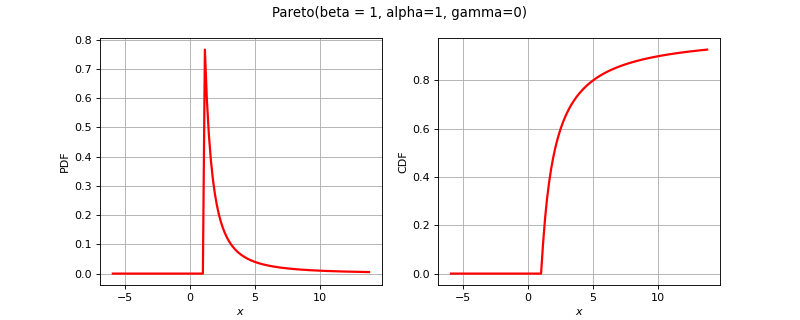

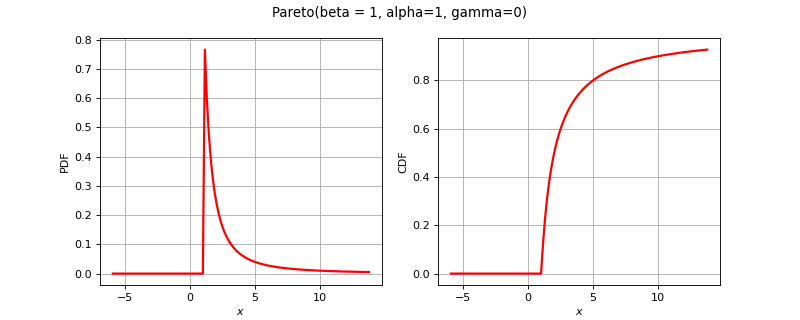

Pareto distribution¶

(Source code, png)

- class Pareto(*args)¶

Pareto distribution.

- Parameters:

- betafloat

Scale parameter

.

.- alphafloat,

Shape parameter

.

.- gammafloat

Location parameter

.

.

Notes

Its cumulative and probability distribution functions are defined as:

with

and .Its first moments are:

![\begin{eqnarray*}

\Expect{X} & = & \gamma + \frac{\alpha}{\alpha + 1}\beta

\quad \text{ if } \alpha > 1 \\

\Var{X} & = & \dfrac{\alpha}{\alpha-2}\left(\dfrac{\beta}{\alpha - 1} \right)^2 \quad \text{ if } \alpha > 2 \\

Skew[X] & = & \dfrac{2(1+\alpha)}{\alpha-3}\sqrt{\dfrac{\alpha-2}{\alpha}} \quad \text{ if } \alpha > 3

\end{eqnarray*}](data:image/svg+xml;base64,PD94bWwgdmVyc2lvbj0nMS4wJyBlbmNvZGluZz0nVVRGLTgnPz4KPCEtLSBUaGlzIGZpbGUgd2FzIGdlbmVyYXRlZCBieSBkdmlzdmdtIDMuMS4yIC0tPgo8c3ZnIHZlcnNpb249JzEuMScgeG1sbnM9J2h0dHA6Ly93d3cudzMub3JnLzIwMDAvc3ZnJyB4bWxuczp4bGluaz0naHR0cDovL3d3dy53My5vcmcvMTk5OS94bGluaycgd2lkdGg9JzIxNy42MjE3NDNwdCcgaGVpZ2h0PSc5MC4xNjQxMjRwdCcgdmlld0JveD0nODUuNDYwNjIgLTkwLjE2NDExNiAyMTcuNjIxNzQzIDkwLjE2NDEyNCc+CjxkZWZzPgo8cGF0aCBpZD0nZzQtNTAnIGQ9J00yLjI0NzU3Mi0xLjYyNTkwM0MyLjM3NTA5My0xLjc0NTQ1NSAyLjcwOTgzOC0yLjAwODQ2OCAyLjgzNzM2LTIuMTIwMDVDMy4zMzE1MDctMi41NzQzNDYgMy44MDE3NDMtMy4wMTI3MDIgMy44MDE3NDMtMy43Mzc5ODNDMy44MDE3NDMtNC42ODY0MjYgMy4wMDQ3MzItNS4zMDAxMjUgMi4wMDg0NjgtNS4zMDAxMjVDMS4wNTIwNTUtNS4zMDAxMjUgLjQyMjQxNi00LjU3NDg0NCAuNDIyNDE2LTMuODY1NTA0Qy40MjI0MTYtMy40NzQ5NjkgLjczMzI1LTMuNDE5MTc4IC44NDQ4MzItMy40MTkxNzhDMS4wMTIyMDQtMy40MTkxNzggMS4yNTkyNzgtMy41Mzg3MyAxLjI1OTI3OC0zLjg0MTU5NEMxLjI1OTI3OC00LjI1NjA0IC44NjA3NzItNC4yNTYwNCAuNzY1MTMxLTQuMjU2MDRDLjk5NjI2NC00LjgzNzg1OCAxLjUzMDI2Mi01LjAzNzExMSAxLjkyMDc5Ny01LjAzNzExMUMyLjY2MjAxNy01LjAzNzExMSAzLjA0NDU4My00LjQwNzQ3MiAzLjA0NDU4My0zLjczNzk4M0MzLjA0NDU4My0yLjkwOTA5MSAyLjQ2Mjc2NS0yLjMwMzM2MiAxLjUyMjI5MS0xLjMzODk3OUwuNTE4MDU3LS4zMDI4NjRDLjQyMjQxNi0uMjE1MTkzIC40MjI0MTYtLjE5OTI1MyAuNDIyNDE2IDBIMy41NzA2MUwzLjgwMTc0My0xLjQyNjY1SDMuNTU0NjdDMy41MzA3Ni0xLjI2NzI0OCAzLjQ2Njk5OS0uODY4NzQyIDMuMzcxMzU3LS43MTczMUMzLjMyMzUzNy0uNjUzNTQ5IDIuNzE3ODA4LS42NTM1NDkgMi41OTAyODYtLjY1MzU0OUgxLjE3MTYwNkwyLjI0NzU3Mi0xLjYyNTkwM1onLz4KPHBhdGggaWQ9J2cyLTAnIGQ9J003Ljg3ODQ1Ni0yLjc0OTY4OUM4LjA4MTY5NC0yLjc0OTY4OSA4LjI5Njg4Ny0yLjc0OTY4OSA4LjI5Njg4Ny0yLjk4ODc5MlM4LjA4MTY5NC0zLjIyNzg5NSA3Ljg3ODQ1Ni0zLjIyNzg5NUgxLjQxMDcxQzEuMjA3NDcyLTMuMjI3ODk1IC45OTIyNzktMy4yMjc4OTUgLjk5MjI3OS0yLjk4ODc5MlMxLjIwNzQ3Mi0yLjc0OTY4OSAxLjQxMDcxLTIuNzQ5Njg5SDcuODc4NDU2WicvPgo8cGF0aCBpZD0nZzEtMTgnIGQ9J004LjM2ODYxOCAyOC4wODI2OUM4LjM2ODYxOCAyOC4wMzQ4NjkgOC4zNDQ3MDcgMjguMDEwOTU5IDguMzIwNzk3IDI3Ljk3NTA5M0M3Ljg3ODQ1NiAyNy41MzI3NTIgNy4wNzc0NiAyNi43MzE3NTYgNi4yNzY0NjMgMjUuNDQwNTk4QzQuMzUxNjgxIDIyLjM1NjE2NCAzLjQ3ODk1NCAxOC40NzA3MzUgMy40Nzg5NTQgMTMuODY3OTk1QzMuNDc4OTU0IDEwLjY1MjA1NSAzLjkwOTM0IDYuNTAzNjExIDUuODgxOTQzIDIuOTQwOTcxQzYuODI2NDAxIDEuMjQzMzM3IDcuODA2NzI1IC4yNjMwMTQgOC4zMzI3NTItLjI2MzAxNEM4LjM2ODYxOC0uMjk4ODc5IDguMzY4NjE4LS4zMjI3OSA4LjM2ODYxOC0uMzU4NjU1QzguMzY4NjE4LS40NzgyMDcgOC4yODQ5MzItLjQ3ODIwNyA4LjExNzU1OS0uNDc4MjA3UzcuOTI2Mjc2LS40NzgyMDcgNy43NDY5NDktLjI5ODg3OUMzLjc0MTk2OCAzLjM0NzQ0NyAyLjQ4NjY3NSA4LjgyMjkxNCAyLjQ4NjY3NSAxMy44NTYwNEMyLjQ4NjY3NSAxOC41NTQ0MjEgMy41NjI2NCAyMy4yODg2NjcgNi41OTkyNTMgMjYuODYzMjYzQzYuODM4MzU2IDI3LjEzODIzMiA3LjI5MjY1MyAyNy42MjgzOTQgNy43ODI4MTQgMjguMDU4NzhDNy45MjYyNzYgMjguMjAyMjQyIDcuOTUwMTg3IDI4LjIwMjI0MiA4LjExNzU1OSAyOC4yMDIyNDJTOC4zNjg2MTggMjguMjAyMjQyIDguMzY4NjE4IDI4LjA4MjY5WicvPgo8cGF0aCBpZD0nZzEtMTknIGQ9J002LjMwMDM3NCAxMy44Njc5OTVDNi4zMDAzNzQgOS4xNjk2MTQgNS4yMjQ0MDggNC40MzUzNjcgMi4xODc3OTYgLjg2MDc3MkMxLjk0ODY5MiAuNTg1ODAzIDEuNDk0Mzk2IC4wOTU2NDEgMS4wMDQyMzQtLjMzNDc0NUMuODYwNzcyLS40NzgyMDcgLjgzNjg2Mi0uNDc4MjA3IC42Njk0ODktLjQ3ODIwN0MuNTI2MDI3LS40NzgyMDcgLjQxODQzMS0uNDc4MjA3IC40MTg0MzEtLjM1ODY1NUMuNDE4NDMxLS4zMTA4MzQgLjQ2NjI1Mi0uMjYzMDE0IC40OTAxNjItLjIzOTEwM0MuOTA4NTkzIC4xOTEyODMgMS43MDk1ODkgLjk5MjI3OSAyLjUxMDU4NSAyLjI4MzQzN0M0LjQzNTM2NyA1LjM2Nzg3IDUuMzA4MDk1IDkuMjUzMyA1LjMwODA5NSAxMy44NTYwNEM1LjMwODA5NSAxNy4wNzE5OCA0Ljg3NzcwOSAyMS4yMjA0MjMgMi45MDUxMDYgMjQuNzgzMDY0QzEuOTYwNjQ4IDI2LjQ4MDY5NyAuOTY4MzY5IDI3LjQ3Mjk3NiAuNDY2MjUyIDI3Ljk3NTA5M0MuNDQyMzQxIDI4LjAxMDk1OSAuNDE4NDMxIDI4LjA0NjgyNCAuNDE4NDMxIDI4LjA4MjY5Qy40MTg0MzEgMjguMjAyMjQyIC41MjYwMjcgMjguMjAyMjQyIC42Njk0ODkgMjguMjAyMjQyQy44MzY4NjIgMjguMjAyMjQyIC44NjA3NzIgMjguMjAyMjQyIDEuMDQwMSAyOC4wMjI5MTRDNS4wNDUwODEgMjQuMzc2NTg4IDYuMzAwMzc0IDE4LjkwMTEyMSA2LjMwMDM3NCAxMy44Njc5OTVaJy8+CjxwYXRoIGlkPSdnMS0xMTQnIGQ9J001LjU3MTEwOCAyNS44NDcwNzNINS41NTkxNTNMMi45NzY4MzcgMTMuODY3OTk1TDEuNDEwNzEgMTYuMzMwNzZDMS4zMjcwMjQgMTYuNDM4MzU2IDEuMzI3MDI0IDE2LjQ2MjI2NyAxLjMyNzAyNCAxNi40NzQyMjJDMS4zMjcwMjQgMTYuNTIyMDQyIDEuNDgyNDQxIDE2LjY1MzU0OSAxLjQ5NDM5NiAxNi42NjU1MDRMMi4zMDczNDcgMTUuMzg2MzAxTDUuMDY4OTkxIDI4LjIxNDE5N0M1LjQ2MzUxMiAyOC4yMTQxOTcgNS40OTkzNzcgMjguMjE0MTk3IDUuNTcxMTA4IDI3LjkwMzM2MkwxMi4xNDY0NTEgLjAxMTk1NUMxMi4xNzAzNjEtLjA3MTczMSAxMi4xOTQyNzEtLjE3OTMyOCAxMi4xOTQyNzEtLjIzOTEwM0MxMi4xOTQyNzEtLjM3MDYxIDEyLjA5ODYzLS40NzgyMDcgMTEuOTU1MTY4LS40NzgyMDdDMTEuNzYzODg1LS40NzgyMDcgMTEuNzI4MDItLjMyMjc5IDExLjY5MjE1NC0uMTU1NDE3TDUuNTcxMTA4IDI1Ljg0NzA3M1onLz4KPHBhdGggaWQ9J2czLTExJyBkPSdNNS41MzUyNDMtMy4wMjQ2NThDNS41MzUyNDMtNC4xODQzMDkgNC44Nzc3MDktNS4yNzIyMjkgMy42MTA0NjEtNS4yNzIyMjlDMi4wNDQzMzQtNS4yNzIyMjkgLjQ3ODIwNy0zLjU2MjY0IC40NzgyMDctMS44NjUwMDZDLjQ3ODIwNy0uODI0OTA3IDEuMTIzNzg2IC4xMTk1NTIgMi4zNDMyMTMgLjExOTU1MkMzLjA4NDQzMyAuMTE5NTUyIDMuOTY5MTE2LS4xNjczNzIgNC44MTc5MzMtLjg4NDY4MkM0Ljk4NTMwNS0uMjE1MTkzIDUuMzU1OTE1IC4xMTk1NTIgNS44Njk5ODggLjExOTU1MkM2LjUxNTU2NyAuMTE5NTUyIDYuODM4MzU2LS41NDk5MzggNi44MzgzNTYtLjcwNTM1NUM2LjgzODM1Ni0uODEyOTUxIDYuNzU0NjctLjgxMjk1MSA2LjcxODgwNC0uODEyOTUxQzYuNjIzMTYzLS44MTI5NTEgNi42MTEyMDgtLjc3NzA4NiA2LjU3NTM0Mi0uNjgxNDQ1QzYuNDY3NzQ2LS4zODI1NjUgNi4xOTI3NzctLjExOTU1MiA1LjkwNTg1My0uMTE5NTUyQzUuNTM1MjQzLS4xMTk1NTIgNS41MzUyNDMtLjg4NDY4MiA1LjUzNTI0My0xLjYxMzk0OEM2Ljc1NDY3LTMuMDcyNDc4IDcuMDQxNTk0LTQuNTc4ODI5IDcuMDQxNTk0LTQuNTkwNzg1QzcuMDQxNTk0LTQuNjk4MzgxIDYuOTQ1OTUzLTQuNjk4MzgxIDYuOTEwMDg3LTQuNjk4MzgxQzYuODAyNDkxLTQuNjk4MzgxIDYuNzkwNTM1LTQuNjYyNTE2IDYuNzQyNzE1LTQuNDQ3MzIzQzYuNTg3Mjk4LTMuOTIxMjk1IDYuMjc2NDYzLTIuOTg4NzkyIDUuNTM1MjQzLTIuMDA4NDY4Vi0zLjAyNDY1OFpNNC43ODIwNjctMS4xNzE2MDZDMy43MzAwMTItLjIyNzE0OCAyLjc4NTU1NC0uMTE5NTUyIDIuMzY3MTIzLS4xMTk1NTJDMS41MTgzMDYtLjExOTU1MiAxLjI3OTIwMy0uODcyNzI3IDEuMjc5MjAzLTEuNDM0NjJDMS4yNzkyMDMtMS45NDg2OTIgMS41NDIyMTctMy4xNjgxMiAxLjkxMjgyNy0zLjgyNTY1NEMyLjQwMjk4OS00LjY2MjUxNiAzLjA3MjQ3OC01LjAzMzEyNiAzLjYxMDQ2MS01LjAzMzEyNkM0Ljc3MDExMi01LjAzMzEyNiA0Ljc3MDExMi0zLjUxNDgxOSA0Ljc3MDExMi0yLjUxMDU4NUM0Ljc3MDExMi0yLjIxMTcwNiA0Ljc1ODE1Ny0xLjkwMDg3MiA0Ljc1ODE1Ny0xLjYwMTk5M0M0Ljc1ODE1Ny0xLjM2Mjg4OSA0Ljc3MDExMi0xLjMwMzExMyA0Ljc4MjA2Ny0xLjE3MTYwNlonLz4KPHBhdGggaWQ9J2czLTEyJyBkPSdNNi43NjY2MjUtNi45NTc5MDhDNi43NjY2MjUtNy42NzUyMTggNi4xNTY5MTItOC40MjgzOTQgNS4wNjg5OTEtOC40MjgzOTRDMy41MjY3NzUtOC40MjgzOTQgMi41NDY0NTEtNi41Mzk0NzcgMi4yMzU2MTYtNS4yOTYxMzlMLjM0NjcgMi4xOTk3NTFDLjMyMjc5IDIuMjk1MzkyIC4zOTQ1MjEgMi4zMTkzMDMgLjQ1NDI5NiAyLjMxOTMwM0MuNTM3OTgzIDIuMzE5MzAzIC41OTc3NTggMi4zMDczNDcgLjYwOTcxNCAyLjI0NzU3MkwxLjQ0NjU3NS0xLjA5OTg3NUMxLjU2NjEyNy0uNDMwMzg2IDIuMjIzNjYxIC4xMTk1NTIgMi45MjkwMTYgLjExOTU1MkM0LjYzODYwNSAuMTE5NTUyIDYuMjUyNTUzLTEuMjE5NDI3IDYuMjUyNTUzLTMuMDAwNzQ3QzYuMjUyNTUzLTMuNDU1MDQ0IDYuMTQ0OTU2LTMuOTA5MzQgNS44OTM4OTgtNC4yOTE5MDVDNS43NTA0MzYtNC41MTkwNTQgNS41NzExMDgtNC42ODY0MjYgNS4zNzk4MjYtNC44Mjk4ODhDNi4yNDA1OTgtNS4yODQxODQgNi43NjY2MjUtNi4wMTM0NSA2Ljc2NjYyNS02Ljk1NzkwOFpNNC42ODY0MjYtNC44NDE4NDNDNC40OTUxNDMtNC43NzAxMTIgNC4zMDM4NjEtNC43NDYyMDIgNC4wNzY3MTItNC43NDYyMDJDMy45MDkzNC00Ljc0NjIwMiAzLjc1MzkyMy00LjczNDI0NyAzLjUzODczLTQuODA1OTc4QzMuNjU4MjgxLTQuODg5NjY0IDMuODM3NjA5LTQuOTEzNTc0IDQuMDg4NjY3LTQuOTEzNTc0QzQuMzAzODYxLTQuOTEzNTc0IDQuNTE5MDU0LTQuODg5NjY0IDQuNjg2NDI2LTQuODQxODQzWk02LjE0NDk1Ni03LjA2NTUwNEM2LjE0NDk1Ni02LjQwNzk3IDUuODIyMTY3LTUuNDUxNTU3IDUuMDQ1MDgxLTUuMDA5MjE1QzQuODE3OTMzLTUuMDkyOTAyIDQuNTA3MDk4LTUuMTUyNjc3IDQuMjQ0MDg1LTUuMTUyNjc3QzMuOTkzMDI2LTUuMTUyNjc3IDMuMjc1NzE2LTUuMTc2NTg4IDMuMjc1NzE2LTQuNzk0MDIyQzMuMjc1NzE2LTQuNDcxMjMzIDMuOTMzMjUtNC41MDcwOTggNC4xMzY0ODgtNC41MDcwOThDNC40NDczMjMtNC41MDcwOTggNC43MjIyOTEtNC41Nzg4MjkgNS4wMDkyMTUtNC42NjI1MTZDNS4zOTE3ODEtNC4zNTE2ODEgNS41NTkxNTMtMy45NDUyMDUgNS41NTkxNTMtMy4zNDc0NDdDNS41NTkxNTMtMi42NTQwNDcgNS4zNjc4Ny0yLjA5MjE1NCA1LjE0MDcyMi0xLjU3ODA4MkM0Ljc0NjIwMi0uNjkzNCAzLjgxMzY5OS0uMTE5NTUyIDIuOTg4NzkyLS4xMTk1NTJDMi4xMTYwNjUtLjExOTU1MiAxLjY2MTc2OC0uODEyOTUxIDEuNjYxNzY4LTEuNjI1OTAzQzEuNjYxNzY4LTEuNzMzNDk5IDEuNjYxNzY4LTEuODg4OTE3IDEuNzA5NTg5LTIuMDY4MjQ0TDIuNDg2Njc1LTUuMjEyNDUzQzIuODgxMTk2LTYuNzc4NTggMy44ODU0My04LjE4OTI5IDUuMDQ1MDgxLTguMTg5MjlDNS45MDU4NTMtOC4xODkyOSA2LjE0NDk1Ni03LjU5MTUzMiA2LjE0NDk1Ni03LjA2NTUwNFonLz4KPHBhdGggaWQ9J2czLTEzJyBkPSdNNC41MTkwNTQtMS40NTg1MzFDNC40OTUxNDMtMi4wNDQzMzQgNC40NzEyMzMtMi45NjQ4ODIgNC4wMTY5MzYtNC4wNDA4NDdDMy43Nzc4MzMtNC42Mzg2MDUgMy4zNzEzNTctNS4yNzIyMjkgMi40OTg2My01LjI3MjIyOUMxLjAyODE0NC01LjI3MjIyOSAuMjI3MTQ4LTMuMzk1MjY4IC4yMjcxNDgtMy4wODQ0MzNDLjIyNzE0OC0yLjk3NjgzNyAuMzEwODM0LTIuOTc2ODM3IC4zNDY3LTIuOTc2ODM3Qy40NTQyOTYtMi45NzY4MzcgLjQ1NDI5Ni0zLjAwMDc0NyAuNTE0MDcyLTMuMTU2MTY0Qy43NjUxMzEtMy44OTczODUgMS41MzAyNjItNC40ODMxODggMi4zNTUxNjgtNC40ODMxODhDNC4wMTY5MzYtNC40ODMxODggNC4yNTYwNC0yLjYzMDEzNyA0LjI1NjA0LTEuNDQ2NTc1QzQuMjU2MDQtLjY5MzQgNC4xNzIzNTQtLjQ0MjM0MSA0LjEwMDYyMy0uMjAzMjM4QzMuODczNDc0IC41Mzc5ODMgMy40Nzg5NTQgMi4wMjA0MjMgMy40Nzg5NTQgMi4zNTUxNjhDMy40Nzg5NTQgMi40NTA4MDkgMy41MTQ4MTkgMi41NTg0MDYgMy42MTA0NjEgMi41NTg0MDZDMy43ODk3ODggMi41NTg0MDYgMy44OTczODUgMi4xNjM4ODUgNC4wMjg4OTIgMS42ODU2NzlDNC4zMTU4MTYgLjYzMzYyNCA0LjM4NzU0NyAuMTA3NTk3IDQuNDQ3MzIzLS4zNzA2MUM0LjQ4MzE4OC0uNjU3NTM0IDUuMTY0NjMzLTIuNjMwMTM3IDYuMTA5MDkxLTQuNTA3MDk4QzYuMTkyNzc3LTQuNjk4MzgxIDYuMzYwMTQ5LTUuMDIxMTcxIDYuMzYwMTQ5LTUuMDU3MDM2QzYuMzYwMTQ5LTUuMDY4OTkxIDYuMzQ4MTk0LTUuMTUyNjc3IDYuMjQwNTk4LTUuMTUyNjc3QzYuMjE2Njg3LTUuMTUyNjc3IDYuMTU2OTEyLTUuMTUyNjc3IDYuMTMzMDAxLTUuMTA0ODU3QzYuMTA5MDkxLTUuMDgwOTQ2IDUuNjkwNjYtNC4yNjc5OTUgNS4zMzIwMDUtMy40NTUwNDRDNS4xNTI2NzctMy4wNDg1NjggNC45MTM1NzQtMi41MTA1ODUgNC41MTkwNTQtMS40NTg1MzFaJy8+CjxwYXRoIGlkPSdnMy02MicgZD0nTTcuODc4NDU2LTIuNzI1Nzc4QzguMTA1NjA0LTIuODMzMzc1IDguMTE3NTU5LTIuOTA1MTA2IDguMTE3NTU5LTIuOTg4NzkyQzguMTE3NTU5LTMuMDYwNTIzIDguMDkzNjQ5LTMuMTQ0MjA5IDcuODc4NDU2LTMuMjM5ODUxTDEuNDEwNzEtNi4yMTY2ODdDMS4yNTUyOTMtNi4yODg0MTggMS4yMzEzODItNi4zMDAzNzQgMS4yMDc0NzItNi4zMDAzNzRDMS4wNjQwMS02LjMwMDM3NCAuOTgwMzI0LTYuMTgwODIyIC45ODAzMjQtNi4wODUxODFDLjk4MDMyNC01Ljk0MTcxOSAxLjA3NTk2NS01Ljg5Mzg5OCAxLjIzMTM4Mi01LjgyMjE2N0w3LjM3NjMzOS0yLjk4ODc5MkwxLjIxOTQyNy0uMTQzNDYyQy45ODAzMjQtLjAzNTg2NiAuOTgwMzI0IC4wNDc4MjEgLjk4MDMyNCAuMTE5NTUyQy45ODAzMjQgLjIxNTE5MyAxLjA2NDAxIC4zMzQ3NDUgMS4yMDc0NzIgLjMzNDc0NUMxLjIzMTM4MiAuMzM0NzQ1IDEuMjQzMzM3IC4zMjI3OSAxLjQxMDcxIC4yNTEwNTlMNy44Nzg0NTYtMi43MjU3NzhaJy8+CjxwYXRoIGlkPSdnMy04MycgZD0nTTcuNTkxNTMyLTguMzA4ODQyQzcuNTkxNTMyLTguNDE2NDM4IDcuNTA3ODQ2LTguNDE2NDM4IDcuNDgzOTM1LTguNDE2NDM4QzcuNDM2MTE1LTguNDE2NDM4IDcuNDI0MTU5LTguNDA0NDgzIDcuMjgwNjk3LTguMjI1MTU2QzcuMjA4OTY2LTguMTQxNDY5IDYuNzE4ODA0LTcuNTE5ODAxIDYuNzA2ODQ5LTcuNTA3ODQ2QzYuMzEyMzI5LTguMjg0OTMyIDUuNTIzMjg4LTguNDE2NDM4IDUuMDIxMTcxLTguNDE2NDM4QzMuNTAyODY0LTguNDE2NDM4IDIuMTI4MDItNy4wMjk2MzkgMi4xMjgwMi01LjY3ODcwNUMyLjEyODAyLTQuNzgyMDY3IDIuNjY2MDAyLTQuMjU2MDQgMy4yNTE4MDYtNC4wNTI4MDJDMy4zODMzMTMtNC4wMDQ5ODEgNC4wODg2NjctMy44MTM2OTkgNC40NDczMjMtMy43MzAwMTJDNS4wNTcwMzYtMy41NjI2NCA1LjIxMjQ1My0zLjUxNDgxOSA1LjQ2MzUxMi0zLjI1MTgwNkM1LjUxMTMzMy0zLjE5MjAzIDUuNzUwNDM2LTIuOTE3MDYxIDUuNzUwNDM2LTIuMzU1MTY4QzUuNzUwNDM2LTEuMjQzMzM3IDQuNzIyMjkxLS4wOTU2NDEgMy41MjY3NzUtLjA5NTY0MUMyLjU0NjQ1MS0uMDk1NjQxIDEuNDU4NTMxLS41MTQwNzIgMS40NTg1MzEtMS44NTMwNTFDMS40NTg1MzEtMi4wODAxOTkgMS41MDYzNTEtMi4zNjcxMjMgMS41NDIyMTctMi40ODY2NzVDMS41NDIyMTctMi41MjI1NCAxLjU1NDE3Mi0yLjU4MjMxNiAxLjU1NDE3Mi0yLjYwNjIyN0MxLjU1NDE3Mi0yLjY1NDA0NyAxLjUzMDI2Mi0yLjcxMzgyMyAxLjQzNDYyLTIuNzEzODIzQzEuMzI3MDI0LTIuNzEzODIzIDEuMzE1MDY4LTIuNjg5OTEzIDEuMjY3MjQ4LTIuNDg2Njc1TC42NTc1MzQtLjAzNTg2NkMuNjU3NTM0LS4wMjM5MSAuNjA5NzE0IC4xMzE1MDcgLjYwOTcxNCAuMTQzNDYyQy42MDk3MTQgLjI1MTA1OSAuNzA1MzU1IC4yNTEwNTkgLjcyOTI2NSAuMjUxMDU5Qy43NzcwODYgLjI1MTA1OSAuNzg5MDQxIC4yMzkxMDMgLjkzMjUwMyAuMDU5Nzc2TDEuNDgyNDQxLS42NTc1MzRDMS43NjkzNjUtLjIyNzE0OCAyLjM5MTAzNCAuMjUxMDU5IDMuNTAyODY0IC4yNTEwNTlDNS4wNDUwODEgLjI1MTA1OSA2LjQ1NTc5MS0xLjI0MzMzNyA2LjQ1NTc5MS0yLjczNzczM0M2LjQ1NTc5MS0zLjIzOTg1MSA2LjMzNjIzOS0zLjY4MjE5MiA1Ljg4MTk0My00LjEyNDUzM0M1LjYzMDg4NC00LjM3NTU5MiA1LjQxNTY5MS00LjQzNTM2NyA0LjMxNTgxNi00LjcyMjI5MUMzLjUxNDgxOS00LjkzNzQ4NCAzLjQwNzIyMy00Ljk3MzM1IDMuMTkyMDMtNS4xNjQ2MzNDMi45ODg3OTItNS4zNjc4NyAyLjgzMzM3NS01LjY1NDc5NSAyLjgzMzM3NS02LjA2MTI3QzIuODMzMzc1LTcuMDY1NTA0IDMuODQ5NTY0LTguMDkzNjQ5IDQuOTg1MzA1LTguMDkzNjQ5QzYuMTU2OTEyLTguMDkzNjQ5IDYuNzA2ODQ5LTcuMzc2MzM5IDYuNzA2ODQ5LTYuMjQwNTk4QzYuNzA2ODQ5LTUuOTI5NzYzIDYuNjQ3MDczLTUuNjA2OTc0IDYuNjQ3MDczLTUuNTU5MTUzQzYuNjQ3MDczLTUuNDUxNTU3IDYuNzQyNzE1LTUuNDUxNTU3IDYuNzc4NTgtNS40NTE1NTdDNi44ODYxNzctNS40NTE1NTcgNi44OTgxMzItNS40ODc0MjIgNi45NDU5NTMtNS42Nzg3MDVMNy41OTE1MzItOC4zMDg4NDJaJy8+CjxwYXRoIGlkPSdnMy04OCcgZD0nTTUuNjc4NzA1LTQuODUzNzk4TDQuNTU0OTE5LTcuNDcxOThDNC43MTAzMzYtNy43NTg5MDQgNS4wNjg5OTEtNy44MDY3MjUgNS4yMTI0NTMtNy44MTg2OEM1LjI4NDE4NC03LjgxODY4IDUuNDE1NjkxLTcuODMwNjM1IDUuNDE1NjkxLTguMDMzODczQzUuNDE1NjkxLTguMTY1MzggNS4zMDgwOTUtOC4xNjUzOCA1LjIzNjM2NC04LjE2NTM4QzUuMDMzMTI2LTguMTY1MzggNC43OTQwMjItOC4xNDE0NjkgNC41OTA3ODUtOC4xNDE0NjlIMy44OTczODVDMy4xNjgxMi04LjE0MTQ2OSAyLjY0MjA5Mi04LjE2NTM4IDIuNjMwMTM3LTguMTY1MzhDMi41MzQ0OTYtOC4xNjUzOCAyLjQxNDk0NC04LjE2NTM4IDIuNDE0OTQ0LTcuOTM4MjMyQzIuNDE0OTQ0LTcuODE4NjggMi41MjI1NC03LjgxODY4IDIuNjc3OTU4LTcuODE4NjhDMy4zNzEzNTctNy44MTg2OCAzLjQxOTE3OC03LjY5OTEyOCAzLjUzODczLTcuNDEyMjA0TDQuOTYxMzk1LTQuMDg4NjY3TDIuMzY3MTIzLTEuMzE1MDY4QzEuOTM2NzM3LS44NDg4MTcgMS40MjI2NjUtLjM5NDUyMSAuNTM3OTgzLS4zNDY3Qy4zOTQ1MjEtLjMzNDc0NSAuMjk4ODc5LS4zMzQ3NDUgLjI5ODg3OS0uMTE5NTUyQy4yOTg4NzktLjA4MzY4NiAuMzEwODM0IDAgLjQ0MjM0MSAwQy42MDk3MTQgMCAuNzg5MDQxLS4wMjM5MSAuOTU2NDEzLS4wMjM5MUgxLjUxODMwNkMxLjkwMDg3Mi0uMDIzOTEgMi4zMTkzMDMgMCAyLjY4OTkxMyAwQzIuNzczNTk5IDAgMi45MTcwNjEgMCAyLjkxNzA2MS0uMjE1MTkzQzIuOTE3MDYxLS4zMzQ3NDUgMi44MzMzNzUtLjM0NjcgMi43NjE2NDQtLjM0NjdDMi41MjI1NC0uMzcwNjEgMi4zNjcxMjMtLjUwMjExNyAyLjM2NzEyMy0uNjkzNEMyLjM2NzEyMy0uODk2NjM4IDIuNTEwNTg1LTEuMDQwMSAyLjg1NzI4NS0xLjM5ODc1NUwzLjkyMTI5NS0yLjU1ODQwNkM0LjE4NDMwOS0yLjgzMzM3NSA0LjgxNzkzMy0zLjUyNjc3NSA1LjA4MDk0Ni0zLjc4OTc4OEw2LjMzNjIzOS0uODQ4ODE3QzYuMzQ4MTk0LS44MjQ5MDcgNi4zOTYwMTUtLjcwNTM1NSA2LjM5NjAxNS0uNjkzNEM2LjM5NjAxNS0uNTg1ODAzIDYuMTMzMDAxLS4zNzA2MSA1Ljc1MDQzNi0uMzQ2N0M1LjY3ODcwNS0uMzQ2NyA1LjU0NzE5OC0uMzM0NzQ1IDUuNTQ3MTk4LS4xMTk1NTJDNS41NDcxOTggMCA1LjY2Njc1IDAgNS43MjY1MjYgMEM1LjkyOTc2MyAwIDYuMTY4ODY3LS4wMjM5MSA2LjM3MjEwNS0uMDIzOTFINy42ODcxNzNDNy45MDIzNjYtLjAyMzkxIDguMTI5NTE0IDAgOC4zMzI3NTIgMEM4LjQxNjQzOCAwIDguNTQ3OTQ1IDAgOC41NDc5NDUtLjIyNzE0OEM4LjU0Nzk0NS0uMzQ2NyA4LjQyODM5NC0uMzQ2NyA4LjMyMDc5Ny0uMzQ2N0M3LjYwMzQ4Ny0uMzU4NjU1IDcuNTc5NTc3LS40MTg0MzEgNy4zNzYzMzktLjg2MDc3Mkw1Ljc5ODI1Ny00LjU2Njg3NEw3LjMxNjU2My02LjE5Mjc3N0M3LjQzNjExNS02LjMxMjMyOSA3LjcxMTA4My02LjYxMTIwOCA3LjgxODY4LTYuNzMwNzZDOC4zMzI3NTItNy4yNjg3NDIgOC44MTA5NTktNy43NTg5MDQgOS43NzkzMjgtNy44MTg2OEM5Ljg5ODg3OS03LjgzMDYzNSAxMC4wMTg0MzEtNy44MzA2MzUgMTAuMDE4NDMxLTguMDMzODczQzEwLjAxODQzMS04LjE2NTM4IDkuOTEwODM0LTguMTY1MzggOS44NjMwMTQtOC4xNjUzOEM5LjY5NTY0MS04LjE2NTM4IDkuNTE2MzE0LTguMTQxNDY5IDkuMzQ4OTQxLTguMTQxNDY5SDguNzk5MDA0QzguNDE2NDM4LTguMTQxNDY5IDcuOTk4MDA3LTguMTY1MzggNy42MjczOTctOC4xNjUzOEM3LjU0MzcxMS04LjE2NTM4IDcuNDAwMjQ5LTguMTY1MzggNy40MDAyNDktNy45NTAxODdDNy40MDAyNDktNy44MzA2MzUgNy40ODM5MzUtNy44MTg2OCA3LjU1NTY2Ni03LjgxODY4QzcuNzQ2OTQ5LTcuNzk0NzcgNy45NTAxODctNy42OTkxMjggNy45NTAxODctNy40NzE5OEw3LjkzODIzMi03LjQ0ODA3QzcuOTI2Mjc2LTcuMzY0Mzg0IDcuOTAyMzY2LTcuMjQ0ODMyIDcuNzcwODU5LTcuMTAxMzdMNS42Nzg3MDUtNC44NTM3OThaJy8+CjxwYXRoIGlkPSdnMy0xMDEnIGQ9J00yLjEzOTk3NS0yLjc3MzU5OUMyLjQ2Mjc2NS0yLjc3MzU5OSAzLjI3NTcxNi0yLjc5NzUwOSAzLjg0OTU2NC0zLjAxMjcwMkM0Ljc1ODE1Ny0zLjM1OTQwMiA0Ljg0MTg0My00LjA1MjgwMiA0Ljg0MTg0My00LjI2Nzk5NUM0Ljg0MTg0My00Ljc5NDAyMiA0LjM4NzU0Ny01LjI3MjIyOSAzLjU5ODUwNi01LjI3MjIyOUMyLjM0MzIxMy01LjI3MjIyOSAuNTM3OTgzLTQuMTM2NDg4IC41Mzc5ODMtMi4wMDg0NjhDLjUzNzk4My0uNzUzMTc2IDEuMjU1MjkzIC4xMTk1NTIgMi4zNDMyMTMgLjExOTU1MkMzLjk2OTExNiAuMTE5NTUyIDQuOTk3MjYtMS4xNDc2OTYgNC45OTcyNi0xLjMwMzExM0M0Ljk5NzI2LTEuMzc0ODQ0IDQuOTI1NTI5LTEuNDM0NjIgNC44Nzc3MDktMS40MzQ2MkM0Ljg0MTg0My0xLjQzNDYyIDQuODI5ODg4LTEuNDIyNjY1IDQuNzIyMjkxLTEuMzE1MDY4QzMuOTU3MTYxLS4yOTg4NzkgMi44MjE0Mi0uMTE5NTUyIDIuMzY3MTIzLS4xMTk1NTJDMS42ODU2NzktLjExOTU1MiAxLjMyNzAyNC0uNjU3NTM0IDEuMzI3MDI0LTEuNTQyMjE3QzEuMzI3MDI0LTEuNzA5NTg5IDEuMzI3MDI0LTIuMDA4NDY4IDEuNTA2MzUxLTIuNzczNTk5SDIuMTM5OTc1Wk0xLjU2NjEyNy0zLjAxMjcwMkMyLjA4MDE5OS00Ljg1Mzc5OCAzLjIxNTk0LTUuMDMzMTI2IDMuNTk4NTA2LTUuMDMzMTI2QzQuMTI0NTMzLTUuMDMzMTI2IDQuNDgzMTg4LTQuNzIyMjkxIDQuNDgzMTg4LTQuMjY3OTk1QzQuNDgzMTg4LTMuMDEyNzAyIDIuNTcwMzYxLTMuMDEyNzAyIDIuMDY4MjQ0LTMuMDEyNzAySDEuNTY2MTI3WicvPgo8cGF0aCBpZD0nZzMtMTA3JyBkPSdNMy4zNTk0MDItNy45OTgwMDdDMy4zNzEzNTctOC4wNDU4MjggMy4zOTUyNjgtOC4xMTc1NTkgMy4zOTUyNjgtOC4xNzczMzVDMy4zOTUyNjgtOC4yOTY4ODcgMy4yNzU3MTYtOC4yOTY4ODcgMy4yNTE4MDYtOC4yOTY4ODdDMy4yMzk4NTEtOC4yOTY4ODcgMi44MDk0NjUtOC4yNjEwMjEgMi41OTQyNzEtOC4yMzcxMTFDMi4zOTEwMzQtOC4yMjUxNTYgMi4yMTE3MDYtOC4yMDEyNDUgMS45OTY1MTMtOC4xODkyOUMxLjcwOTU4OS04LjE2NTM4IDEuNjI1OTAzLTguMTUzNDI1IDEuNjI1OTAzLTcuOTM4MjMyQzEuNjI1OTAzLTcuODE4NjggMS43NDU0NTUtNy44MTg2OCAxLjg2NTAwNi03LjgxODY4QzIuNDc0NzItNy44MTg2OCAyLjQ3NDcyLTcuNzExMDgzIDIuNDc0NzItNy41OTE1MzJDMi40NzQ3Mi03LjU0MzcxMSAyLjQ3NDcyLTcuNTE5ODAxIDIuNDE0OTQ0LTcuMzA0NjA4TC43MDUzNTUtLjQ2NjI1MkMuNjU3NTM0LS4yODY5MjQgLjY1NzUzNC0uMjYzMDE0IC42NTc1MzQtLjE5MTI4M0MuNjU3NTM0IC4wNzE3MzEgLjg2MDc3MiAuMTE5NTUyIC45ODAzMjQgLjExOTU1MkMxLjMxNTA2OCAuMTE5NTUyIDEuMzg2OC0uMTQzNDYyIDEuNDgyNDQxLS41MTQwNzJMMi4wNDQzMzQtMi43NDk2ODlDMi45MDUxMDYtMi42NTQwNDcgMy40MTkxNzgtMi4yOTUzOTIgMy40MTkxNzgtMS43MjE1NDRDMy40MTkxNzgtMS42NDk4MTMgMy40MTkxNzgtMS42MDE5OTMgMy4zODMzMTMtMS40MjI2NjVDMy4zMzU0OTItMS4yNDMzMzcgMy4zMzU0OTItMS4wOTk4NzUgMy4zMzU0OTItMS4wNDAxQzMuMzM1NDkyLS4zNDY3IDMuNzg5Nzg4IC4xMTk1NTIgNC4zOTk1MDIgLjExOTU1MkM0Ljk0OTQ0IC4xMTk1NTIgNS4yMzYzNjQtLjM4MjU2NSA1LjMzMjAwNS0uNTQ5OTM4QzUuNTgzMDY0LS45OTIyNzkgNS43Mzg0ODEtMS42NjE3NjggNS43Mzg0ODEtMS43MDk1ODlDNS43Mzg0ODEtMS43NjkzNjUgNS42OTA2Ni0xLjgxNzE4NiA1LjYxODkyOS0xLjgxNzE4NkM1LjUxMTMzMy0xLjgxNzE4NiA1LjQ5OTM3Ny0xLjc2OTM2NSA1LjQ1MTU1Ny0xLjU3ODA4MkM1LjI4NDE4NC0uOTU2NDEzIDUuMDMzMTI2LS4xMTk1NTIgNC40MjM0MTItLjExOTU1MkM0LjE4NDMwOS0uMTE5NTUyIDQuMDI4ODkyLS4yMzkxMDMgNC4wMjg4OTItLjY5MzRDNC4wMjg4OTItLjkyMDU0OCA0LjA3NjcxMi0xLjE4MzU2MiA0LjEyNDUzMy0xLjM2Mjg4OUM0LjE3MjM1NC0xLjU3ODA4MiA0LjE3MjM1NC0xLjU5MDAzNyA0LjE3MjM1NC0xLjczMzQ5OUM0LjE3MjM1NC0yLjQzODg1NCAzLjUzODczLTIuODMzMzc1IDIuNDM4ODU0LTIuOTc2ODM3QzIuODY5MjQtMy4yMzk4NTEgMy4yOTk2MjYtMy43MDYxMDIgMy40NjY5OTktMy44ODU0M0M0LjE0ODQ0My00LjY1MDU2IDQuNjE0Njk1LTUuMDMzMTI2IDUuMTY0NjMzLTUuMDMzMTI2QzUuNDM5NjAxLTUuMDMzMTI2IDUuNTExMzMzLTQuOTYxMzk1IDUuNTk1MDE5LTQuODg5NjY0QzUuMTUyNjc3LTQuODQxODQzIDQuOTg1MzA1LTQuNTMxMDA5IDQuOTg1MzA1LTQuMjkxOTA1QzQuOTg1MzA1LTQuMDA0OTgxIDUuMjEyNDUzLTMuOTA5MzQgNS4zNzk4MjYtMy45MDkzNEM1LjcwMjYxNS0zLjkwOTM0IDUuOTg5NTM5LTQuMTg0MzA5IDUuOTg5NTM5LTQuNTY2ODc0QzUuOTg5NTM5LTQuOTEzNTc0IDUuNzE0NTctNS4yNzIyMjkgNS4xNzY1ODgtNS4yNzIyMjlDNC41MTkwNTQtNS4yNzIyMjkgMy45ODEwNzEtNC44MDU5NzggMy4xMzIyNTQtMy44NDk1NjRDMy4wMTI3MDItMy43MDYxMDIgMi41NzAzNjEtMy4yNTE4MDYgMi4xMjgwMi0zLjA4NDQzM0wzLjM1OTQwMi03Ljk5ODAwN1onLz4KPHBhdGggaWQ9J2czLTExOScgZD0nTTQuMTEyNTc4LS43MjkyNjVDNC4zNzU1OTItLjAxMTk1NSA1LjExNjgxMiAuMTE5NTUyIDUuNTcxMTA4IC4xMTk1NTJDNi40Nzk3MDEgLjExOTU1MiA3LjAxNzY4NC0uNjY5NDg5IDcuMzUyNDI4LTEuNDk0Mzk2QzcuNjI3Mzk3LTIuMTg3Nzk2IDguMDY5NzM4LTMuNzY1ODc4IDguMDY5NzM4LTQuNDcxMjMzQzguMDY5NzM4LTUuMjAwNDk4IDcuNjk5MTI4LTUuMjcyMjI5IDcuNTkxNTMyLTUuMjcyMjI5QzcuMzA0NjA4LTUuMjcyMjI5IDcuMDQxNTk0LTQuOTg1MzA1IDcuMDQxNTk0LTQuNzQ2MjAyQzcuMDQxNTk0LTQuNjAyNzQgNy4xMjUyOC00LjUxOTA1NCA3LjE4NTA1Ni00LjQ3MTIzM0M3LjI5MjY1My00LjM2MzYzNiA3LjYwMzQ4Ny00LjA0MDg0NyA3LjYwMzQ4Ny0zLjQxOTE3OEM3LjYwMzQ4Ny0zLjAxMjcwMiA3LjI2ODc0Mi0xLjg4ODkxNyA3LjAxNzY4NC0xLjMyNzAyNEM2LjY4MjkzOS0uNTk3NzU4IDYuMjQwNTk4LS4xMTk1NTIgNS42MTg5MjktLjExOTU1MkM0Ljk0OTQ0LS4xMTk1NTIgNC43MzQyNDctLjYyMTY2OSA0LjczNDI0Ny0xLjE3MTYwNkM0LjczNDI0Ny0xLjUxODMwNiA0Ljg0MTg0My0xLjkzNjczNyA0Ljg4OTY2NC0yLjEzOTk3NUw1LjM5MTc4MS00LjE0ODQ0M0M1LjQ1MTU1Ny00LjM4NzU0NyA1LjU1OTE1My00LjgwNTk3OCA1LjU1OTE1My00Ljg1Mzc5OEM1LjU1OTE1My01LjAzMzEyNiA1LjQxNTY5MS01LjE1MjY3NyA1LjIzNjM2NC01LjE1MjY3N0M0Ljg4OTY2NC01LjE1MjY3NyA0LjgwNTk3OC00Ljg1Mzc5OCA0LjczNDI0Ny00LjU2Njg3NEM0LjYxNDY5NS00LjEwMDYyMyA0LjExMjU3OC0yLjA4MDE5OSA0LjA2NDc1Ny0xLjgxNzE4NkM0LjAxNjkzNi0xLjYxMzk0OCA0LjAxNjkzNi0xLjQ4MjQ0MSA0LjAxNjkzNi0xLjIxOTQyN0M0LjAxNjkzNi0uOTMyNTAzIDMuNjM0MzcxLS40NzgyMDcgMy42MjI0MTYtLjQ1NDI5NkMzLjQ5MDkwOS0uMzIyNzkgMy4yOTk2MjYtLjExOTU1MiAyLjkyOTAxNi0uMTE5NTUyQzEuOTg0NTU4LS4xMTk1NTIgMS45ODQ1NTgtMS4wMTYxODkgMS45ODQ1NTgtMS4yMTk0MjdDMS45ODQ1NTgtMS42MDE5OTMgMi4wNjgyNDQtMi4xMjgwMiAyLjYwNjIyNy0zLjU1MDY4NUMyLjc0OTY4OS0zLjkyMTI5NSAyLjgwOTQ2NS00LjA3NjcxMiAyLjgwOTQ2NS00LjMxNTgxNkMyLjgwOTQ2NS00LjgxNzkzMyAyLjQ1MDgwOS01LjI3MjIyOSAxLjg2NTAwNi01LjI3MjIyOUMuNzY1MTMxLTUuMjcyMjI5IC4zMjI3OS0zLjUzODczIC4zMjI3OS0zLjQ0MzA4OEMuMzIyNzktMy4zOTUyNjggLjM3MDYxLTMuMzM1NDkyIC40NTQyOTYtMy4zMzU0OTJDLjU2MTg5My0zLjMzNTQ5MiAuNTczODQ4LTMuMzgzMzEzIC42MjE2NjktMy41NTA2ODVDLjkyMDU0OC00LjYwMjc0IDEuMzg2OC01LjAzMzEyNiAxLjgyOTE0MS01LjAzMzEyNkMxLjk0ODY5Mi01LjAzMzEyNiAyLjEzOTk3NS01LjAyMTE3MSAyLjEzOTk3NS00LjYzODYwNUMyLjEzOTk3NS00LjU3ODgyOSAyLjEzOTk3NS00LjMyNzc3MSAxLjkzNjczNy0zLjgwMTc0M0MxLjM3NDg0NC0yLjMwNzM0NyAxLjI1NTI5My0xLjgxNzE4NiAxLjI1NTI5My0xLjM2Mjg4OUMxLjI1NTI5My0uMTA3NTk3IDIuMjgzNDM3IC4xMTk1NTIgMi44OTMxNTEgLjExOTU1MkMzLjA5NjM4OSAuMTE5NTUyIDMuNjM0MzcxIC4xMTk1NTIgNC4xMTI1NzgtLjcyOTI2NVonLz4KPHBhdGggaWQ9J2c1LTQwJyBkPSdNMy44ODU0MyAyLjkwNTEwNkMzLjg4NTQzIDIuODY5MjQgMy44ODU0MyAyLjg0NTMzIDMuNjgyMTkyIDIuNjQyMDkyQzIuNDg2Njc1IDEuNDM0NjIgMS44MTcxODYtLjUzNzk4MyAxLjgxNzE4Ni0yLjk3NjgzN0MxLjgxNzE4Ni01LjI5NjEzOSAyLjM3OTA3OC03LjI5MjY1MyAzLjc2NTg3OC04LjcwMzM2MkMzLjg4NTQzLTguODEwOTU5IDMuODg1NDMtOC44MzQ4NjkgMy44ODU0My04Ljg3MDczNUMzLjg4NTQzLTguOTQyNDY2IDMuODI1NjU0LTguOTY2Mzc2IDMuNzc3ODMzLTguOTY2Mzc2QzMuNjIyNDE2LTguOTY2Mzc2IDIuNjQyMDkyLTguMTA1NjA0IDIuMDU2Mjg5LTYuOTMzOTk4QzEuNDQ2NTc1LTUuNzI2NTI2IDEuMTcxNjA2LTQuNDQ3MzIzIDEuMTcxNjA2LTIuOTc2ODM3QzEuMTcxNjA2LTEuOTEyODI3IDEuMzM4OTc5LS40OTAxNjIgMS45NjA2NDggLjc4OTA0MUMyLjY2NjAwMiAyLjIyMzY2MSAzLjY0NjMyNiAzLjAwMDc0NyAzLjc3NzgzMyAzLjAwMDc0N0MzLjgyNTY1NCAzLjAwMDc0NyAzLjg4NTQzIDIuOTc2ODM3IDMuODg1NDMgMi45MDUxMDZaJy8+CjxwYXRoIGlkPSdnNS00MScgZD0nTTMuMzcxMzU3LTIuOTc2ODM3QzMuMzcxMzU3LTMuODg1NDMgMy4yNTE4MDYtNS4zNjc4NyAyLjU4MjMxNi02Ljc1NDY3QzEuODc2OTYxLTguMTg5MjkgLjg5NjYzOC04Ljk2NjM3NiAuNzY1MTMxLTguOTY2Mzc2Qy43MTczMS04Ljk2NjM3NiAuNjU3NTM0LTguOTQyNDY2IC42NTc1MzQtOC44NzA3MzVDLjY1NzUzNC04LjgzNDg2OSAuNjU3NTM0LTguODEwOTU5IC44NjA3NzItOC42MDc3MjFDMi4wNTYyODktNy40MDAyNDkgMi43MjU3NzgtNS40Mjc2NDYgMi43MjU3NzgtMi45ODg3OTJDMi43MjU3NzgtLjY2OTQ4OSAyLjE2Mzg4NSAxLjMyNzAyNCAuNzc3MDg2IDIuNzM3NzMzQy42NTc1MzQgMi44NDUzMyAuNjU3NTM0IDIuODY5MjQgLjY1NzUzNCAyLjkwNTEwNkMuNjU3NTM0IDIuOTc2ODM3IC43MTczMSAzLjAwMDc0NyAuNzY1MTMxIDMuMDAwNzQ3Qy45MjA1NDggMy4wMDA3NDcgMS45MDA4NzIgMi4xMzk5NzUgMi40ODY2NzUgLjk2ODM2OUMzLjA5NjM4OS0uMjUxMDU5IDMuMzcxMzU3LTEuNTQyMjE3IDMuMzcxMzU3LTIuOTc2ODM3WicvPgo8cGF0aCBpZD0nZzUtNDMnIGQ9J000Ljc3MDExMi0yLjc2MTY0NEg4LjA2OTczOEM4LjIzNzExMS0yLjc2MTY0NCA4LjQ1MjMwNC0yLjc2MTY0NCA4LjQ1MjMwNC0yLjk3NjgzN0M4LjQ1MjMwNC0zLjIwMzk4NSA4LjI0OTA2Ni0zLjIwMzk4NSA4LjA2OTczOC0zLjIwMzk4NUg0Ljc3MDExMlYtNi41MDM2MTFDNC43NzAxMTItNi42NzA5ODQgNC43NzAxMTItNi44ODYxNzcgNC41NTQ5MTktNi44ODYxNzdDNC4zMjc3NzEtNi44ODYxNzcgNC4zMjc3NzEtNi42ODI5MzkgNC4zMjc3NzEtNi41MDM2MTFWLTMuMjAzOTg1SDEuMDI4MTQ0Qy44NjA3NzItMy4yMDM5ODUgLjY0NTU3OS0zLjIwMzk4NSAuNjQ1NTc5LTIuOTg4NzkyQy42NDU1NzktMi43NjE2NDQgLjg0ODgxNy0yLjc2MTY0NCAxLjAyODE0NC0yLjc2MTY0NEg0LjMyNzc3MVYuNTM3OTgzQzQuMzI3NzcxIC43MDUzNTUgNC4zMjc3NzEgLjkyMDU0OCA0LjU0Mjk2NCAuOTIwNTQ4QzQuNzcwMTEyIC45MjA1NDggNC43NzAxMTIgLjcxNzMxIDQuNzcwMTEyIC41Mzc5ODNWLTIuNzYxNjQ0WicvPgo8cGF0aCBpZD0nZzUtNDknIGQ9J00zLjQ0MzA4OC03LjY2MzI2M0MzLjQ0MzA4OC03LjkzODIzMiAzLjQ0MzA4OC03Ljk1MDE4NyAzLjIwMzk4NS03Ljk1MDE4N0MyLjkxNzA2MS03LjYyNzM5NyAyLjMxOTMwMy03LjE4NTA1NiAxLjA4NzkyLTcuMTg1MDU2Vi02LjgzODM1NkMxLjM2Mjg4OS02LjgzODM1NiAxLjk2MDY0OC02LjgzODM1NiAyLjYxODE4Mi03LjE0OTE5MVYtLjkyMDU0OEMyLjYxODE4Mi0uNDkwMTYyIDIuNTgyMzE2LS4zNDY3IDEuNTMwMjYyLS4zNDY3SDEuMTU5NjUxVjBDMS40ODI0NDEtLjAyMzkxIDIuNjQyMDkyLS4wMjM5MSAzLjAzNjYxMy0uMDIzOTFTNC41Nzg4MjktLjAyMzkxIDQuOTAxNjE5IDBWLS4zNDY3SDQuNTMxMDA5QzMuNDc4OTU0LS4zNDY3IDMuNDQzMDg4LS40OTAxNjIgMy40NDMwODgtLjkyMDU0OFYtNy42NjMyNjNaJy8+CjxwYXRoIGlkPSdnNS01MCcgZD0nTTUuMjYwMjc0LTIuMDA4NDY4SDQuOTk3MjZDNC45NjEzOTUtMS44MDUyMyA0Ljg2NTc1My0xLjE0NzY5NiA0Ljc0NjIwMi0uOTU2NDEzQzQuNjYyNTE2LS44NDg4MTcgMy45ODEwNzEtLjg0ODgxNyAzLjYyMjQxNi0uODQ4ODE3SDEuNDEwNzFDMS43MzM0OTktMS4xMjM3ODYgMi40NjI3NjUtMS44ODg5MTcgMi43NzM1OTktMi4xNzU4NDFDNC41OTA3ODUtMy44NDk1NjQgNS4yNjAyNzQtNC40NzEyMzMgNS4yNjAyNzQtNS42NTQ3OTVDNS4yNjAyNzQtNy4wMjk2MzkgNC4xNzIzNTQtNy45NTAxODcgMi43ODU1NTQtNy45NTAxODdTLjU4NTgwMy02Ljc2NjYyNSAuNTg1ODAzLTUuNzM4NDgxQy41ODU4MDMtNS4xMjg3NjcgMS4xMTE4MzEtNS4xMjg3NjcgMS4xNDc2OTYtNS4xMjg3NjdDMS4zOTg3NTUtNS4xMjg3NjcgMS43MDk1ODktNS4zMDgwOTUgMS43MDk1ODktNS42OTA2NkMxLjcwOTU4OS02LjAyNTQwNSAxLjQ4MjQ0MS02LjI1MjU1MyAxLjE0NzY5Ni02LjI1MjU1M0MxLjA0MDEtNi4yNTI1NTMgMS4wMTYxODktNi4yNTI1NTMgLjk4MDMyNC02LjI0MDU5OEMxLjIwNzQ3Mi03LjA1MzU0OSAxLjg1MzA1MS03LjYwMzQ4NyAyLjYzMDEzNy03LjYwMzQ4N0MzLjY0NjMyNi03LjYwMzQ4NyA0LjI2Nzk5NS02Ljc1NDY3IDQuMjY3OTk1LTUuNjU0Nzk1QzQuMjY3OTk1LTQuNjM4NjA1IDMuNjgyMTkyLTMuNzUzOTIzIDMuMDAwNzQ3LTIuOTg4NzkyTC41ODU4MDMtLjI4NjkyNFYwSDQuOTQ5NDRMNS4yNjAyNzQtMi4wMDg0NjhaJy8+CjxwYXRoIGlkPSdnNS01MScgZD0nTTIuMTk5NzUxLTQuMjkxOTA1QzEuOTk2NTEzLTQuMjc5OTUgMS45NDg2OTItNC4yNjc5OTUgMS45NDg2OTItNC4xNjAzOTlDMS45NDg2OTItNC4wNDA4NDcgMi4wMDg0NjgtNC4wNDA4NDcgMi4yMjM2NjEtNC4wNDA4NDdIMi43NzM1OTlDMy43ODk3ODgtNC4wNDA4NDcgNC4yNDQwODUtMy4yMDM5ODUgNC4yNDQwODUtMi4wNTYyODlDNC4yNDQwODUtLjQ5MDE2MiAzLjQzMTEzMy0uMDcxNzMxIDIuODQ1MzMtLjA3MTczMUMyLjI3MTQ4Mi0uMDcxNzMxIDEuMjkxMTU4LS4zNDY3IC45NDQ0NTgtMS4xMzU3NDFDMS4zMjcwMjQtMS4wNzU5NjUgMS42NzM3MjQtMS4yOTExNTggMS42NzM3MjQtMS43MjE1NDRDMS42NzM3MjQtMi4wNjgyNDQgMS40MjI2NjUtMi4zMDczNDcgMS4wODc5Mi0yLjMwNzM0N0MuODAwOTk2LTIuMzA3MzQ3IC40OTAxNjItMi4xMzk5NzUgLjQ5MDE2Mi0xLjY4NTY3OUMuNDkwMTYyLS42MjE2NjkgMS41NTQxNzIgLjI1MTA1OSAyLjg4MTE5NiAuMjUxMDU5QzQuMzAzODYxIC4yNTEwNTkgNS4zNTU5MTUtLjgzNjg2MiA1LjM1NTkxNS0yLjA0NDMzNEM1LjM1NTkxNS0zLjE0NDIwOSA0LjQ3MTIzMy00LjAwNDk4MSAzLjMyMzUzNy00LjIwODIxOUM0LjM2MzYzNi00LjUwNzA5OCA1LjAzMzEyNi01LjM3OTgyNiA1LjAzMzEyNi02LjMxMjMyOUM1LjAzMzEyNi03LjI1Njc4NyA0LjA1MjgwMi03Ljk1MDE4NyAyLjg5MzE1MS03Ljk1MDE4N0MxLjY5NzYzNC03Ljk1MDE4NyAuODEyOTUxLTcuMjIwOTIyIC44MTI5NTEtNi4zNDgxOTRDLjgxMjk1MS01Ljg2OTk4OCAxLjE4MzU2Mi01Ljc3NDM0NiAxLjM2Mjg4OS01Ljc3NDM0NkMxLjYxMzk0OC01Ljc3NDM0NiAxLjkwMDg3Mi01Ljk1MzY3NCAxLjkwMDg3Mi02LjMxMjMyOUMxLjkwMDg3Mi02LjY5NDg5NCAxLjYxMzk0OC02Ljg2MjI2NyAxLjM1MDkzNC02Ljg2MjI2N0MxLjI3OTIwMy02Ljg2MjI2NyAxLjI1NTI5My02Ljg2MjI2NyAxLjIxOTQyNy02Ljg1MDMxMUMxLjY3MzcyNC03LjY2MzI2MyAyLjc5NzUwOS03LjY2MzI2MyAyLjg1NzI4NS03LjY2MzI2M0MzLjI1MTgwNi03LjY2MzI2MyA0LjAyODg5Mi03LjQ4MzkzNSA0LjAyODg5Mi02LjMxMjMyOUM0LjAyODg5Mi02LjA4NTE4MSAzLjk5MzAyNi01LjQxNTY5MSAzLjY0NjMyNi00LjkwMTYxOUMzLjI4NzY3MS00LjM3NTU5MiAyLjg4MTE5Ni00LjMzOTcyNiAyLjU1ODQwNi00LjMyNzc3MUwyLjE5OTc1MS00LjI5MTkwNVonLz4KPHBhdGggaWQ9J2c1LTYxJyBkPSdNOC4wNjk3MzgtMy44NzM0NzRDOC4yMzcxMTEtMy44NzM0NzQgOC40NTIzMDQtMy44NzM0NzQgOC40NTIzMDQtNC4wODg2NjdDOC40NTIzMDQtNC4zMTU4MTYgOC4yNDkwNjYtNC4zMTU4MTYgOC4wNjk3MzgtNC4zMTU4MTZIMS4wMjgxNDRDLjg2MDc3Mi00LjMxNTgxNiAuNjQ1NTc5LTQuMzE1ODE2IC42NDU1NzktNC4xMDA2MjNDLjY0NTU3OS0zLjg3MzQ3NCAuODQ4ODE3LTMuODczNDc0IDEuMDI4MTQ0LTMuODczNDc0SDguMDY5NzM4Wk04LjA2OTczOC0xLjY0OTgxM0M4LjIzNzExMS0xLjY0OTgxMyA4LjQ1MjMwNC0xLjY0OTgxMyA4LjQ1MjMwNC0xLjg2NTAwNkM4LjQ1MjMwNC0yLjA5MjE1NCA4LjI0OTA2Ni0yLjA5MjE1NCA4LjA2OTczOC0yLjA5MjE1NEgxLjAyODE0NEMuODYwNzcyLTIuMDkyMTU0IC42NDU1NzktMi4wOTIxNTQgLjY0NTU3OS0xLjg3Njk2MUMuNjQ1NTc5LTEuNjQ5ODEzIC44NDg4MTctMS42NDk4MTMgMS4wMjgxNDQtMS42NDk4MTNIOC4wNjk3MzhaJy8+CjxwYXRoIGlkPSdnNS04NicgZD0nTTcuMzA0NjA4LTYuOTgxODE4QzcuNDEyMjA0LTcuMjgwNjk3IDcuNjE1NDQyLTcuODA2NzI1IDguNTQ3OTQ1LTcuODE4NjhWLTguMTY1MzhDNy45MzgyMzItOC4xNDE0NjkgNy45MTQzMjEtOC4xNDE0NjkgNy40NDgwNy04LjE0MTQ2OUM3LjEyNTI4LTguMTQxNDY5IDYuNTI3NTIyLTguMTQxNDY5IDYuMjI4NjQzLTguMTY1MzhWLTcuODE4NjhDNi44MzgzNTYtNy44MDY3MjUgNy4wMTc2ODQtNy40NzE5OCA3LjAxNzY4NC03LjIzMjg3N0M3LjAxNzY4NC03LjE2MTE0NiA3LjAxNzY4NC03LjEzNzIzNSA2Ljk0NTk1My02Ljk2OTg2M0w0LjcxMDMzNi0xLjA3NTk2NUwyLjM1NTE2OC03LjI5MjY1M0MyLjI5NTM5Mi03LjQyNDE1OSAyLjI5NTM5Mi03LjQ0ODA3IDIuMjk1MzkyLTcuNDcxOThDMi4yOTUzOTItNy44MTg2OCAyLjg5MzE1MS03LjgxODY4IDMuMTkyMDMtNy44MTg2OFYtOC4xNjUzOEMyLjkwNTEwNi04LjE0MTQ2OSAxLjk5NjUxMy04LjE0MTQ2OSAxLjY0OTgxMy04LjE0MTQ2OUMxLjMxNTA2OC04LjE0MTQ2OSAuNTAyMTE3LTguMTQxNDY5IC4yMTUxOTMtOC4xNjUzOFYtNy44MTg2OEMuOTU2NDEzLTcuODE4NjggMS4xNDc2OTYtNy44MTg2OCAxLjMyNzAyNC03LjM0MDQ3M0w0LjEyNDUzMyAuMDIzOTFDNC4xODQzMDkgLjE5MTI4MyA0LjIwODIxOSAuMjUxMDU5IDQuMzc1NTkyIC4yNTEwNTlTNC41NTQ5MTkgLjIxNTE5MyA0LjYzODYwNSAuMDExOTU1TDcuMzA0NjA4LTYuOTgxODE4WicvPgo8cGF0aCBpZD0nZzUtOTEnIGQ9J00yLjk4ODc5MiAyLjk4ODc5MlYyLjU0NjQ1MUgxLjgyOTE0MVYtOC41MjQwMzVIMi45ODg3OTJWLTguOTY2Mzc2SDEuMzg2OFYyLjk4ODc5MkgyLjk4ODc5MlonLz4KPHBhdGggaWQ9J2c1LTkzJyBkPSdNMS44NTMwNTEtOC45NjYzNzZILjI1MTA1OVYtOC41MjQwMzVIMS40MTA3MVYyLjU0NjQ1MUguMjUxMDU5VjIuOTg4NzkySDEuODUzMDUxVi04Ljk2NjM3NlonLz4KPHBhdGggaWQ9J2c1LTk3JyBkPSdNNC42MTQ2OTUtMy4xOTIwM0M0LjYxNDY5NS0zLjgzNzYwOSA0LjYxNDY5NS00LjMxNTgxNiA0LjA4ODY2Ny00Ljc4MjA2N0MzLjY3MDIzNy01LjE2NDYzMyAzLjEzMjI1NC01LjMzMjAwNSAyLjYwNjIyNy01LjMzMjAwNUMxLjYyNTkwMy01LjMzMjAwNSAuODcyNzI3LTQuNjg2NDI2IC44NzI3MjctMy45MDkzNEMuODcyNzI3LTMuNTYyNjQgMS4wOTk4NzUtMy4zOTUyNjggMS4zNzQ4NDQtMy4zOTUyNjhDMS42NjE3NjgtMy4zOTUyNjggMS44NjUwMDYtMy41OTg1MDYgMS44NjUwMDYtMy44ODU0M0MxLjg2NTAwNi00LjM3NTU5MiAxLjQzNDYyLTQuMzc1NTkyIDEuMjU1MjkzLTQuMzc1NTkyQzEuNTMwMjYyLTQuODc3NzA5IDIuMTA0MTEtNS4wOTI5MDIgMi41ODIzMTYtNS4wOTI5MDJDMy4xMzIyNTQtNS4wOTI5MDIgMy44Mzc2MDktNC42Mzg2MDUgMy44Mzc2MDktMy41NjI2NFYtMy4wODQ0MzNDMS40MzQ2Mi0zLjA0ODU2OCAuNTI2MDI3LTIuMDQ0MzM0IC41MjYwMjctMS4xMjM3ODZDLjUyNjAyNy0uMTc5MzI4IDEuNjI1OTAzIC4xMTk1NTIgMi4zNTUxNjggLjExOTU1MkMzLjE0NDIwOSAuMTE5NTUyIDMuNjgyMTkyLS4zNTg2NTUgMy45MDkzNC0uOTMyNTAzQzMuOTU3MTYxLS4zNzA2MSA0LjMyNzc3MSAuMDU5Nzc2IDQuODQxODQzIC4wNTk3NzZDNS4wOTI5MDIgLjA1OTc3NiA1Ljc4NjMwMS0uMTA3NTk3IDUuNzg2MzAxLTEuMDY0MDFWLTEuNzMzNDk5SDUuNTIzMjg4Vi0xLjA2NDAxQzUuNTIzMjg4LS4zODI1NjUgNS4yMzYzNjQtLjI4NjkyNCA1LjA2ODk5MS0uMjg2OTI0QzQuNjE0Njk1LS4yODY5MjQgNC42MTQ2OTUtLjkyMDU0OCA0LjYxNDY5NS0xLjA5OTg3NVYtMy4xOTIwM1pNMy44Mzc2MDktMS42ODU2NzlDMy44Mzc2MDktLjUxNDA3MiAyLjk2NDg4Mi0uMTE5NTUyIDIuNDUwODA5LS4xMTk1NTJDMS44NjUwMDYtLjExOTU1MiAxLjM3NDg0NC0uNTQ5OTM4IDEuMzc0ODQ0LTEuMTIzNzg2QzEuMzc0ODQ0LTIuNzAxODY4IDMuNDA3MjIzLTIuODQ1MzMgMy44Mzc2MDktMi44NjkyNFYtMS42ODU2NzlaJy8+CjxwYXRoIGlkPSdnNS0xMDInIGQ9J00yLjA1NjI4OS00LjgwNTk3OEgzLjQwNzIyM1YtNS4xNTI2NzdIMi4wMzIzNzlWLTYuNTUxNDMyQzIuMDMyMzc5LTcuNjI3Mzk3IDIuNTgyMzE2LTguMTc3MzM1IDMuMDcyNDc4LTguMTc3MzM1QzMuMTY4MTItOC4xNzczMzUgMy4zNDc0NDctOC4xNTM0MjUgMy40OTA5MDktOC4wODE2OTRDMy40NDMwODgtOC4wNjk3MzggMy4xNDQyMDktNy45NjIxNDIgMy4xNDQyMDktNy42MTU0NDJDMy4xNDQyMDktNy4zNDA0NzMgMy4zMzU0OTItNy4xNDkxOTEgMy42MTA0NjEtNy4xNDkxOTFDMy44OTczODUtNy4xNDkxOTEgNC4wODg2NjctNy4zNDA0NzMgNC4wODg2NjctNy42MjczOTdDNC4wODg2NjctOC4wNjk3MzggMy42NTgyODEtOC40MTY0MzggMy4wODQ0MzMtOC40MTY0MzhDMi4yNDc1NzItOC40MTY0MzggMS4zMDMxMTMtNy43NzA4NTkgMS4zMDMxMTMtNi41NTE0MzJWLTUuMTUyNjc3SC4zNzA2MVYtNC44MDU5NzhIMS4zMDMxMTNWLS44ODQ2ODJDMS4zMDMxMTMtLjM0NjcgMS4xNzE2MDYtLjM0NjcgLjM5NDUyMS0uMzQ2N1YwQy43MjkyNjUtLjAyMzkxIDEuMzg2OC0uMDIzOTEgMS43NDU0NTUtLjAyMzkxQzIuMDY4MjQ0LS4wMjM5MSAyLjkxNzA2MS0uMDIzOTEgMy4xOTIwMyAwVi0uMzQ2N0gyLjk1MjkyN0MyLjA4MDE5OS0uMzQ2NyAyLjA1NjI4OS0uNDc4MjA3IDIuMDU2Mjg5LS45MDg1OTNWLTQuODA1OTc4WicvPgo8cGF0aCBpZD0nZzUtMTA1JyBkPSdNMi4wODAxOTktNy4zNjQzODRDMi4wODAxOTktNy42NzUyMTggMS44MjkxNDEtNy45NTAxODcgMS40OTQzOTYtNy45NTAxODdDMS4xODM1NjItNy45NTAxODcgLjkyMDU0OC03LjY5OTEyOCAuOTIwNTQ4LTcuMzc2MzM5Qy45MjA1NDgtNy4wMTc2ODQgMS4yMDc0NzItNi43OTA1MzUgMS40OTQzOTYtNi43OTA1MzVDMS44NjUwMDYtNi43OTA1MzUgMi4wODAxOTktNy4xMDEzNyAyLjA4MDE5OS03LjM2NDM4NFpNLjQzMDM4Ni01LjE0MDcyMlYtNC43OTQwMjJDMS4xOTU1MTctNC43OTQwMjIgMS4zMDMxMTMtNC43MjIyOTEgMS4zMDMxMTMtNC4xMzY0ODhWLS44ODQ2ODJDMS4zMDMxMTMtLjM0NjcgMS4xNzE2MDYtLjM0NjcgLjM5NDUyMS0uMzQ2N1YwQy43MjkyNjUtLjAyMzkxIDEuMzAzMTEzLS4wMjM5MSAxLjY0OTgxMy0uMDIzOTFDMS43ODEzMi0uMDIzOTEgMi40NzQ3Mi0uMDIzOTEgMi44ODExOTYgMFYtLjM0NjdDMi4xMDQxMS0uMzQ2NyAyLjA1NjI4OS0uNDA2NDc2IDIuMDU2Mjg5LS44NzI3MjdWLTUuMjcyMjI5TC40MzAzODYtNS4xNDA3MjJaJy8+CjxwYXRoIGlkPSdnNS0xMTQnIGQ9J00xLjk5NjUxMy0yLjc4NTU1NEMxLjk5NjUxMy0zLjk0NTIwNSAyLjQ3NDcyLTUuMDMzMTI2IDMuMzk1MjY4LTUuMDMzMTI2QzMuNDkwOTA5LTUuMDMzMTI2IDMuNTE0ODE5LTUuMDMzMTI2IDMuNTYyNjQtNS4wMjExNzFDMy40NjY5OTktNC45NzMzNSAzLjI3NTcxNi00LjkwMTYxOSAzLjI3NTcxNi00LjU3ODgyOUMzLjI3NTcxNi00LjIzMjEzIDMuNTUwNjg1LTQuMTAwNjIzIDMuNzQxOTY4LTQuMTAwNjIzQzMuOTgxMDcxLTQuMTAwNjIzIDQuMjIwMTc0LTQuMjU2MDQgNC4yMjAxNzQtNC41Nzg4MjlDNC4yMjAxNzQtNC45Mzc0ODQgMy44OTczODUtNS4yNzIyMjkgMy4zODMzMTMtNS4yNzIyMjlDMi4zNjcxMjMtNS4yNzIyMjkgMi4wMjA0MjMtNC4xNzIzNTQgMS45NDg2OTItMy45NDUyMDVIMS45MzY3MzdWLTUuMjcyMjI5TC4zMzQ3NDUtNS4xNDA3MjJWLTQuNzk0MDIyQzEuMTQ3Njk2LTQuNzk0MDIyIDEuMjQzMzM3LTQuNzEwMzM2IDEuMjQzMzM3LTQuMTI0NTMzVi0uODg0NjgyQzEuMjQzMzM3LS4zNDY3IDEuMTExODMxLS4zNDY3IC4zMzQ3NDUtLjM0NjdWMEMuNjY5NDg5LS4wMjM5MSAxLjMyNzAyNC0uMDIzOTEgMS42ODU2NzktLjAyMzkxQzIuMDA4NDY4LS4wMjM5MSAyLjg1NzI4NS0uMDIzOTEgMy4xMzIyNTQgMFYtLjM0NjdIMi44OTMxNTFDMi4wMjA0MjMtLjM0NjcgMS45OTY1MTMtLjQ3ODIwNyAxLjk5NjUxMy0uOTA4NTkzVi0yLjc4NTU1NFonLz4KPHBhdGggaWQ9J2cwLTY5JyBkPSdNMy4wOTYzODktNC4wMTY5MzZDMy4zOTUyNjgtNC4wMTY5MzYgMy45NjkxMTYtNC4wMTY5MzYgNC4zODc1NDctMy43NjU4NzhDNC45NjEzOTUtMy4zOTUyNjggNS4wMDkyMTUtMi43NDk2ODkgNS4wMDkyMTUtMi42Nzc5NThDNS4wMjExNzEtMi41MTA1ODUgNS4wMjExNzEtMi4zNTUxNjggNS4yMjQ0MDgtMi4zNTUxNjhTNS40Mjc2NDYtMi41MjI1NCA1LjQyNzY0Ni0yLjczNzczM1YtNS45Nzc1ODRDNS40Mjc2NDYtNi4xNjg4NjcgNS40Mjc2NDYtNi4zNjAxNDkgNS4yMjQ0MDgtNi4zNjAxNDlTNS4wMDkyMTUtNi4xODA4MjIgNS4wMDkyMTUtNi4wODUxODFDNC45Mzc0ODQtNC41NDI5NjQgMy43MTgwNTctNC40NTkyNzggMy4wOTYzODktNC40NDczMjNWLTYuOTY5ODYzQzMuMDk2Mzg5LTcuNzcwODU5IDMuMzIzNTM3LTcuNzcwODU5IDMuNjEwNDYxLTcuNzcwODU5SDQuMTg0MzA5QzUuNzk4MjU3LTcuNzcwODU5IDYuNTk5MjUzLTYuOTQ1OTUzIDYuNjcwOTg0LTYuMTIxMDQ2QzYuNjgyOTM5LTYuMDI1NDA1IDYuNjk0ODk0LTUuODQ2MDc3IDYuODg2MTc3LTUuODQ2MDc3QzcuMDg5NDE1LTUuODQ2MDc3IDcuMDg5NDE1LTYuMDM3MzYgNy4wODk0MTUtNi4yNDA1OThWLTcuNzk0NzdDNy4wODk0MTUtOC4xNjUzOCA3LjA2NTUwNC04LjE4OTI5IDYuNjk0ODk0LTguMTg5MjlILjU3Mzg0OEMuMzU4NjU1LTguMTg5MjkgLjE2NzM3Mi04LjE4OTI5IC4xNjczNzItNy45NzQwOTdDLjE2NzM3Mi03Ljc3MDg1OSAuMzk0NTIxLTcuNzcwODU5IC40OTAxNjItNy43NzA4NTlDMS4xNzE2MDYtNy43NzA4NTkgMS4yMTk0MjctNy42NzUyMTggMS4yMTk0MjctNy4wODk0MTVWLTEuMDk5ODc1QzEuMjE5NDI3LS41Mzc5ODMgMS4xODM1NjItLjQxODQzMSAuNTQ5OTM4LS40MTg0MzFDLjM3MDYxLS40MTg0MzEgLjE2NzM3Mi0uNDE4NDMxIC4xNjczNzItLjIxNTE5M0MuMTY3MzcyIDAgLjM1ODY1NSAwIC41NzM4NDggMEg2LjkxMDA4N0M3LjEzNzIzNSAwIDcuMjU2Nzg3IDAgNy4yOTI2NTMtLjE2NzM3MkM3LjMwNDYwOC0uMTc5MzI4IDcuNjM5MzUyLTIuMTc1ODQxIDcuNjM5MzUyLTIuMjM1NjE2QzcuNjM5MzUyLTIuMzY3MTIzIDcuNTMxNzU2LTIuNDUwODA5IDcuNDM2MTE1LTIuNDUwODA5QzcuMjY4NzQyLTIuNDUwODA5IDcuMjIwOTIyLTIuMjk1MzkyIDcuMjIwOTIyLTIuMjgzNDM3QzcuMTQ5MTkxLTEuOTcyNjAzIDcuMDI5NjM5LTEuNDcwNDg2IDYuMTU2OTEyLS45NTY0MTNDNS41MzUyNDMtLjU4NTgwMyA0LjkyNTUyOS0uNDE4NDMxIDQuMjY3OTk1LS40MTg0MzFIMy42MTA0NjFDMy4zMjM1MzctLjQxODQzMSAzLjA5NjM4OS0uNDE4NDMxIDMuMDk2Mzg5LTEuMjE5NDI3Vi00LjAxNjkzNlpNNi42NzA5ODQtNy43NzA4NTlWLTcuMTk3MDExQzYuNDY3NzQ2LTcuNDI0MTU5IDYuMjQwNTk4LTcuNjE1NDQyIDUuOTg5NTM5LTcuNzcwODU5SDYuNjcwOTg0Wk00LjMzOTcyNi00LjI2Nzk5NUM0LjUzMTAwOS00LjM1MTY4MSA0Ljc5NDAyMi00LjUzMTAwOSA1LjAwOTIxNS00Ljc4MjA2N1YtMy43Nzc4MzNDNC43MjIyOTEtNC4xMDA2MjMgNC4zNTE2ODEtNC4yNTYwNCA0LjMzOTcyNi00LjI1NjA0Vi00LjI2Nzk5NVpNMS42Mzc4NTgtNy4xMTMzMjVDMS42Mzc4NTgtNy4yNTY3ODcgMS42Mzc4NTgtNy41NTU2NjYgMS41NDIyMTctNy43NzA4NTlIMi44MDk0NjVDMi42Nzc5NTgtNy40OTU4OSAyLjY3Nzk1OC03LjEwMTM3IDIuNjc3OTU4LTYuOTkzNzczVi0xLjE5NTUxN0MyLjY3Nzk1OC0uNzY1MTMxIDIuNzYxNjQ0LS41MjYwMjcgMi44MDk0NjUtLjQxODQzMUgxLjU0MjIxN0MxLjYzNzg1OC0uNjMzNjI0IDEuNjM3ODU4LS45MzI1MDMgMS42Mzc4NTgtMS4wNzU5NjVWLTcuMTEzMzI1Wk02LjA4NTE4MS0uNDE4NDMxVi0uNDMwMzg2QzYuNDY3NzQ2LS42MjE2NjkgNi43OTA1MzUtLjg3MjcyNyA3LjAyOTYzOS0xLjA4NzkyQzcuMDE3Njg0LTEuMDQwMSA2LjkzMzk5OC0uNTE0MDcyIDYuOTIyMDQyLS40MTg0MzFINi4wODUxODFaJy8+CjwvZGVmcz4KPGcgaWQ9J3BhZ2UxJz4KPHVzZSB4PScxMDMuOTk3Nzk1JyB5PSctNzYuOTI4OTg1JyB4bGluazpocmVmPScjZzAtNjknLz4KPHVzZSB4PScxMTMuOTYwNDMxJyB5PSctNzYuOTI4OTg1JyB4bGluazpocmVmPScjZzUtOTEnLz4KPHVzZSB4PScxMTcuMjEyMDkzJyB5PSctNzYuOTI4OTg1JyB4bGluazpocmVmPScjZzMtODgnLz4KPHVzZSB4PScxMjcuODY3MjAxJyB5PSctNzYuOTI4OTg1JyB4bGluazpocmVmPScjZzUtOTMnLz4KPHVzZSB4PScxNDEuMDgxNDc5JyB5PSctNzYuOTI4OTg1JyB4bGluazpocmVmPScjZzUtNjEnLz4KPHVzZSB4PScxNjAuMTQ4NzcxJyB5PSctNzYuOTI4OTg1JyB4bGluazpocmVmPScjZzMtMTMnLz4KPHVzZSB4PScxNjkuNTI3NjYyJyB5PSctNzYuOTI4OTg1JyB4bGluazpocmVmPScjZzUtNDMnLz4KPHVzZSB4PScxOTIuNjE5OTc2JyB5PSctODUuMDE2NzQzJyB4bGluazpocmVmPScjZzMtMTEnLz4KPHJlY3QgeD0nMTgyLjQ4NDQ5MScgeT0nLTgwLjE1Njg3JyBoZWlnaHQ9Jy40NzgxODcnIHdpZHRoPScyNy43OTI2ODknLz4KPHVzZSB4PScxODIuNDg0NDkxJyB5PSctNjguNzI4MzIyJyB4bGluazpocmVmPScjZzMtMTEnLz4KPHVzZSB4PScxOTIuNjYyODc5JyB5PSctNjguNzI4MzIyJyB4bGluazpocmVmPScjZzUtNDMnLz4KPHVzZSB4PScyMDQuNDI0MTk0JyB5PSctNjguNzI4MzIyJyB4bGluazpocmVmPScjZzUtNDknLz4KPHVzZSB4PScyMTEuNDcyNjk0JyB5PSctNzYuOTI4OTg1JyB4bGluazpocmVmPScjZzMtMTInLz4KPHVzZSB4PScyMzQuMzUxOTM5JyB5PSctNzYuOTI4OTg1JyB4bGluazpocmVmPScjZzUtMTA1Jy8+Cjx1c2UgeD0nMjM3LjYwMzYnIHk9Jy03Ni45Mjg5ODUnIHhsaW5rOmhyZWY9JyNnNS0xMDInLz4KPHVzZSB4PScyNDUuMDgyNDIxJyB5PSctNzYuOTI4OTg1JyB4bGluazpocmVmPScjZzMtMTEnLz4KPHVzZSB4PScyNTUuOTI0OTc0JyB5PSctNzYuOTI4OTg1JyB4bGluazpocmVmPScjZzMtNjInLz4KPHVzZSB4PScyNjguMzUwNDU1JyB5PSctNzYuOTI4OTg1JyB4bGluazpocmVmPScjZzUtNDknLz4KPHVzZSB4PSc5My43NjI3NjknIHk9Jy00NC41MTM0NzknIHhsaW5rOmhyZWY9JyNnNS04NicvPgo8dXNlIHg9JzEwMS41NjI2MTgnIHk9Jy00NC41MTM0NzknIHhsaW5rOmhyZWY9JyNnNS05NycvPgo8dXNlIHg9JzEwNy40MTU2MDgnIHk9Jy00NC41MTM0NzknIHhsaW5rOmhyZWY9JyNnNS0xMTQnLz4KPHVzZSB4PScxMTMuOTYwNDInIHk9Jy00NC41MTM0NzknIHhsaW5rOmhyZWY9JyNnNS05MScvPgo8dXNlIHg9JzExNy4yMTIwODEnIHk9Jy00NC41MTM0NzknIHhsaW5rOmhyZWY9JyNnMy04OCcvPgo8dXNlIHg9JzEyNy44NjcxODknIHk9Jy00NC41MTM0NzknIHhsaW5rOmhyZWY9JyNnNS05MycvPgo8dXNlIHg9JzE0MS4wODE0NzknIHk9Jy00NC41MTM0NzknIHhsaW5rOmhyZWY9JyNnNS02MScvPgo8dXNlIHg9JzE3MS41NzY2OTUnIHk9Jy01Mi42MDEyMzgnIHhsaW5rOmhyZWY9JyNnMy0xMScvPgo8cmVjdCB4PScxNjEuMzQ0Mjg0JyB5PSctNDcuNzQxMzY1JyBoZWlnaHQ9Jy40NzgxODcnIHdpZHRoPScyNy45ODY1MjcnLz4KPHVzZSB4PScxNjEuMzQ0Mjg0JyB5PSctMzYuMzEyODE3JyB4bGluazpocmVmPScjZzMtMTEnLz4KPHVzZSB4PScxNzEuNTIyNjcyJyB5PSctMzYuMzEyODE3JyB4bGluazpocmVmPScjZzItMCcvPgo8dXNlIHg9JzE4My40Nzc4MzMnIHk9Jy0zNi4zMTI4MTcnIHhsaW5rOmhyZWY9JyNnNS01MCcvPgo8dXNlIHg9JzE5Mi41MTg4MjMnIHk9Jy02MS4zNzA0MTYnIHhsaW5rOmhyZWY9JyNnMS0xOCcvPgo8dXNlIHg9JzIxMi44NzIzMzcnIHk9Jy01Mi42MDEyMzgnIHhsaW5rOmhyZWY9JyNnMy0xMicvPgo8cmVjdCB4PScyMDIuNTE0NzA5JyB5PSctNDcuNzQxMzY1JyBoZWlnaHQ9Jy40NzgxODcnIHdpZHRoPScyNy45ODY1MjcnLz4KPHVzZSB4PScyMDIuNTE0NzA5JyB5PSctMzYuMzEyODE3JyB4bGluazpocmVmPScjZzMtMTEnLz4KPHVzZSB4PScyMTIuNjkzMDk3JyB5PSctMzYuMzEyODE3JyB4bGluazpocmVmPScjZzItMCcvPgo8dXNlIHg9JzIyNC42NDgyNTcnIHk9Jy0zNi4zMTI4MTcnIHhsaW5rOmhyZWY9JyNnNS00OScvPgo8dXNlIHg9JzIzMS42OTY3NScgeT0nLTYxLjM3MDQxNicgeGxpbms6aHJlZj0nI2cxLTE5Jy8+Cjx1c2UgeD0nMjQwLjQ5NzEyMycgeT0nLTU4LjY5Mzc2MycgeGxpbms6aHJlZj0nI2c0LTUwJy8+Cjx1c2UgeD0nMjYyLjgyOTkwOScgeT0nLTQ0LjUxMzQ3OScgeGxpbms6aHJlZj0nI2c1LTEwNScvPgo8dXNlIHg9JzI2Ni4wODE1NycgeT0nLTQ0LjUxMzQ3OScgeGxpbms6aHJlZj0nI2c1LTEwMicvPgo8dXNlIHg9JzI3My41NjAzOTEnIHk9Jy00NC41MTM0NzknIHhsaW5rOmhyZWY9JyNnMy0xMScvPgo8dXNlIHg9JzI4NC40MDI5NDUnIHk9Jy00NC41MTM0NzknIHhsaW5rOmhyZWY9JyNnMy02MicvPgo8dXNlIHg9JzI5Ni44Mjg0MjYnIHk9Jy00NC41MTM0NzknIHhsaW5rOmhyZWY9JyNnNS01MCcvPgo8dXNlIHg9Jzg1LjQ2MDYyJyB5PSctOS40Mjg5NjYnIHhsaW5rOmhyZWY9JyNnMy04MycvPgo8dXNlIHg9JzkzLjM1NTk0MycgeT0nLTkuNDI4OTY2JyB4bGluazpocmVmPScjZzMtMTA3Jy8+Cjx1c2UgeD0nOTkuODQ1NDQ3JyB5PSctOS40Mjg5NjYnIHhsaW5rOmhyZWY9JyNnMy0xMDEnLz4KPHVzZSB4PScxMDUuMjcwODg3JyB5PSctOS40Mjg5NjYnIHhsaW5rOmhyZWY9JyNnMy0xMTknLz4KPHVzZSB4PScxMTMuOTYwNDI4JyB5PSctOS40Mjg5NjYnIHhsaW5rOmhyZWY9JyNnNS05MScvPgo8dXNlIHg9JzExNy4yMTIwODknIHk9Jy05LjQyODk2NicgeGxpbms6aHJlZj0nI2czLTg4Jy8+Cjx1c2UgeD0nMTI3Ljg2NzE5NycgeT0nLTkuNDI4OTY2JyB4bGluazpocmVmPScjZzUtOTMnLz4KPHVzZSB4PScxNDEuMDgxNDc5JyB5PSctOS40Mjg5NjYnIHhsaW5rOmhyZWY9JyNnNS02MScvPgo8dXNlIHg9JzE2MS4zNDQyODQnIHk9Jy0xNy41MTY3MjUnIHhsaW5rOmhyZWY9JyNnNS01MCcvPgo8dXNlIHg9JzE2Ny4xOTcyNzUnIHk9Jy0xNy41MTY3MjUnIHhsaW5rOmhyZWY9JyNnNS00MCcvPgo8dXNlIHg9JzE3MS43NDk2JyB5PSctMTcuNTE2NzI1JyB4bGluazpocmVmPScjZzUtNDknLz4KPHVzZSB4PScxODAuMjU5MjU0JyB5PSctMTcuNTE2NzI1JyB4bGluazpocmVmPScjZzUtNDMnLz4KPHVzZSB4PScxOTIuMDIwNTY5JyB5PSctMTcuNTE2NzI1JyB4bGluazpocmVmPScjZzMtMTEnLz4KPHVzZSB4PScxOTkuNTQyMjkzJyB5PSctMTcuNTE2NzI1JyB4bGluazpocmVmPScjZzUtNDEnLz4KPHJlY3QgeD0nMTYxLjM0NDI4NCcgeT0nLTEyLjY1Njg1MicgaGVpZ2h0PScuNDc4MTg3JyB3aWR0aD0nNDIuNzUwMzMxJy8+Cjx1c2UgeD0nMTY4LjcyNjE5NCcgeT0nLTEuMjI4MzA0JyB4bGluazpocmVmPScjZzMtMTEnLz4KPHVzZSB4PScxNzguOTA0NTgyJyB5PSctMS4yMjgzMDQnIHhsaW5rOmhyZWY9JyNnMi0wJy8+Cjx1c2UgeD0nMTkwLjg1OTc0MicgeT0nLTEuMjI4MzA0JyB4bGluazpocmVmPScjZzUtNTEnLz4KPHVzZSB4PScyMDUuMjkwMTI5JyB5PSctMjguMjE0NDkzJyB4bGluazpocmVmPScjZzEtMTE0Jy8+CjxyZWN0IHg9JzIxNy4yNDUzMjgnIHk9Jy0yOC42OTI2OCcgaGVpZ2h0PScuNDc4MTg3JyB3aWR0aD0nMzAuMzc3NTU1Jy8+Cjx1c2UgeD0nMjE4LjQ0MDg0MScgeT0nLTE3LjUxNjcyNScgeGxpbms6aHJlZj0nI2czLTExJy8+Cjx1c2UgeD0nMjI4LjYxOTIyOScgeT0nLTE3LjUxNjcyNScgeGxpbms6aHJlZj0nI2cyLTAnLz4KPHVzZSB4PScyNDAuNTc0Mzg5JyB5PSctMTcuNTE2NzI1JyB4bGluazpocmVmPScjZzUtNTAnLz4KPHJlY3QgeD0nMjE4LjQ0MDg0MScgeT0nLTEyLjY1Njg1MicgaGVpZ2h0PScuNDc4MTg3JyB3aWR0aD0nMjcuOTg2NTI3Jy8+Cjx1c2UgeD0nMjI4LjY3MzI1MicgeT0nLTEuMjI4MzA0JyB4bGluazpocmVmPScjZzMtMTEnLz4KPHVzZSB4PScyNjMuMjMwODU2JyB5PSctOS40Mjg5NjYnIHhsaW5rOmhyZWY9JyNnNS0xMDUnLz4KPHVzZSB4PScyNjYuNDgyNTE3JyB5PSctOS40Mjg5NjYnIHhsaW5rOmhyZWY9JyNnNS0xMDInLz4KPHVzZSB4PScyNzMuOTYxMzM4JyB5PSctOS40Mjg5NjYnIHhsaW5rOmhyZWY9JyNnMy0xMScvPgo8dXNlIHg9JzI4NC44MDM4OTInIHk9Jy05LjQyODk2NicgeGxpbms6aHJlZj0nI2czLTYyJy8+Cjx1c2UgeD0nMjk3LjIyOTM3MycgeT0nLTkuNDI4OTY2JyB4bGluazpocmVmPScjZzUtNTEnLz4KPC9nPgo8L3N2Zz4KPCEtLSBERVBUSD0wIC0tPg==)

Examples

Create a distribution:

>>> import openturns as ot >>> distribution = ot.Pareto(1.0, 1.0, 0.0)

Draw a sample:

>>> sample = distribution.getSample(5)

Methods

abs()Transform distribution by absolute value function.

acos()Transform distribution by arccosine function.

acosh()Transform distribution by acosh function.

asin()Transform distribution by arcsine function.

asinh()Transform distribution by asinh function.

atan()Transform distribution by arctangent function.

atanh()Transform distribution by atanh function.

cbrt()Transform distribution by cubic root function.

Compute a bilateral confidence interval.

computeBilateralConfidenceIntervalWithMarginalProbability(prob)Compute a bilateral confidence interval.

computeCDF(*args)Compute the cumulative distribution function.

computeCDFGradient(*args)Compute the gradient of the cumulative distribution function.

Compute the characteristic function.

computeComplementaryCDF(*args)Compute the complementary cumulative distribution function.

computeConditionalCDF(*args)Compute the conditional cumulative distribution function.

computeConditionalDDF(x, y)Compute the conditional derivative density function of the last component.

computeConditionalPDF(*args)Compute the conditional probability density function.

computeConditionalQuantile(*args)Compute the conditional quantile function of the last component.

computeDDF(*args)Compute the derivative density function.

computeDensityGenerator(betaSquare)Compute the probability density function of the characteristic generator.

computeDensityGeneratorDerivative(betaSquare)Compute the first-order derivative of the probability density function.

Compute the second-order derivative of the probability density function.

Compute the entropy of the distribution.

computeGeneratingFunction(*args)Compute the probability-generating function.

Compute the inverse survival function.

Compute the logarithm of the characteristic function.

computeLogGeneratingFunction(*args)Compute the logarithm of the probability-generating function.

computeLogPDF(*args)Compute the logarithm of the probability density function.

computeLogPDFGradient(*args)Compute the gradient of the log probability density function.

Compute the lower extremal dependence coefficients.

Compute the lower tail dependence coefficients.

Compute the confidence interval with minimum volume.

Compute the confidence interval with minimum volume.

Compute the confidence domain with minimum volume.

Compute the confidence domain with minimum volume.

computePDF(*args)Compute the probability density function.

computePDFGradient(*args)Compute the gradient of the probability density function.

computeProbability(interval)Compute the interval probability.

computeQuantile(*args)Compute the quantile function.

computeRadialDistributionCDF(radius[, tail])Compute the cumulative distribution function of the squared radius.

computeScalarQuantile(prob[, tail])Compute the quantile function for univariate distributions.

Compute the sequential conditional cumulative distribution functions.

Compute the sequential conditional derivative density function.

Compute the sequential conditional probability density function.

Compute the conditional quantile function of the last component.

computeSurvivalFunction(*args)Compute the survival function.

computeUnilateralConfidenceInterval(prob[, tail])Compute a unilateral confidence interval.

computeUnilateralConfidenceIntervalWithMarginalProbability(...)Compute a unilateral confidence interval.

Compute the upper extremal dependence coefficients.

Compute the upper tail dependence coefficients.

cos()Transform distribution by cosine function.

cosh()Transform distribution by cosh function.

drawCDF(*args)Draw the cumulative distribution function.

drawLogPDF(*args)Draw the graph or of iso-lines of log-probability density function.

Draw the lower extremal dependence function.

Draw the lower tail dependence function.

drawMarginal1DCDF(marginalIndex, xMin, xMax, ...)Draw the cumulative distribution function of a margin.

drawMarginal1DLogPDF(marginalIndex, xMin, ...)Draw the log-probability density function of a margin.

drawMarginal1DPDF(marginalIndex, xMin, xMax, ...)Draw the probability density function of a margin.

drawMarginal1DSurvivalFunction(...[, logScale])Draw the cumulative distribution function of a margin.

drawMarginal2DCDF(firstMarginal, ...[, ...])Draw the cumulative distribution function of a couple of margins.

drawMarginal2DLogPDF(firstMarginal, ...[, ...])Draw the log-probability density function of a couple of margins.

drawMarginal2DPDF(firstMarginal, ...[, ...])Draw the probability density function of a couple of margins.

drawMarginal2DSurvivalFunction(...[, ...])Draw the cumulative distribution function of a couple of margins.

drawPDF(*args)Draw the graph or of iso-lines of probability density function.

drawQuantile(*args)Draw the quantile function.

drawSurvivalFunction(*args)Draw the cumulative distribution function.

Draw the upper extremal dependence function.

Draw the upper tail dependence function.

exp()Transform distribution by exponential function.

getAlpha()Accessor to the distribution's shape parameter

.getBeta()Accessor to the distribution's scale parameter

.

.Accessor to the CDF computation precision.

Accessor to the componentwise central moments.

Accessor to the Cholesky factor of the covariance matrix.

Accessor to the object's name.

Accessor to the copula of the distribution.

(ditch me?)

Accessor to the covariance matrix.

Accessor to the componentwise description.

Accessor to the dimension of the distribution.

Dispersion indicator accessor.

getGamma()Accessor to the distribution's location parameter

.getId()Accessor to the object's id.

Accessor to the number of Gauss integration points.

Accessor to the inverse Cholesky factor of the covariance matrix.

Accessor to the inverse iso-probabilistic transformation.

Accessor to the iso-probabilistic transformation.

Accessor to the Kendall coefficients matrix.

Accessor to the componentwise kurtosis.

getMarginal(*args)Accessor to marginal distributions.

getMean()Accessor to the mean.

getMoment(n)Accessor to the componentwise moments.

getName()Accessor to the object's name.

Accessor to the PDF computation precision.

Accessor to the parameter of the distribution.

Accessor to the parameter description of the distribution.

Accessor to the number of parameters in the distribution.

Accessor to the parameter of the distribution.

Accessor to the Pearson correlation matrix.

Position indicator accessor.

Accessor to the discrete probability levels.

getRange()Accessor to the range of the distribution.

Accessor to a pseudo-random realization from the distribution.

Accessor to roughness of the distribution.

getSample(size)Accessor to a pseudo-random sample from the distribution.

getSampleByInversion(size)Accessor to a pseudo-random sample from the distribution.

getSampleByQMC(size)Accessor to a low discrepancy sample from the distribution.

Accessor to the object's shadowed id.

Accessor to the shape matrix of the underlying copula if it is elliptical.

getShiftedMoment(n, shift)Accessor to the componentwise shifted moments.

Accessor to the singularities of the PDF function.

Accessor to the componentwise skewness.

Accessor to the Spearman correlation matrix.

Accessor to the componentwise standard deviation.

Accessor to the standard distribution.

Accessor to the standard representative distribution in the parametric family.

getSupport(*args)Accessor to the support of the distribution.

Accessor to the object's visibility state.

Test whether the copula of the distribution is elliptical or not.

Test whether the copula of the distribution is the independent one.

hasName()Test if the object is named.

Test if the object has a distinguishable name.

inverse()Transform distribution by inverse function.

Test whether the distribution is continuous or not.

isCopula()Test whether the distribution is a copula or not.

Test whether the distribution is discrete or not.

Test whether the distribution is elliptical or not.

Test whether the distribution is integer-valued or not.

ln()Transform distribution by natural logarithm function.

log()Transform distribution by natural logarithm function.

setAlpha(alpha)Accessor to the distribution's shape parameter

.setBeta(beta)Accessor to the distribution's scale parameter

.setDescription(description)Accessor to the componentwise description.

setGamma(gamma)Accessor to the distribution's location parameter

.setIntegrationNodesNumber(integrationNodesNumber)Accessor to the number of Gauss integration points.

setName(name)Accessor to the object's name.

setParameter(parameter)Accessor to the parameter of the distribution.

setParametersCollection(*args)Accessor to the parameter of the distribution.

setShadowedId(id)Accessor to the object's shadowed id.

setVisibility(visible)Accessor to the object's visibility state.

sin()Transform distribution by sine function.

sinh()Transform distribution by sinh function.

sqr()Transform distribution by square function.

sqrt()Transform distribution by square root function.

tan()Transform distribution by tangent function.

tanh()Transform distribution by tanh function.

- __init__(*args)¶

- abs()¶

Transform distribution by absolute value function.

- Returns:

- dist

Distribution The transformed distribution.

- dist

- acos()¶

Transform distribution by arccosine function.

- Returns:

- dist

Distribution The transformed distribution.

- dist

- acosh()¶

Transform distribution by acosh function.

- Returns:

- dist

Distribution The transformed distribution.

- dist

- asin()¶

Transform distribution by arcsine function.

- Returns:

- dist

Distribution The transformed distribution.

- dist

- asinh()¶

Transform distribution by asinh function.

- Returns:

- dist

Distribution The transformed distribution.

- dist

- atan()¶

Transform distribution by arctangent function.

- Returns:

- dist

Distribution The transformed distribution.

- dist

- atanh()¶

Transform distribution by atanh function.

- Returns:

- dist

Distribution The transformed distribution.

- dist

- cbrt()¶

Transform distribution by cubic root function.

- Returns:

- dist

Distribution The transformed distribution.

- dist

- computeBilateralConfidenceInterval(prob)¶

Compute a bilateral confidence interval.

- Parameters:

- alphafloat,

![\alpha \in [0,1]](data:image/svg+xml;base64,PD94bWwgdmVyc2lvbj0nMS4wJyBlbmNvZGluZz0nVVRGLTgnPz4KPCEtLSBUaGlzIGZpbGUgd2FzIGdlbmVyYXRlZCBieSBkdmlzdmdtIDMuMS4yIC0tPgo8c3ZnIHZlcnNpb249JzEuMScgeG1sbnM9J2h0dHA6Ly93d3cudzMub3JnLzIwMDAvc3ZnJyB4bWxuczp4bGluaz0naHR0cDovL3d3dy53My5vcmcvMTk5OS94bGluaycgd2lkdGg9JzQ1LjU4Njk4M3B0JyBoZWlnaHQ9JzExLjk1NTE2OHB0JyB2aWV3Qm94PScwIC04Ljk2NjM3NiA0NS41ODY5ODMgMTEuOTU1MTY4Jz4KPGRlZnM+CjxwYXRoIGlkPSdnMi00OCcgZD0nTTUuMzU1OTE1LTMuODI1NjU0QzUuMzU1OTE1LTQuODE3OTMzIDUuMjk2MTM5LTUuNzg2MzAxIDQuODY1NzUzLTYuNjk0ODk0QzQuMzc1NTkyLTcuNjg3MTczIDMuNTE0ODE5LTcuOTUwMTg3IDIuOTI5MDE2LTcuOTUwMTg3QzIuMjM1NjE2LTcuOTUwMTg3IDEuMzg2OC03LjYwMzQ4NyAuOTQ0NDU4LTYuNjExMjA4Qy42MDk3MTQtNS44NTgwMzIgLjQ5MDE2Mi01LjExNjgxMiAuNDkwMTYyLTMuODI1NjU0Qy40OTAxNjItMi42NjYwMDIgLjU3Mzg0OC0xLjc5MzI3NSAxLjAwNDIzNC0uOTQ0NDU4QzEuNDcwNDg2LS4wMzU4NjYgMi4yOTUzOTIgLjI1MTA1OSAyLjkxNzA2MSAuMjUxMDU5QzMuOTU3MTYxIC4yNTEwNTkgNC41NTQ5MTktLjM3MDYxIDQuOTAxNjE5LTEuMDY0MDFDNS4zMzIwMDUtMS45NjA2NDggNS4zNTU5MTUtMy4xMzIyNTQgNS4zNTU5MTUtMy44MjU2NTRaTTIuOTE3MDYxIC4wMTE5NTVDMi41MzQ0OTYgLjAxMTk1NSAxLjc1NzQxLS4yMDMyMzggMS41MzAyNjItMS41MDYzNTFDMS4zOTg3NTUtMi4yMjM2NjEgMS4zOTg3NTUtMy4xMzIyNTQgMS4zOTg3NTUtMy45NjkxMTZDMS4zOTg3NTUtNC45NDk0NCAxLjM5ODc1NS01LjgzNDEyMiAxLjU5MDAzNy02LjUzOTQ3N0MxLjc5MzI3NS03LjM0MDQ3MyAyLjQwMjk4OS03LjcxMTA4MyAyLjkxNzA2MS03LjcxMTA4M0MzLjM3MTM1Ny03LjcxMTA4MyA0LjA2NDc1Ny03LjQzNjExNSA0LjI5MTkwNS02LjQwNzk3QzQuNDQ3MzIzLTUuNzI2NTI2IDQuNDQ3MzIzLTQuNzgyMDY3IDQuNDQ3MzIzLTMuOTY5MTE2QzQuNDQ3MzIzLTMuMTY4MTIgNC40NDczMjMtMi4yNTk1MjcgNC4zMTU4MTYtMS41MzAyNjJDNC4wODg2NjctLjIxNTE5MyAzLjMzNTQ5MiAuMDExOTU1IDIuOTE3MDYxIC4wMTE5NTVaJy8+CjxwYXRoIGlkPSdnMi00OScgZD0nTTMuNDQzMDg4LTcuNjYzMjYzQzMuNDQzMDg4LTcuOTM4MjMyIDMuNDQzMDg4LTcuOTUwMTg3IDMuMjAzOTg1LTcuOTUwMTg3QzIuOTE3MDYxLTcuNjI3Mzk3IDIuMzE5MzAzLTcuMTg1MDU2IDEuMDg3OTItNy4xODUwNTZWLTYuODM4MzU2QzEuMzYyODg5LTYuODM4MzU2IDEuOTYwNjQ4LTYuODM4MzU2IDIuNjE4MTgyLTcuMTQ5MTkxVi0uOTIwNTQ4QzIuNjE4MTgyLS40OTAxNjIgMi41ODIzMTYtLjM0NjcgMS41MzAyNjItLjM0NjdIMS4xNTk2NTFWMEMxLjQ4MjQ0MS0uMDIzOTEgMi42NDIwOTItLjAyMzkxIDMuMDM2NjEzLS4wMjM5MVM0LjU3ODgyOS0uMDIzOTEgNC45MDE2MTkgMFYtLjM0NjdINC41MzEwMDlDMy40Nzg5NTQtLjM0NjcgMy40NDMwODgtLjQ5MDE2MiAzLjQ0MzA4OC0uOTIwNTQ4Vi03LjY2MzI2M1onLz4KPHBhdGggaWQ9J2cyLTkxJyBkPSdNMi45ODg3OTIgMi45ODg3OTJWMi41NDY0NTFIMS44MjkxNDFWLTguNTI0MDM1SDIuOTg4NzkyVi04Ljk2NjM3NkgxLjM4NjhWMi45ODg3OTJIMi45ODg3OTJaJy8+CjxwYXRoIGlkPSdnMi05MycgZD0nTTEuODUzMDUxLTguOTY2Mzc2SC4yNTEwNTlWLTguNTI0MDM1SDEuNDEwNzFWMi41NDY0NTFILjI1MTA1OVYyLjk4ODc5MkgxLjg1MzA1MVYtOC45NjYzNzZaJy8+CjxwYXRoIGlkPSdnMC01MCcgZD0nTTYuNTUxNDMyLTIuNzQ5Njg5QzYuNzU0NjctMi43NDk2ODkgNi45Njk4NjMtMi43NDk2ODkgNi45Njk4NjMtMi45ODg3OTJTNi43NTQ2Ny0zLjIyNzg5NSA2LjU1MTQzMi0zLjIyNzg5NUgxLjQ4MjQ0MUMxLjYyNTkwMy00LjgyOTg4OCAzLjAwMDc0Ny01Ljk3NzU4NCA0LjY4NjQyNi01Ljk3NzU4NEg2LjU1MTQzMkM2Ljc1NDY3LTUuOTc3NTg0IDYuOTY5ODYzLTUuOTc3NTg0IDYuOTY5ODYzLTYuMjE2Njg3UzYuNzU0NjctNi40NTU3OTEgNi41NTE0MzItNi40NTU3OTFINC42NjI1MTZDMi42MTgxODItNi40NTU3OTEgLjk5MjI3OS00LjkwMTYxOSAuOTkyMjc5LTIuOTg4NzkyUzIuNjE4MTgyIC40NzgyMDcgNC42NjI1MTYgLjQ3ODIwN0g2LjU1MTQzMkM2Ljc1NDY3IC40NzgyMDcgNi45Njk4NjMgLjQ3ODIwNyA2Ljk2OTg2MyAuMjM5MTAzUzYuNzU0NjcgMCA2LjU1MTQzMiAwSDQuNjg2NDI2QzMuMDAwNzQ3IDAgMS42MjU5MDMtMS4xNDc2OTYgMS40ODI0NDEtMi43NDk2ODlINi41NTE0MzJaJy8+CjxwYXRoIGlkPSdnMS0xMScgZD0nTTUuNTM1MjQzLTMuMDI0NjU4QzUuNTM1MjQzLTQuMTg0MzA5IDQuODc3NzA5LTUuMjcyMjI5IDMuNjEwNDYxLTUuMjcyMjI5QzIuMDQ0MzM0LTUuMjcyMjI5IC40NzgyMDctMy41NjI2NCAuNDc4MjA3LTEuODY1MDA2Qy40NzgyMDctLjgyNDkwNyAxLjEyMzc4NiAuMTE5NTUyIDIuMzQzMjEzIC4xMTk1NTJDMy4wODQ0MzMgLjExOTU1MiAzLjk2OTExNi0uMTY3MzcyIDQuODE3OTMzLS44ODQ2ODJDNC45ODUzMDUtLjIxNTE5MyA1LjM1NTkxNSAuMTE5NTUyIDUuODY5OTg4IC4xMTk1NTJDNi41MTU1NjcgLjExOTU1MiA2LjgzODM1Ni0uNTQ5OTM4IDYuODM4MzU2LS43MDUzNTVDNi44MzgzNTYtLjgxMjk1MSA2Ljc1NDY3LS44MTI5NTEgNi43MTg4MDQtLjgxMjk1MUM2LjYyMzE2My0uODEyOTUxIDYuNjExMjA4LS43NzcwODYgNi41NzUzNDItLjY4MTQ0NUM2LjQ2Nzc0Ni0uMzgyNTY1IDYuMTkyNzc3LS4xMTk1NTIgNS45MDU4NTMtLjExOTU1MkM1LjUzNTI0My0uMTE5NTUyIDUuNTM1MjQzLS44ODQ2ODIgNS41MzUyNDMtMS42MTM5NDhDNi43NTQ2Ny0zLjA3MjQ3OCA3LjA0MTU5NC00LjU3ODgyOSA3LjA0MTU5NC00LjU5MDc4NUM3LjA0MTU5NC00LjY5ODM4MSA2Ljk0NTk1My00LjY5ODM4MSA2LjkxMDA4Ny00LjY5ODM4MUM2LjgwMjQ5MS00LjY5ODM4MSA2Ljc5MDUzNS00LjY2MjUxNiA2Ljc0MjcxNS00LjQ0NzMyM0M2LjU4NzI5OC0zLjkyMTI5NSA2LjI3NjQ2My0yLjk4ODc5MiA1LjUzNTI0My0yLjAwODQ2OFYtMy4wMjQ2NThaTTQuNzgyMDY3LTEuMTcxNjA2QzMuNzMwMDEyLS4yMjcxNDggMi43ODU1NTQtLjExOTU1MiAyLjM2NzEyMy0uMTE5NTUyQzEuNTE4MzA2LS4xMTk1NTIgMS4yNzkyMDMtLjg3MjcyNyAxLjI3OTIwMy0xLjQzNDYyQzEuMjc5MjAzLTEuOTQ4NjkyIDEuNTQyMjE3LTMuMTY4MTIgMS45MTI4MjctMy44MjU2NTRDMi40MDI5ODktNC42NjI1MTYgMy4wNzI0NzgtNS4wMzMxMjYgMy42MTA0NjEtNS4wMzMxMjZDNC43NzAxMTItNS4wMzMxMjYgNC43NzAxMTItMy41MTQ4MTkgNC43NzAxMTItMi41MTA1ODVDNC43NzAxMTItMi4yMTE3MDYgNC43NTgxNTctMS45MDA4NzIgNC43NTgxNTctMS42MDE5OTNDNC43NTgxNTctMS4zNjI4ODkgNC43NzAxMTItMS4zMDMxMTMgNC43ODIwNjctMS4xNzE2MDZaJy8+CjxwYXRoIGlkPSdnMS01OScgZD0nTTIuMzMxMjU4IC4wNDc4MjFDMi4zMzEyNTgtLjY0NTU3OSAyLjEwNDExLTEuMTU5NjUxIDEuNjEzOTQ4LTEuMTU5NjUxQzEuMjMxMzgyLTEuMTU5NjUxIDEuMDQwMS0uODQ4ODE3IDEuMDQwMS0uNTg1ODAzUzEuMjE5NDI3IDAgMS42MjU5MDMgMEMxLjc4MTMyIDAgMS45MTI4MjctLjA0NzgyMSAyLjAyMDQyMy0uMTU1NDE3QzIuMDQ0MzM0LS4xNzkzMjggMi4wNTYyODktLjE3OTMyOCAyLjA2ODI0NC0uMTc5MzI4QzIuMDkyMTU0LS4xNzkzMjggMi4wOTIxNTQtLjAxMTk1NSAyLjA5MjE1NCAuMDQ3ODIxQzIuMDkyMTU0IC40NDIzNDEgMi4wMjA0MjMgMS4yMTk0MjcgMS4zMjcwMjQgMS45OTY1MTNDMS4xOTU1MTcgMi4xMzk5NzUgMS4xOTU1MTcgMi4xNjM4ODUgMS4xOTU1MTcgMi4xODc3OTZDMS4xOTU1MTcgMi4yNDc1NzIgMS4yNTUyOTMgMi4zMDczNDcgMS4zMTUwNjggMi4zMDczNDdDMS40MTA3MSAyLjMwNzM0NyAyLjMzMTI1OCAxLjQyMjY2NSAyLjMzMTI1OCAuMDQ3ODIxWicvPgo8L2RlZnM+CjxnIGlkPSdwYWdlMSc+Cjx1c2UgeD0nMCcgeT0nMCcgeGxpbms6aHJlZj0nI2cxLTExJy8+Cjx1c2UgeD0nMTAuODQyNTUzJyB5PScwJyB4bGluazpocmVmPScjZzAtNTAnLz4KPHVzZSB4PScyMi4xMzM1MjInIHk9JzAnIHhsaW5rOmhyZWY9JyNnMi05MScvPgo8dXNlIHg9JzI1LjM4NTE4MycgeT0nMCcgeGxpbms6aHJlZj0nI2cyLTQ4Jy8+Cjx1c2UgeD0nMzEuMjM4MTczJyB5PScwJyB4bGluazpocmVmPScjZzEtNTknLz4KPHVzZSB4PSczNi40ODIzMzInIHk9JzAnIHhsaW5rOmhyZWY9JyNnMi00OScvPgo8dXNlIHg9JzQyLjMzNTMyMicgeT0nMCcgeGxpbms6aHJlZj0nI2cyLTkzJy8+CjwvZz4KPC9zdmc+CjwhLS0gREVQVEg9NCAtLT4=)

The confidence level.

- alphafloat,

- Returns:

- confInterval

Interval The confidence interval of level

.

- confInterval

Notes

We consider an absolutely continuous measure

with density function

with density function  .

.The bilateral confidence interval

is the cartesian product

is the cartesian product ![I^*_{\alpha} = [a_1, b_1] \times \dots \times [a_d, b_d]](data:image/svg+xml;base64,PD94bWwgdmVyc2lvbj0nMS4wJyBlbmNvZGluZz0nVVRGLTgnPz4KPCEtLSBUaGlzIGZpbGUgd2FzIGdlbmVyYXRlZCBieSBkdmlzdmdtIDMuMS4yIC0tPgo8c3ZnIHZlcnNpb249JzEuMScgeG1sbnM9J2h0dHA6Ly93d3cudzMub3JnLzIwMDAvc3ZnJyB4bWxuczp4bGluaz0naHR0cDovL3d3dy53My5vcmcvMTk5OS94bGluaycgd2lkdGg9JzEzNC45MzIxODdwdCcgaGVpZ2h0PScxMS45NTUxNjhwdCcgdmlld0JveD0nMCAtOC45NjYzNzYgMTM0LjkzMjE4NyAxMS45NTUxNjgnPgo8ZGVmcz4KPHBhdGggaWQ9J2c0LTQ5JyBkPSdNMi41MDI2MTUtNS4wNzY5NjFDMi41MDI2MTUtNS4yOTIxNTQgMi40ODY2NzUtNS4zMDAxMjUgMi4yNzE0ODItNS4zMDAxMjVDMS45NDQ3MDctNC45ODEzMiAxLjUyMjI5MS00Ljc5MDAzNyAuNzY1MTMxLTQuNzkwMDM3Vi00LjUyNzAyNEMuOTgwMzI0LTQuNTI3MDI0IDEuNDEwNzEtNC41MjcwMjQgMS44NzI5NzYtNC43NDIyMTdWLS42NTM1NDlDMS44NzI5NzYtLjM1ODY1NSAxLjg0OTA2Ni0uMjYzMDE0IDEuMDkxOTA1LS4yNjMwMTRILjgxMjk1MVYwQzEuMTM5NzI2LS4wMjM5MSAxLjgyNTE1Ni0uMDIzOTEgMi4xODM4MTEtLjAyMzkxUzMuMjM1ODY2LS4wMjM5MSAzLjU2MjY0IDBWLS4yNjMwMTRIMy4yODM2ODZDMi41MjY1MjYtLjI2MzAxNCAyLjUwMjYxNS0uMzU4NjU1IDIuNTAyNjE1LS42NTM1NDlWLTUuMDc2OTYxWicvPgo8cGF0aCBpZD0nZzUtNjEnIGQ9J004LjA2OTczOC0zLjg3MzQ3NEM4LjIzNzExMS0zLjg3MzQ3NCA4LjQ1MjMwNC0zLjg3MzQ3NCA4LjQ1MjMwNC00LjA4ODY2N0M4LjQ1MjMwNC00LjMxNTgxNiA4LjI0OTA2Ni00LjMxNTgxNiA4LjA2OTczOC00LjMxNTgxNkgxLjAyODE0NEMuODYwNzcyLTQuMzE1ODE2IC42NDU1NzktNC4zMTU4MTYgLjY0NTU3OS00LjEwMDYyM0MuNjQ1NTc5LTMuODczNDc0IC44NDg4MTctMy44NzM0NzQgMS4wMjgxNDQtMy44NzM0NzRIOC4wNjk3MzhaTTguMDY5NzM4LTEuNjQ5ODEzQzguMjM3MTExLTEuNjQ5ODEzIDguNDUyMzA0LTEuNjQ5ODEzIDguNDUyMzA0LTEuODY1MDA2QzguNDUyMzA0LTIuMDkyMTU0IDguMjQ5MDY2LTIuMDkyMTU0IDguMDY5NzM4LTIuMDkyMTU0SDEuMDI4MTQ0Qy44NjA3NzItMi4wOTIxNTQgLjY0NTU3OS0yLjA5MjE1NCAuNjQ1NTc5LTEuODc2OTYxQy42NDU1NzktMS42NDk4MTMgLjg0ODgxNy0xLjY0OTgxMyAxLjAyODE0NC0xLjY0OTgxM0g4LjA2OTczOFonLz4KPHBhdGggaWQ9J2c1LTkxJyBkPSdNMi45ODg3OTIgMi45ODg3OTJWMi41NDY0NTFIMS44MjkxNDFWLTguNTI0MDM1SDIuOTg4NzkyVi04Ljk2NjM3NkgxLjM4NjhWMi45ODg3OTJIMi45ODg3OTJaJy8+CjxwYXRoIGlkPSdnNS05MycgZD0nTTEuODUzMDUxLTguOTY2Mzc2SC4yNTEwNTlWLTguNTI0MDM1SDEuNDEwNzFWMi41NDY0NTFILjI1MTA1OVYyLjk4ODc5MkgxLjg1MzA1MVYtOC45NjYzNzZaJy8+CjxwYXRoIGlkPSdnMS0xJyBkPSdNMi4yOTUzOTItMi45ODg3OTJDMi4yOTUzOTItMy4zMzU0OTIgMi4wMDg0NjgtMy42MjI0MTYgMS42NjE3NjgtMy42MjI0MTZTMS4wMjgxNDQtMy4zMzU0OTIgMS4wMjgxNDQtMi45ODg3OTJTMS4zMTUwNjgtMi4zNTUxNjggMS42NjE3NjgtMi4zNTUxNjhTMi4yOTUzOTItMi42NDIwOTIgMi4yOTUzOTItMi45ODg3OTJaJy8+CjxwYXRoIGlkPSdnMS0yJyBkPSdNNC42NTA1Ni0zLjMyMzUzN0wyLjI1OTUyNy01LjcwMjYxNUMyLjExNjA2NS01Ljg0NjA3NyAyLjA5MjE1NC01Ljg2OTk4OCAxLjk5NjUxMy01Ljg2OTk4OEMxLjg3Njk2MS01Ljg2OTk4OCAxLjc1NzQxLTUuNzYyMzkxIDEuNzU3NDEtNS42MzA4ODRDMS43NTc0MS01LjU0NzE5OCAxLjc4MTMyLTUuNTIzMjg4IDEuOTEyODI3LTUuMzkxNzgxTDQuMzAzODYxLTIuOTg4NzkyTDEuOTEyODI3LS41ODU4MDNDMS43ODEzMi0uNDU0Mjk2IDEuNzU3NDEtLjQzMDM4NiAxLjc1NzQxLS4zNDY3QzEuNzU3NDEtLjIxNTE5MyAxLjg3Njk2MS0uMTA3NTk3IDEuOTk2NTEzLS4xMDc1OTdDMi4wOTIxNTQtLjEwNzU5NyAyLjExNjA2NS0uMTMxNTA3IDIuMjU5NTI3LS4yNzQ5NjlMNC42Mzg2MDUtMi42NTQwNDdMNy4xMTMzMjUtLjE3OTMyOEM3LjEzNzIzNS0uMTY3MzcyIDcuMjIwOTIyLS4xMDc1OTcgNy4yOTI2NTMtLjEwNzU5N0M3LjQzNjExNS0uMTA3NTk3IDcuNTMxNzU2LS4yMTUxOTMgNy41MzE3NTYtLjM0NjdDNy41MzE3NTYtLjM3MDYxIDcuNTMxNzU2LS40MTg0MzEgNy40OTU4OS0uNDc4MjA3QzcuNDgzOTM1LS41MDIxMTcgNS41ODMwNjQtMi4zNzkwNzggNC45ODUzMDUtMi45ODg3OTJMNy4xNzMxMDEtNS4xNzY1ODhDNy4yMzI4NzctNS4yNDgzMTkgNy40MTIyMDQtNS40MDM3MzYgNy40NzE5OC01LjQ3NTQ2N0M3LjQ4MzkzNS01LjQ5OTM3NyA3LjUzMTc1Ni01LjU0NzE5OCA3LjUzMTc1Ni01LjYzMDg4NEM3LjUzMTc1Ni01Ljc2MjM5MSA3LjQzNjExNS01Ljg2OTk4OCA3LjI5MjY1My01Ljg2OTk4OEM3LjE5NzAxMS01Ljg2OTk4OCA3LjE0OTE5MS01LjgyMjE2NyA3LjAxNzY4NC01LjY5MDY2TDQuNjUwNTYtMy4zMjM1MzdaJy8+CjxwYXRoIGlkPSdnMi0xMScgZD0nTTQuMDY0NzU3LTEuMTE1ODE2QzQuODA1OTc4LTEuOTI4NzY3IDUuMDY4OTkxLTIuOTY0ODgyIDUuMDY4OTkxLTMuMDI4NjQzQzUuMDY4OTkxLTMuMTAwMzc0IDUuMDIxMTcxLTMuMTMyMjU0IDQuOTQ5NDQtMy4xMzIyNTRDNC44NDU4MjgtMy4xMzIyNTQgNC44Mzc4NTgtMy4xMDAzNzQgNC43OTAwMzctMi45MzMwMDFDNC41NjY4NzQtMi4xMjAwNSA0LjA4ODY2Ny0xLjQ5ODM4MSA0LjA2NDc1Ny0xLjQ5ODM4MUM0LjA0ODgxNy0xLjQ5ODM4MSA0LjA0ODgxNy0xLjY5NzYzNCA0LjA0ODgxNy0xLjgyNTE1NkM0LjAzMjg3Ny0zLjIyNzg5NSAzLjEyNDI4NC0zLjUxNDgxOSAyLjU4MjMxNi0zLjUxNDgxOUMxLjQ1ODUzMS0zLjUxNDgxOSAuMzUwNjg1LTIuNDIyOTE0IC4zNTA2ODUtMS4yOTkxMjhDLjM1MDY4NS0uNTEwMDg3IC45MDA2MjMgLjA3OTcwMSAxLjc0NTQ1NSAuMDc5NzAxQzIuMzAzMzYyIC4wNzk3MDEgMi44OTMxNTEtLjExOTU1MiAzLjUyMjc5LS41ODk3ODhDMy42OTgxMzIgLjAzOTg1MSA0LjE2MDM5OSAuMDc5NzAxIDQuMzAzODYxIC4wNzk3MDFDNC43NTgxNTcgLjA3OTcwMSA1LjAyMTE3MS0uMzI2Nzc1IDUuMDIxMTcxLS40NzgyMDdDNS4wMjExNzEtLjU3Mzg0OCA0LjkyNTUyOS0uNTczODQ4IDQuOTAxNjE5LS41NzM4NDhDNC44MTM5NDgtLjU3Mzg0OCA0Ljc5ODAwNy0uNTQ5OTM4IDQuNzc0MDk3LS40OTQxNDdDNC42NDY1NzUtLjE1OTQwMiA0LjM3NTU5Mi0uMTQzNDYyIDQuMzM1NzQxLS4xNDM0NjJDNC4yMjQxNTktLjE0MzQ2MiA0LjA5NjYzOC0uMTQzNDYyIDQuMDY0NzU3LTEuMTE1ODE2Wk0zLjQ2Njk5OS0uODUyODAyQzIuOTAxMTIxLS4zNDI3MTUgMi4yMzE2MzEtLjE0MzQ2MiAxLjc2OTM2NS0uMTQzNDYyQzEuMzU0OTE5LS4xNDM0NjIgLjk5NjI2NC0uMzgyNTY1IC45OTYyNjQtMS4wMjAxNzRDLjk5NjI2NC0xLjI5OTEyOCAxLjEyMzc4Ni0yLjEyMDA1IDEuNDk4MzgxLTIuNjU0MDQ3QzEuODE3MTg2LTMuMTAwMzc0IDIuMjQ3NTcyLTMuMjkxNjU2IDIuNTc0MzQ2LTMuMjkxNjU2QzMuMDEyNzAyLTMuMjkxNjU2IDMuMjU5Nzc2LTIuOTgwODIyIDMuMzYzMzg3LTIuNDk0NjQ1QzMuNDgyOTM5LTEuOTUyNjc3IDMuNDE5MTc4LTEuMzE1MDY4IDMuNDY2OTk5LS44NTI4MDJaJy8+CjxwYXRoIGlkPSdnMi0xMDAnIGQ9J000LjI4NzkyLTUuMjkyMTU0QzQuMjk1ODktNS4zMDgwOTUgNC4zMTk4MDEtNS40MTE3MDYgNC4zMTk4MDEtNS40MTk2NzZDNC4zMTk4MDEtNS40NTk1MjcgNC4yODc5Mi01LjUzMTI1OCA0LjE5MjI3OS01LjUzMTI1OEM0LjE2MDM5OS01LjUzMTI1OCAzLjkxMzMyNS01LjUwNzM0NyAzLjczMDAxMi01LjQ5MTQwN0wzLjI4MzY4Ni01LjQ1OTUyN0MzLjEwODM0NC01LjQ0MzU4NyAzLjAyODY0My01LjQzNTYxNiAzLjAyODY0My01LjI5MjE1NEMzLjAyODY0My01LjE4MDU3MyAzLjE0MDIyNC01LjE4MDU3MyAzLjIzNTg2Ni01LjE4MDU3M0MzLjYxODQzMS01LjE4MDU3MyAzLjYxODQzMS01LjEzMjc1MiAzLjYxODQzMS01LjA2MTAyMUMzLjYxODQzMS01LjAxMzIgMy41NTQ2Ny00Ljc1MDE4NyAzLjUxNDgxOS00LjU5MDc4NUwzLjEyNDI4NC0zLjAzNjYxM0MzLjA1MjU1My0zLjE3MjEwNSAyLjgyMTQyLTMuNTE0ODE5IDIuMzM1MjQzLTMuNTE0ODE5QzEuMzg2OC0zLjUxNDgxOSAuMzQyNzE1LTIuNDA2OTc0IC4zNDI3MTUtMS4yMjczOTdDLjM0MjcxNS0uMzk4NTA2IC44NzY3MTIgLjA3OTcwMSAxLjQ5MDQxMSAuMDc5NzAxQzIuMDAwNDk4IC4wNzk3MDEgMi40Mzg4NTQtLjMyNjc3NSAyLjU4MjMxNi0uNDg2MTc3QzIuNzI1Nzc4IC4wNjM3NjEgMy4yNjc3NDYgLjA3OTcwMSAzLjM2MzM4NyAuMDc5NzAxQzMuNzMwMDEyIC4wNzk3MDEgMy45MTMzMjUtLjIyMzE2MyAzLjk3NzA4Ni0uMzU4NjU1QzQuMTM2NDg4LS42NDU1NzkgNC4yNDgwNy0xLjEwNzg0NiA0LjI0ODA3LTEuMTM5NzI2QzQuMjQ4MDctMS4xODc1NDcgNC4yMTYxODktMS4yNDMzMzcgNC4xMjA1NDgtMS4yNDMzMzdTNC4wMDg5NjYtMS4xOTU1MTcgMy45NjExNDYtLjk5NjI2NEMzLjg0OTU2NC0uNTU3OTA4IDMuNjk4MTMyLS4xNDM0NjIgMy4zODcyOTgtLjE0MzQ2MkMzLjIwMzk4NS0uMTQzNDYyIDMuMTMyMjU0LS4yOTQ4OTQgMy4xMzIyNTQtLjUxODA1N0MzLjEzMjI1NC0uNjY5NDg5IDMuMTU2MTY0LS43NTcxNjEgMy4xODAwNzUtLjg2MDc3Mkw0LjI4NzkyLTUuMjkyMTU0Wk0yLjU4MjMxNi0uODYwNzcyQzIuMTgzODExLS4zMTA4MzQgMS43NjkzNjUtLjE0MzQ2MiAxLjUxNDMyMS0uMTQzNDYyQzEuMTQ3Njk2LS4xNDM0NjIgLjk2NDM4NC0uNDc4MjA3IC45NjQzODQtLjg5MjY1M0MuOTY0Mzg0LTEuMjY3MjQ4IDEuMTc5NTc3LTIuMTIwMDUgMS4zNTQ5MTktMi40NzA3MzVDMS41ODYwNTItMi45NTY5MTIgMS45NzY1ODgtMy4yOTE2NTYgMi4zNDMyMTMtMy4yOTE2NTZDMi44NjEyNy0zLjI5MTY1NiAzLjAxMjcwMi0yLjcwOTgzOCAzLjAxMjcwMi0yLjYxNDE5N0MzLjAxMjcwMi0yLjU4MjMxNiAyLjgxMzQ1LTEuODAxMjQ1IDIuNzY1NjI5LTEuNTk0MDIyQzIuNjYyMDE3LTEuMjE5NDI3IDIuNjYyMDE3LTEuMjAzNDg3IDIuNTgyMzE2LS44NjA3NzJaJy8+CjxwYXRoIGlkPSdnMC0zJyBkPSdNMy4yOTE2NTYtMS4wNTIwNTVDMy4zNjMzODctMS4wMDQyMzQgMy4zODcyOTgtMS4wMDQyMzQgMy40MjcxNDgtMS4wMDQyMzRDMy41NTQ2Ny0xLjAwNDIzNCAzLjY2NjI1Mi0xLjEwNzg0NiAzLjY2NjI1Mi0xLjI1MTMwOEMzLjY2NjI1Mi0xLjQwMjc0IDMuNTg2NTUtMS40MzQ2MiAzLjQ2Njk5OS0xLjQ5MDQxMUMyLjkzMzAwMS0xLjczNzQ4NCAyLjc0MTcxOS0xLjgyNTE1NiAyLjM1MTE4My0xLjk4NDU1OEwzLjI4MzY4Ni0yLjQwNjk3NEMzLjM0NzQ0Ny0yLjQzMDg4NCAzLjQ5ODg3OS0yLjUwMjYxNSAzLjU2MjY0LTIuNTI2NTI2QzMuNjQyMzQxLTIuNTc0MzQ2IDMuNjY2MjUyLTIuNjU0MDQ3IDMuNjY2MjUyLTIuNzI1Nzc4QzMuNjY2MjUyLTIuODIxNDIgMy42MTg0MzEtMi45NzI4NTIgMy4zNzkzMjgtMi45NzI4NTJMMi4yMzE2MzEtMi4xOTE3ODFMMi4zNDMyMTMtMy4zNzEzNTdDMi4zNTkxNTMtMy41MDY4NDkgMi4zNDMyMTMtMy43MDYxMDIgMi4xMTIwOC0zLjcwNjEwMkMxLjk2ODYxOC0zLjcwNjEwMiAxLjg1NzAzNi0zLjU4NjU1IDEuODgwOTQ2LTMuNDc0OTY5Vi0zLjM3OTMyOEwxLjk5MjUyOC0yLjE5MTc4MUwuOTMyNTAzLTIuOTI1MDMxQy44NjA3NzItMi45NzI4NTIgLjgzNjg2Mi0yLjk3Mjg1MiAuNzk3MDExLTIuOTcyODUyQy42Njk0ODktMi45NzI4NTIgLjU1NzkwOC0yLjg2OTI0IC41NTc5MDgtMi43MjU3NzhDLjU1NzkwOC0yLjU3NDM0NiAuNjM3NjA5LTIuNTQyNDY2IC43NTcxNjEtMi40ODY2NzVDMS4yOTExNTgtMi4yMzk2MDEgMS40ODI0NDEtMi4xNTE5MyAxLjg3Mjk3Ni0xLjk5MjUyOEwuOTQwNDczLTEuNTcwMTEyQy44NzY3MTItMS41NDYyMDIgLjcyNTI4LTEuNDc0NDcxIC42NjE1MTktMS40NTA1NkMuNTgxODE4LTEuNDAyNzQgLjU1NzkwOC0xLjMyMzAzOSAuNTU3OTA4LTEuMjUxMzA4Qy41NTc5MDgtMS4xMDc4NDYgLjY2OTQ4OS0xLjAwNDIzNCAuNzk3MDExLTEuMDA0MjM0Qy44NjA3NzItMS4wMDQyMzQgLjg3NjcxMi0xLjAwNDIzNCAxLjA3NTk2NS0xLjE0NzY5NkwxLjk5MjUyOC0xLjc4NTMwNUwxLjg3Mjk3Ni0uNTAyMTE3QzEuODcyOTc2LS4zNDI3MTUgMi4wMDg0NjgtLjI3MDk4NCAyLjExMjA4LS4yNzA5ODRTMi4zNTExODMtLjM0MjcxNSAyLjM1MTE4My0uNTAyMTE3QzIuMzUxMTgzLS41ODE4MTggMi4zMTkzMDMtLjgzNjg2MiAyLjMxMTMzMy0uOTMyNTAzQzIuMjc5NDUyLTEuMjAzNDg3IDIuMjU1NTQyLTEuNTA2MzUxIDIuMjMxNjMxLTEuNzg1MzA1TDMuMjkxNjU2LTEuMDUyMDU1WicvPgo8cGF0aCBpZD0nZzMtNTknIGQ9J00yLjMzMTI1OCAuMDQ3ODIxQzIuMzMxMjU4LS42NDU1NzkgMi4xMDQxMS0xLjE1OTY1MSAxLjYxMzk0OC0xLjE1OTY1MUMxLjIzMTM4Mi0xLjE1OTY1MSAxLjA0MDEtLjg0ODgxNyAxLjA0MDEtLjU4NTgwM1MxLjIxOTQyNyAwIDEuNjI1OTAzIDBDMS43ODEzMiAwIDEuOTEyODI3LS4wNDc4MjEgMi4wMjA0MjMtLjE1NTQxN0MyLjA0NDMzNC0uMTc5MzI4IDIuMDU2Mjg5LS4xNzkzMjggMi4wNjgyNDQtLjE3OTMyOEMyLjA5MjE1NC0uMTc5MzI4IDIuMDkyMTU0LS4wMTE5NTUgMi4wOTIxNTQgLjA0NzgyMUMyLjA5MjE1NCAuNDQyMzQxIDIuMDIwNDIzIDEuMjE5NDI3IDEuMzI3MDI0IDEuOTk2NTEzQzEuMTk1NTE3IDIuMTM5OTc1IDEuMTk1NTE3IDIuMTYzODg1IDEuMTk1NTE3IDIuMTg3Nzk2QzEuMTk1NTE3IDIuMjQ3NTcyIDEuMjU1MjkzIDIuMzA3MzQ3IDEuMzE1MDY4IDIuMzA3MzQ3QzEuNDEwNzEgMi4zMDczNDcgMi4zMzEyNTggMS40MjI2NjUgMi4zMzEyNTggLjA0NzgyMVonLz4KPHBhdGggaWQ9J2czLTczJyBkPSdNNC4zOTk1MDItNy4yODA2OTdDNC41MDcwOTgtNy42OTkxMjggNC41MzEwMDktNy44MTg2OCA1LjQwMzczNi03LjgxODY4QzUuNjY2NzUtNy44MTg2OCA1Ljc2MjM5MS03LjgxODY4IDUuNzYyMzkxLTguMDQ1ODI4QzUuNzYyMzkxLTguMTY1MzggNS42MzA4ODQtOC4xNjUzOCA1LjU5NTAxOS04LjE2NTM4QzUuMzc5ODI2LTguMTY1MzggNS4xMTY4MTItOC4xNDE0NjkgNC45MDE2MTktOC4xNDE0NjlIMy40MzExMzNDMy4xOTIwMy04LjE0MTQ2OSAyLjkxNzA2MS04LjE2NTM4IDIuNjc3OTU4LTguMTY1MzhDMi41ODIzMTYtOC4xNjUzOCAyLjQ1MDgwOS04LjE2NTM4IDIuNDUwODA5LTcuOTM4MjMyQzIuNDUwODA5LTcuODE4NjggMi41NDY0NTEtNy44MTg2OCAyLjc4NTU1NC03LjgxODY4QzMuNTI2Nzc1LTcuODE4NjggMy41MjY3NzUtNy43MjMwMzkgMy41MjY3NzUtNy41OTE1MzJDMy41MjY3NzUtNy41MDc4NDYgMy41MDI4NjQtNy40MzYxMTUgMy40Nzg5NTQtNy4zMjg1MThMMS44NjUwMDYtLjg4NDY4MkMxLjc1NzQxLS40NjYyNTIgMS43MzM0OTktLjM0NjcgLjg2MDc3Mi0uMzQ2N0MuNTk3NzU4LS4zNDY3IC40OTAxNjItLjM0NjcgLjQ5MDE2Mi0uMTE5NTUyQy40OTAxNjIgMCAuNjA5NzE0IDAgLjY2OTQ4OSAwQy44ODQ2ODIgMCAxLjE0NzY5Ni0uMDIzOTEgMS4zNjI4ODktLjAyMzkxSDIuODMzMzc1QzMuMDcyNDc4LS4wMjM5MSAzLjMzNTQ5MiAwIDMuNTc0NTk1IDBDMy42NzAyMzcgMCAzLjgxMzY5OSAwIDMuODEzNjk5LS4yMTUxOTNDMy44MTM2OTktLjM0NjcgMy43NDE5NjgtLjM0NjcgMy40Nzg5NTQtLjM0NjdDMi43Mzc3MzMtLjM0NjcgMi43Mzc3MzMtLjQ0MjM0MSAyLjczNzczMy0uNTg1ODAzQzIuNzM3NzMzLS42MDk3MTQgMi43Mzc3MzMtLjY2OTQ4OSAyLjc4NTU1NC0uODYwNzcyTDQuMzk5NTAyLTcuMjgwNjk3WicvPgo8cGF0aCBpZD0nZzMtOTcnIGQ9J00zLjU5ODUwNi0xLjQyMjY2NUMzLjUzODczLTEuMjE5NDI3IDMuNTM4NzMtMS4xOTU1MTcgMy4zNzEzNTctLjk2ODM2OUMzLjEwODM0NC0uNjMzNjI0IDIuNTgyMzE2LS4xMTk1NTIgMi4wMjA0MjMtLjExOTU1MkMxLjUzMDI2Mi0uMTE5NTUyIDEuMjU1MjkzLS41NjE4OTMgMS4yNTUyOTMtMS4yNjcyNDhDMS4yNTUyOTMtMS45MjQ3ODIgMS42MjU5MDMtMy4yNjM3NjEgMS44NTMwNTEtMy43NjU4NzhDMi4yNTk1MjctNC42MDI3NCAyLjgyMTQyLTUuMDMzMTI2IDMuMjg3NjcxLTUuMDMzMTI2QzQuMDc2NzEyLTUuMDMzMTI2IDQuMjMyMTMtNC4wNTI4MDIgNC4yMzIxMy0zLjk1NzE2MUM0LjIzMjEzLTMuOTQ1MjA1IDQuMTk2MjY0LTMuNzg5Nzg4IDQuMTg0MzA5LTMuNzY1ODc4TDMuNTk4NTA2LTEuNDIyNjY1Wk00LjM2MzYzNi00LjQ4MzE4OEM0LjIzMjEzLTQuNzk0MDIyIDMuOTA5MzQtNS4yNzIyMjkgMy4yODc2NzEtNS4yNzIyMjlDMS45MzY3MzctNS4yNzIyMjkgLjQ3ODIwNy0zLjUyNjc3NSAuNDc4MjA3LTEuNzU3NDFDLjQ3ODIwNy0uNTczODQ4IDEuMTcxNjA2IC4xMTk1NTIgMS45ODQ1NTggLjExOTU1MkMyLjY0MjA5MiAuMTE5NTUyIDMuMjAzOTg1LS4zOTQ1MjEgMy41Mzg3My0uNzg5MDQxQzMuNjU4MjgxLS4wODM2ODYgNC4yMjAxNzQgLjExOTU1MiA0LjU3ODgyOSAuMTE5NTUyUzUuMjI0NDA4LS4wOTU2NDEgNS40Mzk2MDEtLjUyNjAyN0M1LjYzMDg4NC0uOTMyNTAzIDUuNzk4MjU3LTEuNjYxNzY4IDUuNzk4MjU3LTEuNzA5NTg5QzUuNzk4MjU3LTEuNzY5MzY1IDUuNzUwNDM2LTEuODE3MTg2IDUuNjc4NzA1LTEuODE3MTg2QzUuNTcxMTA4LTEuODE3MTg2IDUuNTU5MTUzLTEuNzU3NDEgNS41MTEzMzMtMS41NzgwODJDNS4zMzIwMDUtLjg3MjcyNyA1LjEwNDg1Ny0uMTE5NTUyIDQuNjE0Njk1LS4xMTk1NTJDNC4yNjc5OTUtLjExOTU1MiA0LjI0NDA4NS0uNDMwMzg2IDQuMjQ0MDg1LS42Njk0ODlDNC4yNDQwODUtLjk0NDQ1OCA0LjI3OTk1LTEuMDc1OTY1IDQuMzg3NTQ3LTEuNTQyMjE3QzQuNDcxMjMzLTEuODQxMDk2IDQuNTMxMDA5LTIuMTA0MTEgNC42MjY2NS0yLjQ1MDgwOUM1LjA2ODk5MS00LjI0NDA4NSA1LjE3NjU4OC00LjY3NDQ3MSA1LjE3NjU4OC00Ljc0NjIwMkM1LjE3NjU4OC00LjkxMzU3NCA1LjA0NTA4MS01LjA0NTA4MSA0Ljg2NTc1My01LjA0NTA4MUM0LjQ4MzE4OC01LjA0NTA4MSA0LjM4NzU0Ny00LjYyNjY1IDQuMzYzNjM2LTQuNDgzMTg4WicvPgo8cGF0aCBpZD0nZzMtOTgnIGQ9J00yLjc2MTY0NC03Ljk5ODAwN0MyLjc3MzU5OS04LjA0NTgyOCAyLjc5NzUwOS04LjExNzU1OSAyLjc5NzUwOS04LjE3NzMzNUMyLjc5NzUwOS04LjI5Njg4NyAyLjY3Nzk1OC04LjI5Njg4NyAyLjY1NDA0Ny04LjI5Njg4N0MyLjY0MjA5Mi04LjI5Njg4NyAyLjIxMTcwNi04LjI2MTAyMSAxLjk5NjUxMy04LjIzNzExMUMxLjc5MzI3NS04LjIyNTE1NiAxLjYxMzk0OC04LjIwMTI0NSAxLjM5ODc1NS04LjE4OTI5QzEuMTExODMxLTguMTY1MzggMS4wMjgxNDQtOC4xNTM0MjUgMS4wMjgxNDQtNy45MzgyMzJDMS4wMjgxNDQtNy44MTg2OCAxLjE0NzY5Ni03LjgxODY4IDEuMjY3MjQ4LTcuODE4NjhDMS44NzY5NjEtNy44MTg2OCAxLjg3Njk2MS03LjcxMTA4MyAxLjg3Njk2MS03LjU5MTUzMkMxLjg3Njk2MS03LjUwNzg0NiAxLjc4MTMyLTcuMTYxMTQ2IDEuNzMzNDk5LTYuOTQ1OTUzTDEuNDQ2NTc1LTUuNzk4MjU3QzEuMzI3MDI0LTUuMzIwMDUgLjY0NTU3OS0yLjYwNjIyNyAuNTk3NzU4LTIuMzkxMDM0Qy41Mzc5ODMtMi4wOTIxNTQgLjUzNzk4My0xLjg4ODkxNyAuNTM3OTgzLTEuNzMzNDk5Qy41Mzc5ODMtLjUxNDA3MiAxLjIxOTQyNyAuMTE5NTUyIDEuOTk2NTEzIC4xMTk1NTJDMy4zODMzMTMgLjExOTU1MiA0LjgxNzkzMy0xLjY2MTc2OCA0LjgxNzkzMy0zLjM5NTI2OEM0LjgxNzkzMy00LjQ5NTE0MyA0LjE5NjI2NC01LjI3MjIyOSAzLjI5OTYyNi01LjI3MjIyOUMyLjY3Nzk1OC01LjI3MjIyOSAyLjExNjA2NS00Ljc1ODE1NyAxLjg4ODkxNy00LjUxOTA1NEwyLjc2MTY0NC03Ljk5ODAwN1pNMi4wMDg0NjgtLjExOTU1MkMxLjYyNTkwMy0uMTE5NTUyIDEuMjA3NDcyLS40MDY0NzYgMS4yMDc0NzItMS4zMzg5NzlDMS4yMDc0NzItMS43MzM0OTkgMS4yNDMzMzctMS45NjA2NDggMS40NTg1MzEtMi43OTc1MDlDMS40OTQzOTYtMi45NTI5MjcgMS42ODU2NzktMy43MTgwNTcgMS43MzM0OTktMy44NzM0NzRDMS43NTc0MS0zLjk2OTExNiAyLjQ2Mjc2NS01LjAzMzEyNiAzLjI3NTcxNi01LjAzMzEyNkMzLjgwMTc0My01LjAzMzEyNiA0LjA0MDg0Ny00LjUwNzA5OCA0LjA0MDg0Ny0zLjg4NTQzQzQuMDQwODQ3LTMuMzExNTgyIDMuNzA2MTAyLTEuOTYwNjQ4IDMuNDA3MjIzLTEuMzM4OTc5QzMuMTA4MzQ0LS42OTM0IDIuNTU4NDA2LS4xMTk1NTIgMi4wMDg0NjgtLjExOTU1MlonLz4KPC9kZWZzPgo8ZyBpZD0ncGFnZTEnPgo8dXNlIHg9JzAnIHk9JzAnIHhsaW5rOmhyZWY9JyNnMy03MycvPgo8dXNlIHg9JzYuMTAyNzgyJyB5PSctNC4zMzg0MzcnIHhsaW5rOmhyZWY9JyNnMC0zJy8+Cjx1c2UgeD0nNS4xNjI5MDInIHk9JzIuOTU1NTE1JyB4bGluazpocmVmPScjZzItMTEnLz4KPHVzZSB4PScxNC40MjA4MDInIHk9JzAnIHhsaW5rOmhyZWY9JyNnNS02MScvPgo8dXNlIHg9JzI2Ljg0NjI4MycgeT0nMCcgeGxpbms6aHJlZj0nI2c1LTkxJy8+Cjx1c2UgeD0nMzAuMDk3OTQ0JyB5PScwJyB4bGluazpocmVmPScjZzMtOTcnLz4KPHVzZSB4PSczNi4yNDI4ODknIHk9JzEuNzkzMjYzJyB4bGluazpocmVmPScjZzQtNDknLz4KPHVzZSB4PSc0MC45NzUyMDMnIHk9JzAnIHhsaW5rOmhyZWY9JyNnMy01OScvPgo8dXNlIHg9JzQ2LjIxOTM2MicgeT0nMCcgeGxpbms6aHJlZj0nI2czLTk4Jy8+Cjx1c2UgeD0nNTEuMTk2NDY4JyB5PScxLjc5MzI2MycgeGxpbms6aHJlZj0nI2c0LTQ5Jy8+Cjx1c2UgeD0nNTUuOTI4NzgzJyB5PScwJyB4bGluazpocmVmPScjZzUtOTMnLz4KPHVzZSB4PSc2MS44MzcxMDcnIHk9JzAnIHhsaW5rOmhyZWY9JyNnMS0yJy8+Cjx1c2UgeD0nNzMuNzkyMjY4JyB5PScwJyB4bGluazpocmVmPScjZzEtMScvPgo8dXNlIHg9Jzc5LjEwNTY1NicgeT0nMCcgeGxpbms6aHJlZj0nI2cxLTEnLz4KPHVzZSB4PSc4NC40MTkwNDMnIHk9JzAnIHhsaW5rOmhyZWY9JyNnMS0xJy8+Cjx1c2UgeD0nOTAuMzk2NTk3JyB5PScwJyB4bGluazpocmVmPScjZzEtMicvPgo8dXNlIHg9JzEwMi4zNTE3NTgnIHk9JzAnIHhsaW5rOmhyZWY9JyNnNS05MScvPgo8dXNlIHg9JzEwNS42MDM0MTknIHk9JzAnIHhsaW5rOmhyZWY9JyNnMy05NycvPgo8dXNlIHg9JzExMS43NDgzNjMnIHk9JzEuNzkzMjYzJyB4bGluazpocmVmPScjZzItMTAwJy8+Cjx1c2UgeD0nMTE2LjYwMzgxMicgeT0nMCcgeGxpbms6aHJlZj0nI2czLTU5Jy8+Cjx1c2UgeD0nMTIxLjg0Nzk3MScgeT0nMCcgeGxpbms6aHJlZj0nI2czLTk4Jy8+Cjx1c2UgeD0nMTI2LjgyNTA3NycgeT0nMS43OTMyNjMnIHhsaW5rOmhyZWY9JyNnMi0xMDAnLz4KPHVzZSB4PScxMzEuNjgwNTI2JyB5PScwJyB4bGluazpocmVmPScjZzUtOTMnLz4KPC9nPgo8L3N2Zz4KPCEtLSBERVBUSD00IC0tPg==) where

where  and

and  for all

for all  and which verifies

and which verifies  .

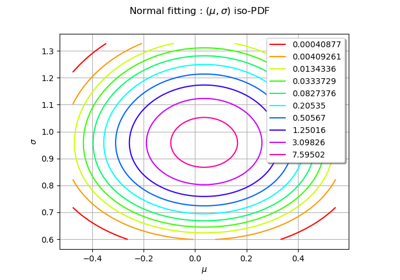

.Examples

Create a sample from a Normal distribution:

>>> import openturns as ot >>> sample = ot.Normal().getSample(10) >>> ot.ResourceMap.SetAsUnsignedInteger('DistributionFactory-DefaultBootstrapSize', 100)

Fit a Normal distribution and extract the asymptotic parameters distribution:

>>> fittedRes = ot.NormalFactory().buildEstimator(sample) >>> paramDist = fittedRes.getParameterDistribution()

Determine the bilateral confidence interval at level 0.9:

>>> confInt = paramDist.computeBilateralConfidenceInterval(0.9)

- computeBilateralConfidenceIntervalWithMarginalProbability(prob)¶

Compute a bilateral confidence interval.

Refer to

computeBilateralConfidenceInterval()- Parameters:

- alphafloat,

The confidence level.

- alphafloat,

- Returns:

- confInterval

Interval The confidence interval of level

.- marginalProbfloat

The value

which is the common marginal probability of each marginal interval.

- confInterval

Examples

Create a sample from a Normal distribution:

>>> import openturns as ot >>> sample = ot.Normal().getSample(10) >>> ot.ResourceMap.SetAsUnsignedInteger('DistributionFactory-DefaultBootstrapSize', 100)

Fit a Normal distribution and extract the asymptotic parameters distribution:

>>> fittedRes = ot.NormalFactory().buildEstimator(sample) >>> paramDist = fittedRes.getParameterDistribution()

Determine the bilateral confidence interval at level 0.9 with marginal probability:

>>> confInt, marginalProb = paramDist.computeBilateralConfidenceIntervalWithMarginalProbability(0.9)

- computeCDF(*args)¶

Compute the cumulative distribution function.

- Parameters:

- Xsequence of float, 2-d sequence of float

CDF input(s).

- Returns:

- Ffloat,

Point CDF value(s) at input(s)

.

.

- Ffloat,

Notes

The cumulative distribution function is defined as:

- computeCDFGradient(*args)¶

Compute the gradient of the cumulative distribution function.

- Parameters:

- Xsequence of float

CDF input.

- Returns:

- dFdtheta

Point Partial derivatives of the CDF with respect to the distribution parameters at input

.

- dFdtheta

- computeCharacteristicFunction(*args)¶

Compute the characteristic function.

- Parameters:

- tfloat

Characteristic function input.

- Returns:

- phicomplex

Characteristic function value at input

.

.

Notes

The characteristic function is defined as:

![\phi_X(t) = \mathbb{E}\left[\exp(- i t X)\right],