Graphical goodness-of-fit tests¶

This method deals with the modelling of a probability distribution of a

random vector  . It

seeks to verify the compatibility between a sample of data

. It

seeks to verify the compatibility between a sample of data

and a

candidate probability distribution previous chosen.

The use of graphical tools allows one to answer this question in the one

dimensional case

and a

candidate probability distribution previous chosen.

The use of graphical tools allows one to answer this question in the one

dimensional case  , and with a continuous distribution.

The QQ-plot, and henry line tests are defined in the case to

, and with a continuous distribution.

The QQ-plot, and henry line tests are defined in the case to

. Thus we denote

. Thus we denote  . The first

graphical tool provided is a QQ-plot (where “QQ” stands

for “quantile-quantile”). In the specific case of a Normal distribution,

Henry’s line may also be used.

. The first

graphical tool provided is a QQ-plot (where “QQ” stands

for “quantile-quantile”). In the specific case of a Normal distribution,

Henry’s line may also be used.

QQ-plot

A QQ-Plot is based on the notion of quantile. The

-quantile

-quantile  of

of  , where

, where

, is defined as follows:

, is defined as follows:

If a sample  of is

available, the quantile can be estimated empirically:

of is

available, the quantile can be estimated empirically:

the sample

is first placed in

ascending order, which gives the sample

;

;then, an estimate of the

-quantile is:![\begin{aligned}

\widehat{q}_{X}(\alpha) = x_{([N\alpha]+1)}

\end{aligned}](../../_images/math/0a341e5d3f95636551278f5516cdd44417d5fd53.svg)

where ![[N\alpha]](../../_images/math/f8ddfef745b6a134169e41715aa061e1ef550f7b.svg) denotes the integral part of

denotes the integral part of

.

.

Thus, the  smallest value of the sample

smallest value of the sample

is an estimate

is an estimate  of the

-quantile where

of the

-quantile where  (

( ).

).

Let us then consider the candidate probability distribution being

tested, and let us denote by  its cumulative distribution

function. An estimate of the -quantile can be also

computed from :

its cumulative distribution

function. An estimate of the -quantile can be also

computed from :

If is really the cumulative distribution function of

, then and

should be close. Thus, graphically, the

points

should be close. Thus, graphically, the

points

should be close to the diagonal.

should be close to the diagonal.

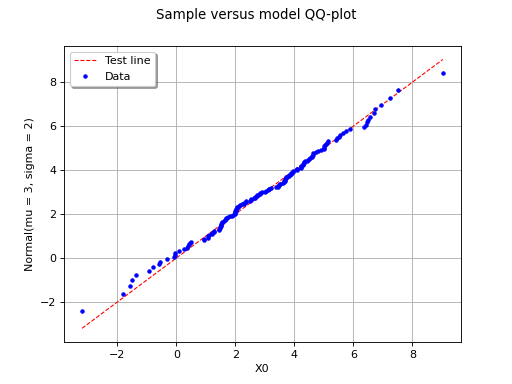

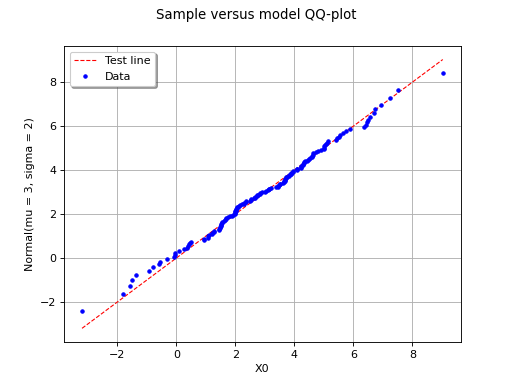

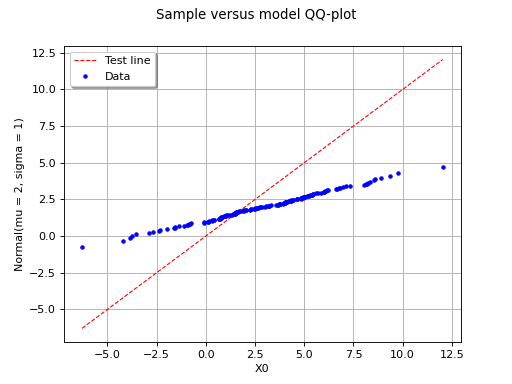

The following figure illustrates the principle of a QQ-plot with a

sample of size  . Note that the unit of the two axis is that

of the variable studied; the quantiles determined via

are called here “value of

. Note that the unit of the two axis is that

of the variable studied; the quantiles determined via

are called here “value of  ”. In this example, the

points remain close to the diagonal and the hypothesis “ is the

cumulative distribution function of ” does not seem irrelevant,

even if a more quantitative analysis (see for instance ) should be

carried out to confirm this.

”. In this example, the

points remain close to the diagonal and the hypothesis “ is the

cumulative distribution function of ” does not seem irrelevant,

even if a more quantitative analysis (see for instance ) should be

carried out to confirm this.

(Source code, png, hires.png, pdf)

{kind=link}

{kind=link}

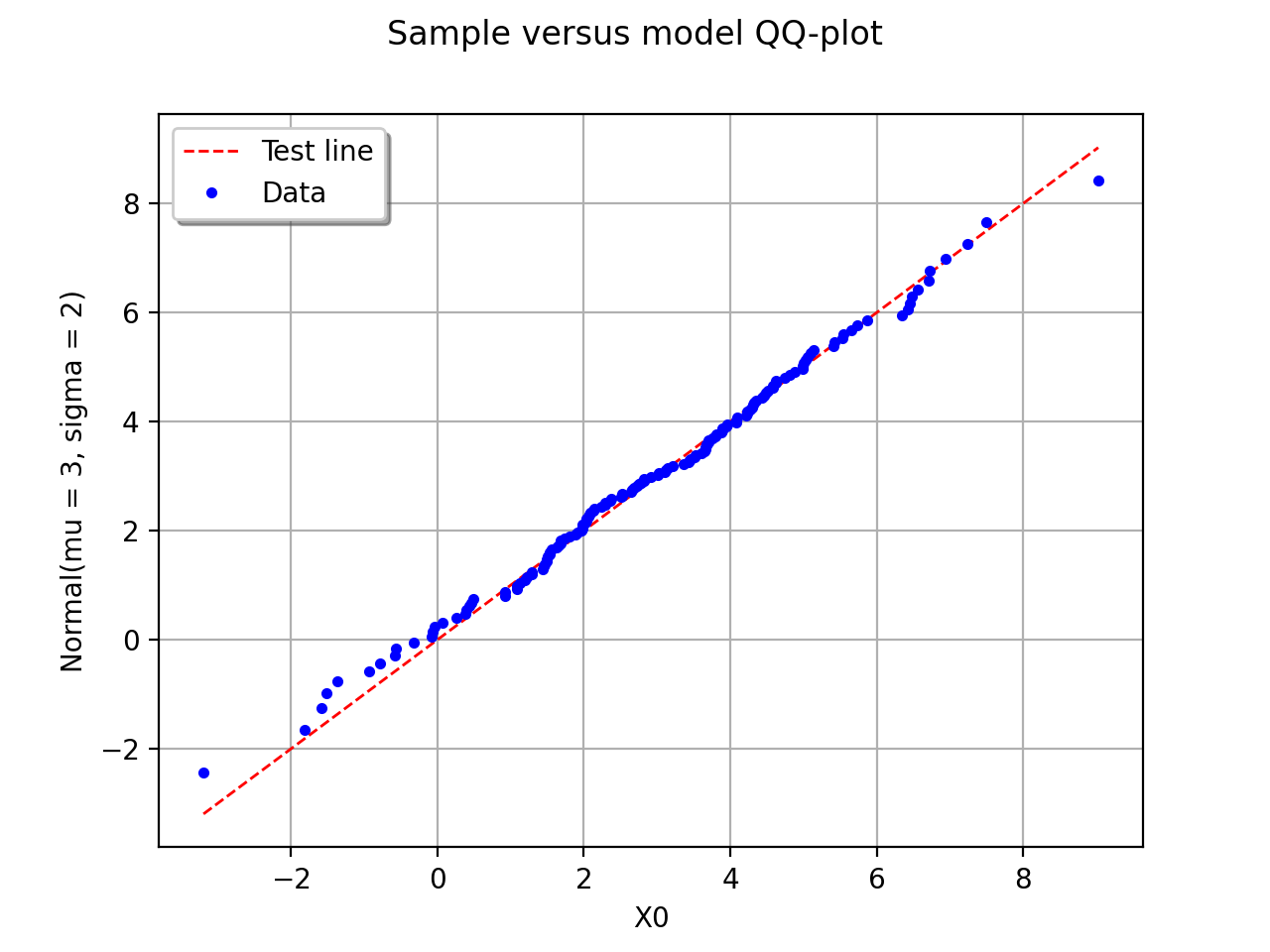

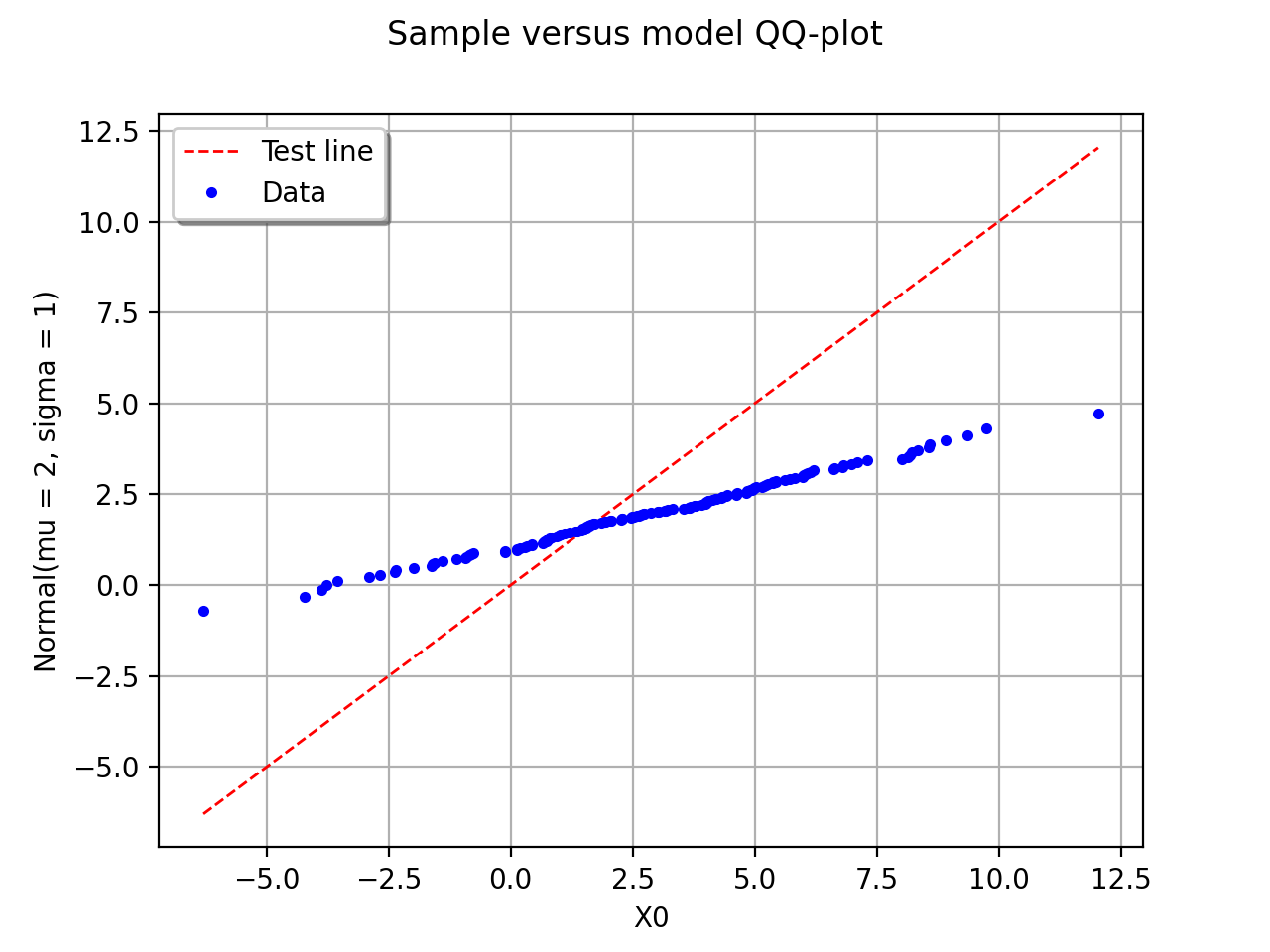

In this second example, the candidate distribution function is clearly irrelevant.

(Source code, png, hires.png, pdf)

{kind=link}

{kind=link}

Henry’s line

This second graphical tool is only relevant if the candidate

distribution function being tested is gaussian. It also uses the ordered

sample introduced for

the QQ-plot, and the empirical cumulative distribution function

presented in .

presented in .

By definition,

Then, let us denote by  the cumulative distribution

function of a Normal distribution with mean 0 and standard deviation 1.

The quantity

the cumulative distribution

function of a Normal distribution with mean 0 and standard deviation 1.

The quantity  is defined as follows:

is defined as follows:

If is distributed according to a normal probability

distribution with mean  and standard-deviation

and standard-deviation

, then the points

, then the points

should be close to the line defined by

should be close to the line defined by  .

This comes from a property of a normal distribution: it the distribution

of is really

.

This comes from a property of a normal distribution: it the distribution

of is really  , then the distribution of

, then the distribution of

is

is  .

.

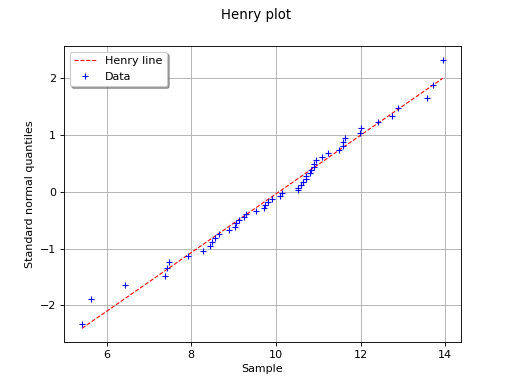

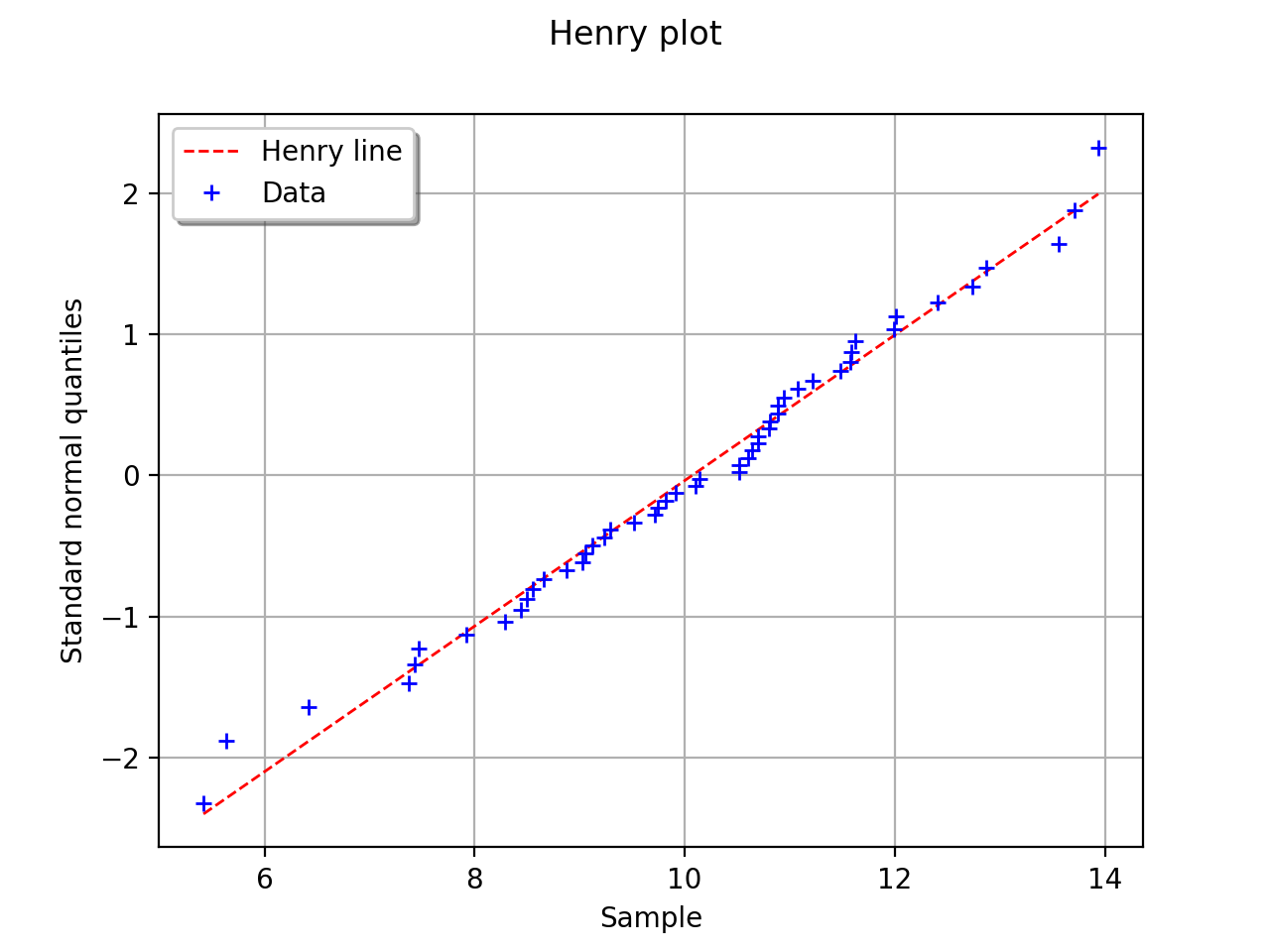

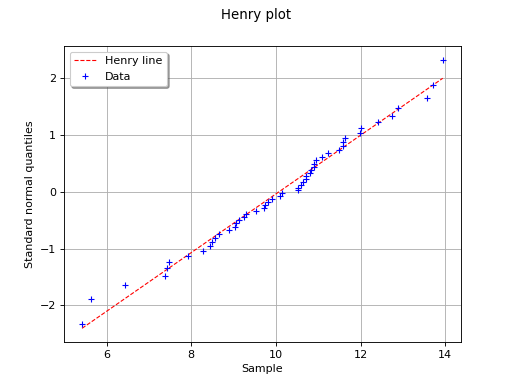

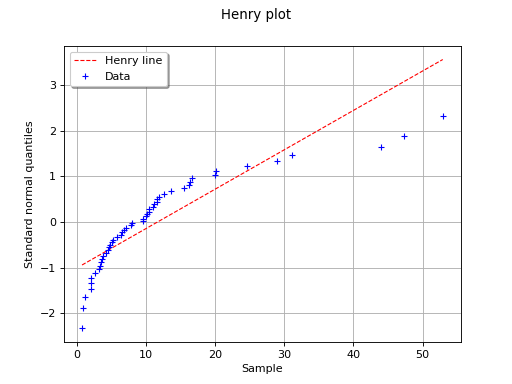

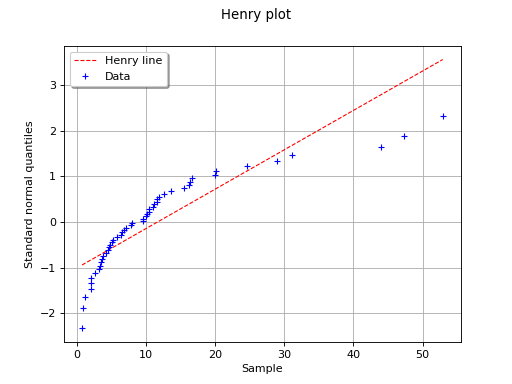

The following figure illustrates the principle of Henry’s graphical test

with a sample of size . Note that only the unit of the

horizontal axis is that of the variable studied. In this

example, the points remain close to a line and the hypothesis “the

distribution function of is a Gaussian one” does not seem

irrelevant, even if a more quantitative analysis (see for instance )

should be carried out to confirm this.

(Source code, png, hires.png, pdf)

{kind=link}

{kind=link}

In this example the test validates the hypothesis of a gaussian distribution.

(Source code, png, hires.png, pdf)

{kind=link}

{kind=link}

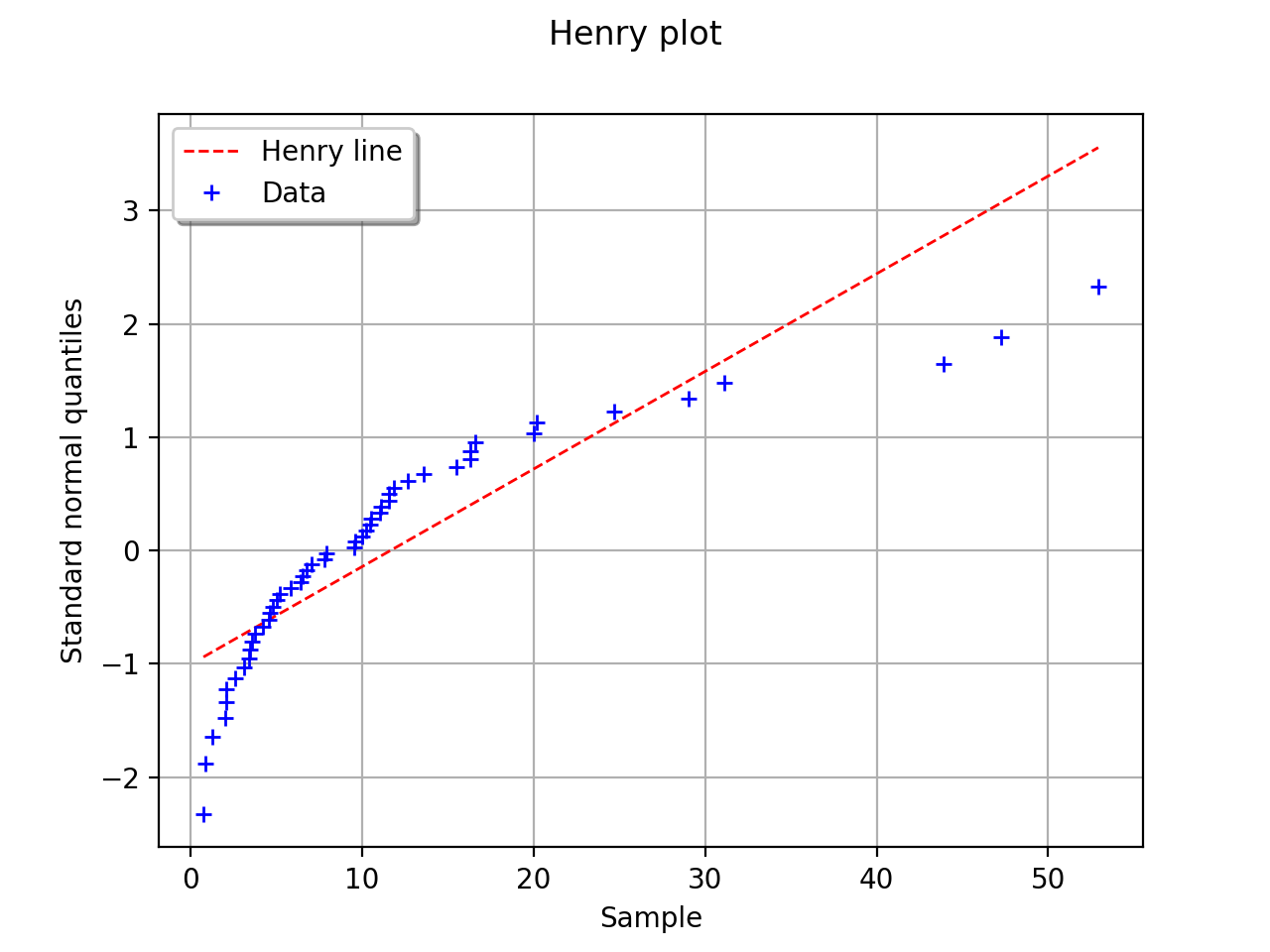

In this second example, the hypothesis of a gaussian distribution seems

far less relevant because of the behavior for small values of

.

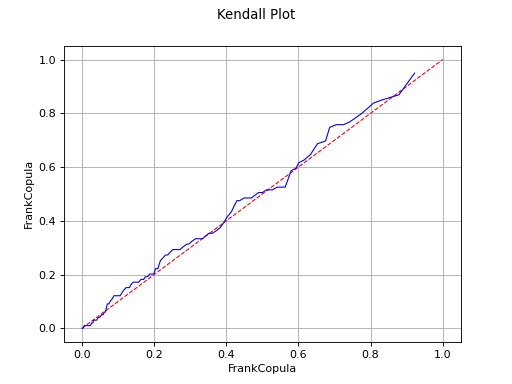

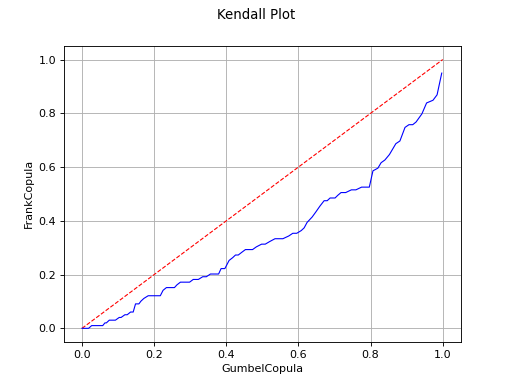

Kendall plot

In the bivariate case, the Kendall Plot test enables to validate the choice of a specific copula model or to verify that two samples share the same copula model.

Let  be a bivariate random vector which copula is

noted

be a bivariate random vector which copula is

noted  .

Let

.

Let  be a sample of

.

be a sample of

.

We note:

![\begin{aligned}

\forall i \geq 1, \displaystyle H_i = \frac{1}{n-1} Card \left\{ j \in [1,N], j \neq i, \, | \, x^j_1 \leq x^i_1 \mbox{ and } x^j_2 \leq x^i_2 \right \}

\end{aligned}](../../_images/math/465bc35c94a1e2056cd5fb1fb7020d346b732f56.svg)

and  the ordered statistics of

the ordered statistics of

.

.

The statistic  is defined by:

is defined by:

(1)¶

where  is the cumulative density function of

is the cumulative density function of

. We can show that this is the cumulative density function

of the random variate

. We can show that this is the cumulative density function

of the random variate  when

when  and

and  are

independent and follow

are

independent and follow  distributions.

distributions.

samples of size

samples of size

from the bivariate copula , in order to have

realizations of the statistics

from the bivariate copula , in order to have

realizations of the statistics

and have an estimation of

and have an estimation of

![W_i = E[H_{(i)}], \forall i \leq N](../../_images/math/ebb1476bb38b12f7376c309ac81d7bc81317d486.svg) .

. .

If the points are one the first diagonal, the copula model is

validated.

.

If the points are one the first diagonal, the copula model is

validated. respectively

associated to the first and second sample. Note that the two samples

must have the same size.

respectively

associated to the first and second sample. Note that the two samples

must have the same size.(Source code, png, hires.png, pdf)

{kind=link}

{kind=link}

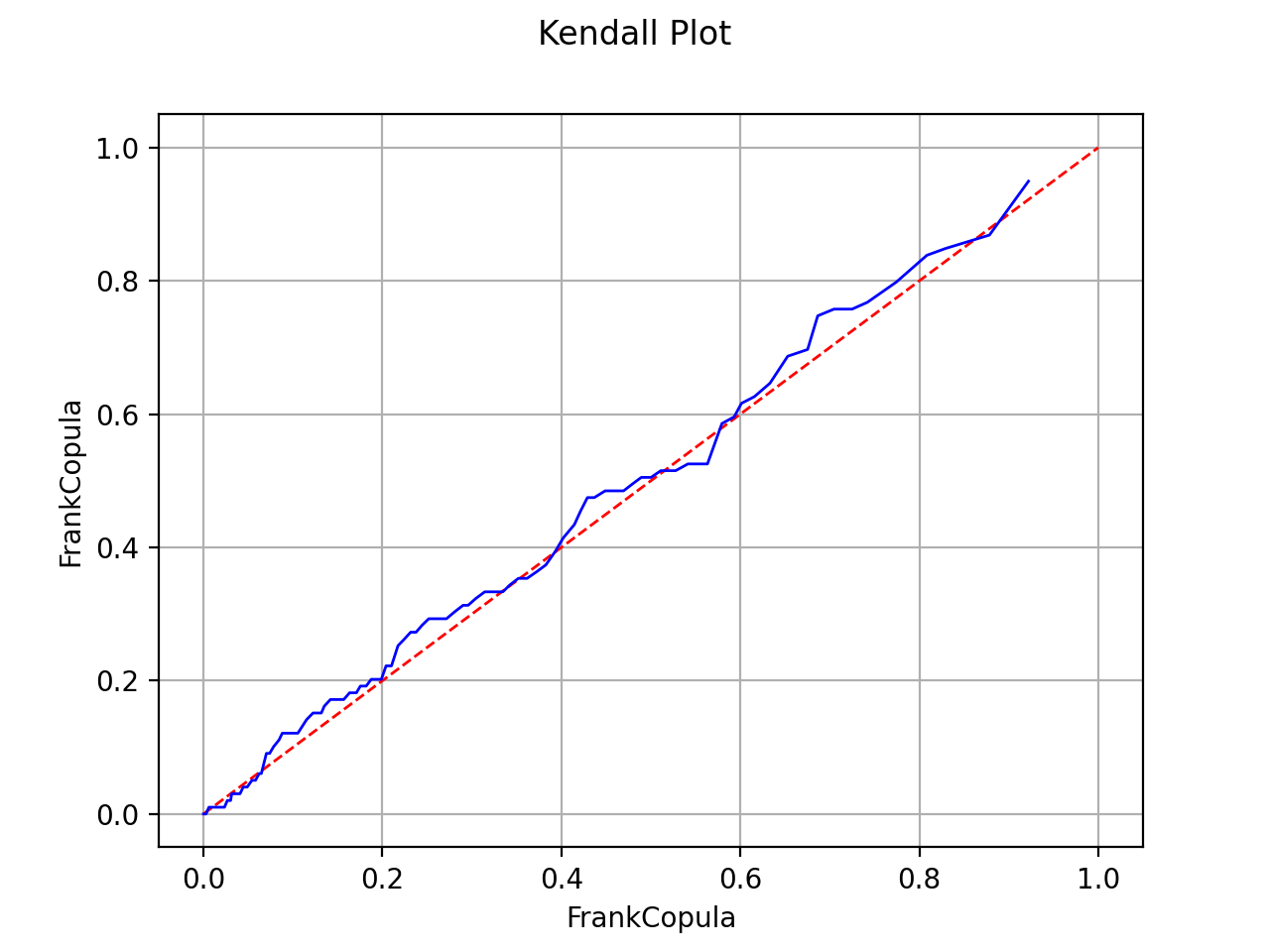

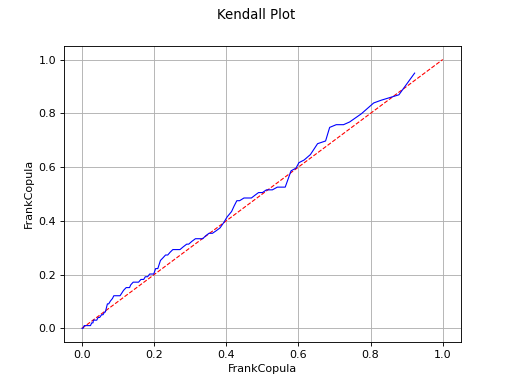

The Kendall Plot test validates the use of the Frank copula for a sample.

(Source code, png, hires.png, pdf)

{kind=link}

{kind=link}

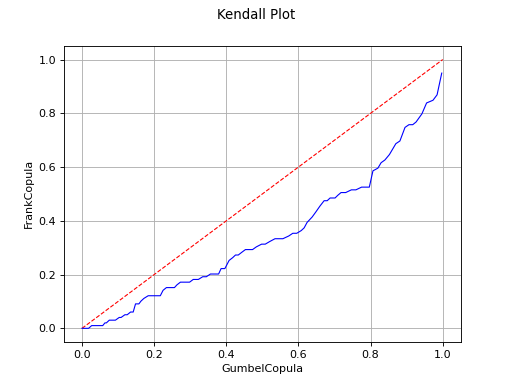

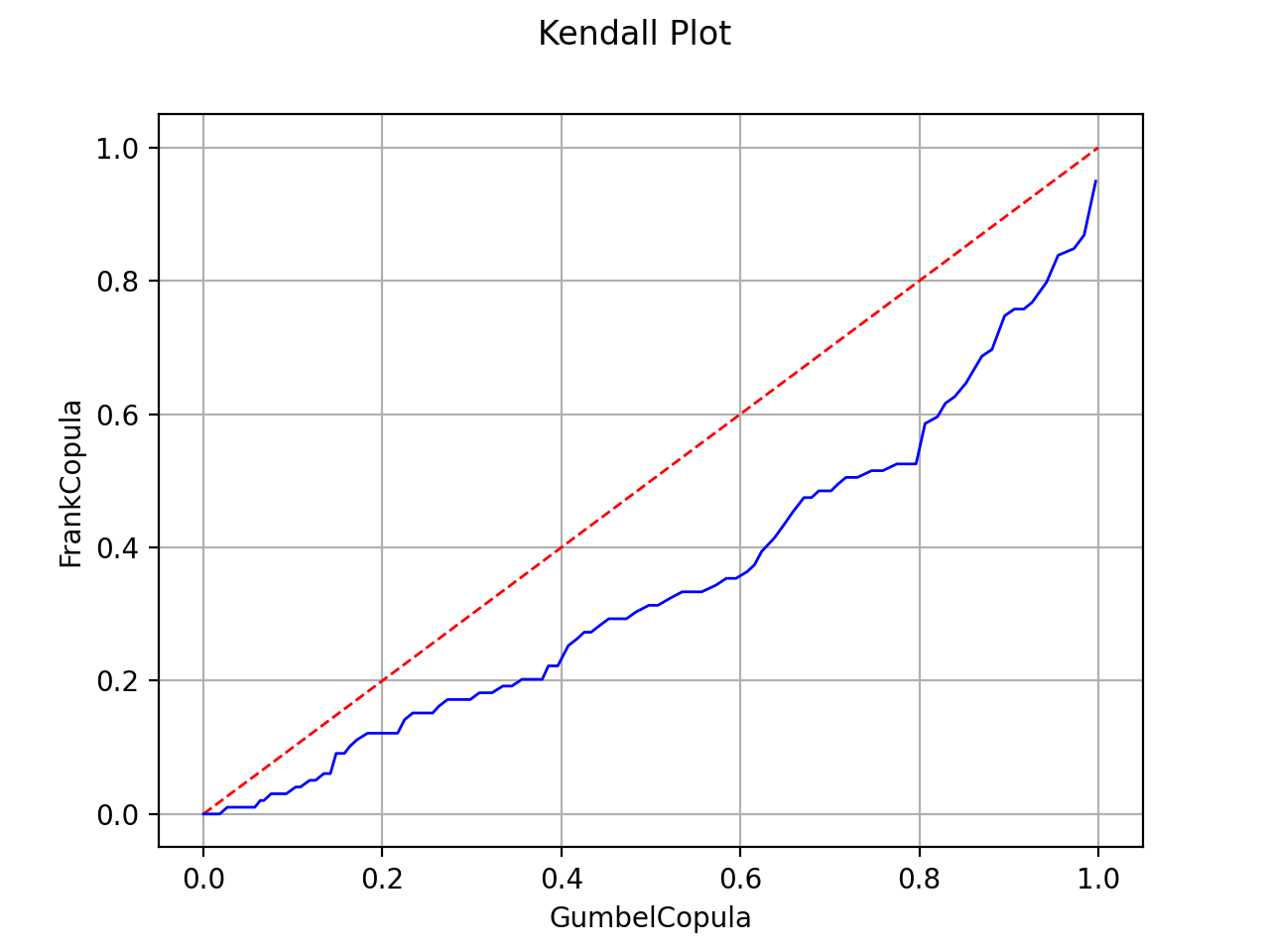

The Kendall Plot test invalidates the use of the Frank copula for a sample.

Remark: In the case where you want to test a sample with respect to a specific copula, if the size of the sample is superior to 500, we recommend to use the second form of the Kendall plot test: generate a sample of the proper size from your copula and then test both samples. This way of doing is more efficient.

API:

See

VisualTest_DrawQQplot()to draw a QQ plotSee

VisualTest_DrawHenryLine()to draw the Henry lineSee

VisualTest_DrawKendallPlot()to draw the Kendall plot

Examples:

See Draw the QQ-Plot

See Test Normality

See Test the copula

References: