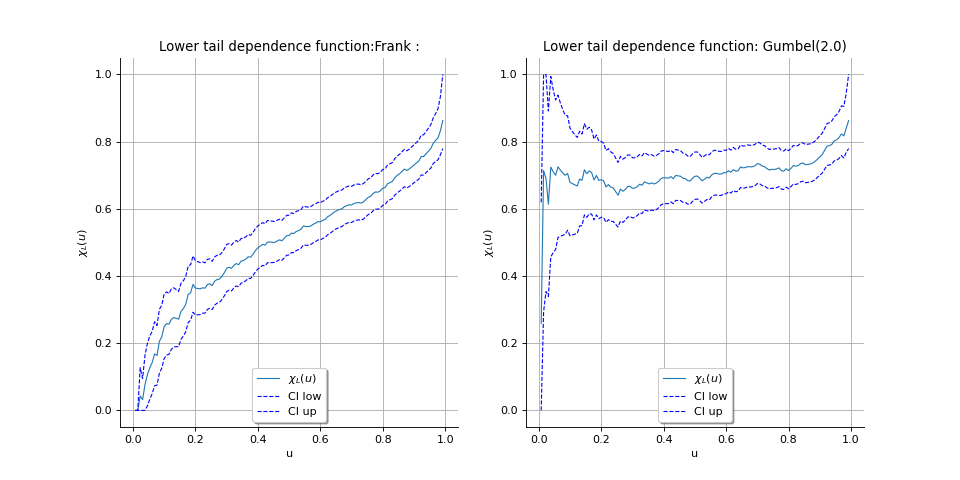

We illustrate two cases where the variables are:

asymptotically independent: we generated a sample of size

from a Frank copula which has a

zero upper tail coefficient whatever the parameter,

from a Frank copula which has a

zero upper tail coefficient whatever the parameter,asymptotically dependent: we generated a sample of size

from a Gumbel copula parametrized

by  which has a positive upper tail coefficient.

which has a positive upper tail coefficient.

(Source code, png)

{kind=link}

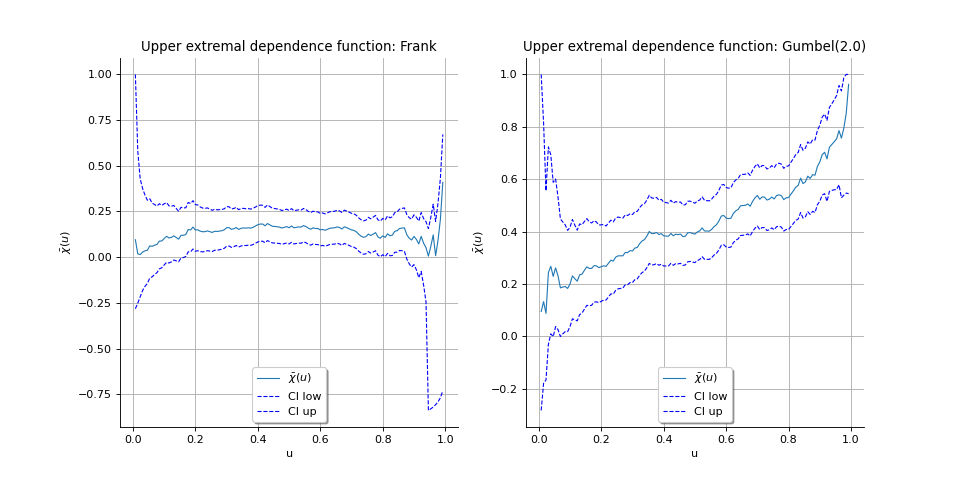

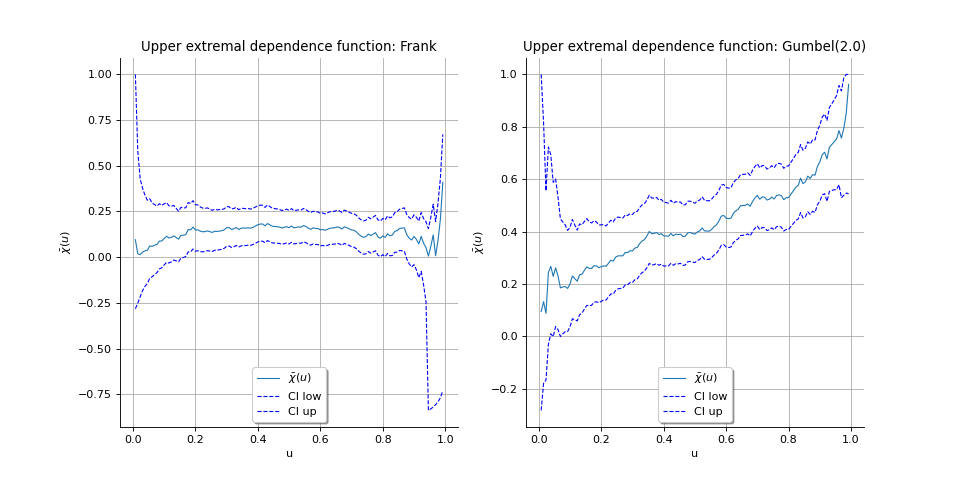

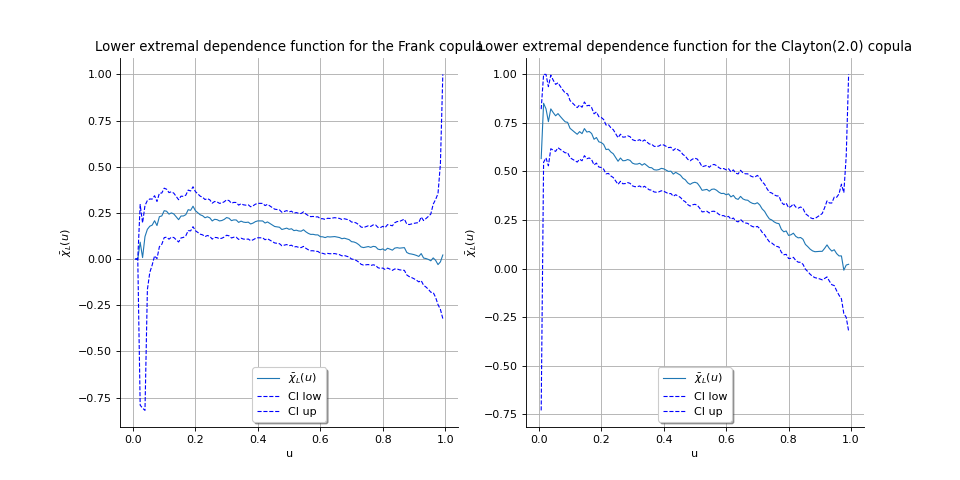

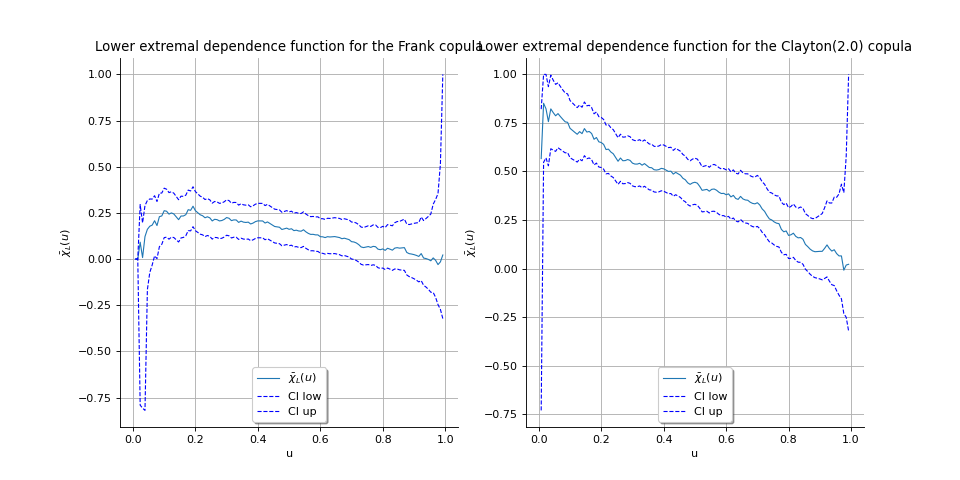

Upper extremal dependence coefficient

Within the class of asymptotically independent variables, the degrees of relative strength of dependence is

given by the function defined by: